E-Commerce Packaging Market Emerging Trends and Outlook

Technology |

2026-04-13 12:20:04

As organizations accelerate investments in resilience, distributed energy and critical infrastructure, the market for Automatic Transfer Switches (ATS) has become a quietly strategic battleground. PW Consulting’s latest study — grounded in a 2025 base year and a 2026–2032 forecast horizon — quantifies a steadily expanding market that we project to grow at a compound annual growth rate (CAGR) of approximately 5.51%. In absolute terms the market has expanded meaningfully since 2020 and is forecast to surpass the billion-dollar threshold in the near term, moving toward higher mid‑single‑digit growth through 2032. For executives making procurement, product, or M&A decisions in 2026, this briefing summarizes the patterns, regulatory inflection points, and competitive dynamics that will determine winners and losers — while reserving the granular segmentation tables for the full report.

Automatic Transfer Switches Market

Automatic Transfer Switches are no longer a commoditized accessory. They are the decision point that links utility grids, on-site generation, energy storage, and building or process controls. ATS technology choices — electromechanical, circuit-breaker-based, or solid-state — influence project architecture, commissioning timelines, interoperability with generator controls, and long-term operational expenditures. The market’s steady growth reflects multiple drivers: expanding data center and healthcare capacity, on-site generation for resiliency, tighter regulatory constraints, and the rising adoption of integrated power management systems in commercial and industrial facilities.

Automatic Transfer Switches Market

PW Consulting’s base-year measurement (2025) and forecast series illuminate the investment scale organizations must plan for as resiliency and energy security rise on boardroom agendas. The growth profile and near-term inflection points should prompt CFOs and asset owners to accelerate lifecycle planning for critical power — not just CapEx — and to embed ATS strategy into broader electrification and DER (distributed energy resources) roadmaps.

Automatic Transfer Switches Market

Regulatory tightening and standards evolution: The revised UL 1008 standard (including the recent amendment addressing solid‑state transfer