PW Consulting: Strategic Preview — Copper Market 2026 Outlook and Why This Research Matters for Your Decisions

Executive snapshot

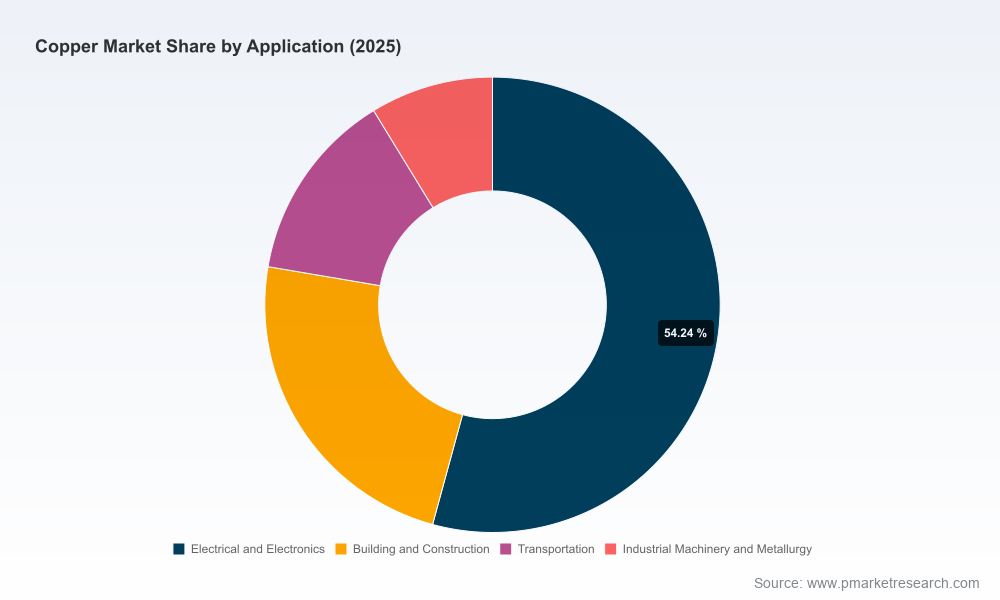

As global decarbonization, electrification and industrial modernization accelerate, copper is re-emerging as a strategic raw material whose market dynamics will shape corporate strategy through the rest of this decade. Our Copper Market study (base year 2025) frames that transition with a data-driven view of historic performance (2020–2025) and a forward-looking forecast (2026–2032). In short: the market that expanded from roughly USD 218 billion in 2020 to USD 306 billion in 2025 is projected to continue growing at a compound annual growth rate of 5.5% through 2032 — reaching a materially larger global market by the end of the forecast window.

Copper Market

This preview lays out the strategic implications of the report for 2026 corporate decision-making, highlights structural risks and opportunities, and summarizes the competitive landscape that will matter to producers, refiners, traders, equipment and services providers, and institutional investors. Detailed segmentation, scenario-weighted supply-demand balances, and proprietary price-paths remain reserved for the full report and supporting dashboards.

Copper Market

Why this matters for 2026 corporate decisions

- Capital allocation and project prioritization: With sustained mid-single-digit CAGR and a widening gap between demand growth and committed supply in many project pipelines, companies must re‑calibrate brownfield expansions, greenfield development timelines and deferred maintenance. The report equips executives to rank projects by payback under alternative price and availability scenarios.

- Procurement, sourcing and supply security: Recent shifts — including a historic TC/RC settlement in early 2026 and concentrated downstream capacity growth in a few countries — have compressive effects on smelting economics and regional availability. Procurement teams need scenario-driven sourcing playbooks that balance cost, traceability compliance and resilience.

- M&A and strategic partnerships: Market concentration metrics show meaningful consolidation at the top of the value chain. Our analysis helps identify targets where scale, geographic position or refining capability deliver asymmetric value under different demand trajectories.

- ESG and compliance strategy: With ISO progressing a global copper traceability standard and buyers accelerating scope-3 requirements, investments in traceable supply, certification pathways and third-party verification will no longer be optional for premium offtake.

Market trajectory and macro drivers

The copper market’s recent performance reflects a blend of demand seculars and episodic supply dynamics. Key demand drivers include electrification of transport, grid upgrades, renewable deployment and growth in high-power electronics. On the supply side, concentrated production, smelter capacity growth in specific jurisdictions, and the lag between discovery, permitting and first throughput create structural tightness.

Copper Market

Our 2026–2032 forecast at a 5.5% CAGR captures those sustained demand lifts while embedding a range of supply outcomes. Notably, publicly available project pipelines and our proprietary sourcing stress tests point to meaningful upside risk in tightening — with industry commentary flagging a potential multi‑decade shortfall if permitted and financed projects do not proceed at scale. For strategic planners, this means preparing for scenarios where the market swings from comfortable to constrained within a few years depending on policy, financing and operational execution.

Recent dynamics that change playbooks in 2026

- TC/RC pricing pressure: In January 2026 an unprecedented benchmark outcome reset tolling economics. This has implications for smelter margins, concentrate flows and the economics of concentrate-built portfolios versus integrated refined supply.

- Traceability and standards: ISO’s work on a copper traceability standard is accelerating. Firms that move early to align systems, audit trails and supplier engagement will be advantaged in offtake negotiations and in accessing sustainability-linked financing.

- Regional throughput changes: Aggregate refined output in some mature markets contracted in 2025 because of planned maintenance cycles even as new secondary capacity came online elsewhere. These dynamics create short-term regional tightness and highlight the importance of flexible logistics and secondary sourcing strategies.

- Concentrated smelter growth: Since 2005, the bulk of global smelter capacity expansion has been concentrated in a small number of countries. That geographic concentration elevates policy, trade and operational risk on global flows.

Competitive landscape — what leading players are doing

The industry is dominated by a mix of global majors and regionally focused producers. Market concentration is meaningful: the top three players control approximately 42% of attributable capacity, while the top five control roughly 68% — a structure that enables scale advantages but also creates exposure where a small set of operational disruptions can move global balances.

- BHP (Melbourne): Continues to prioritize low‑cost open-pit operations and exploration. Their capital allocation is focused on extending life-of-mine and decarbonization of primary operations — moves that reduce long-term operating cost and emissions risk.

- Codelco (Santiago): The state-owned producer remains a cornerstone of supply. Its scale, relationship with national policy and capital program choices make it a strategic bellwether for policymakers and markets alike.

- Freeport-McMoRan (Phoenix): Maintains a North America-centric asset base with a focus on cathode and concentrate production. Its operational choices influence regional availability and price sensitivity in the U.S. market.

- Rio Tinto (London): Leverages integrated operations to manage cost volatility and maintain refined throughput. Their portfolio decisions illustrate the value of flexibility between concentrate and refined exposure.

- Southern Copper (Peru), Glencore (Baar) and Antofagasta (Santiago): These players combine regional sourcing strength, trading capability and integrated value-chain positions. Trading desks and offtake agreements are increasingly strategic assets as TCs and traceability requirements evolve.

Across the board, leading firms are prioritizing three strategic moves: (1) locking offtake and downstream integration to secure margin, (2) investing in traceability and low‑carbon pathways to preserve premium access, and (3) pursuing targeted M&A to diversify geological and geopolitical exposure. Our full report maps these moves to likely outcomes under alternative market scenarios.

What PW Consulting’s Copper Market report contains (practical elements)

The full study is a practitioner’s playbook designed for executives who must make near-term decisions within a two- to five-year investment horizon while managing long-horizon strategic risk. Highlights include:

- Scenario-driven supply‑demand models (2026–2032) with sensitized price paths and scenario probabilities calibrated to permit, finance and execution risks;

- Project pipeline heatmaps and decision matrices that prioritize projects by capital efficiency, execution lead time and strategic fit;

- Smelter and refinery margin simulations that incorporate evolving TC/RC outcomes, energy cost trajectories and traceability premiums;

- Risk registers and playbooks for procurement, logistics and inventory management tailored for producers, end‑users and traders;

- Strategic options frameworks for M&A, joint ventures and offtake structuring that show how different combinations of assets and contracts perform across scenarios;

- Regulatory and ESG impact analysis, including a roadmap to operationalize ISO traceability certification and to capture sustainability-linked financing;

- Executive dashboards and decision-support templates (licensable) to run bespoke sensitivity tests for board-level deliberations.

To preserve commercial value for subscribers we demonstrate methodologies, provide executive summaries and high-level scenario outcomes in this preview, while granular regional, type and application splits and proprietary price projections are available in the subscriber package.

Actionable implications for 2026 planning cycles

- Reassess short-term hedging and pricing strategies: With tolling dynamics and downstream capacity moves shifting cash-flows, companies should re-run hedging models under the updated base-case and downside scenarios.

- Prioritize traceable supply lanes: Establish near-term pilots to align purchasing, certification and supplier-assurance workflows with emerging international standards — these pilots convert into tangible negotiating leverage within 12–18 months.

- Re-evaluate brownfield investments: Brownfield expansions often deliver quicker throughput than greenfield projects; use our project prioritization lens to re-rank CAPEX queues by expected IRR under multiple market scenarios.

- Prepare contingency sourcing plans: Given concentrated smelter growth and episodic maintenance in legacy markets, maintain flexible logistics contracts and consider short-term secondary sourcing to smooth production curves.

- Embed scenario-testing into capital committees: Require project approval gates to include stress-tested outcomes against both fast‑tightening and moderate‑growth scenarios from our forecast suite.

How PW Consulting can help

Our Copper Market study synthesizes proprietary models, project-level data and scenario analysis into decision-ready outputs for boardrooms and operating teams. Clients receive the full dataset, interactive dashboards and advisory time to translate model outputs into actionable capital, procurement and commercial strategies.

If your organization faces material exposure to copper prices, supply reliability or traceability requirements in 2026 planning cycles, investing in a tightly focused strategic assessment now will materially reduce execution risk and protect margin through the next stage of market tightening. For access to the full report, granular segmentation tables, and bespoke scenario workshops, download the subscriber package on our research portal or contact PW Consulting’s Metals Practice to arrange an executive briefing.

For detailed analysis of this topic, please visit the official page:Copper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com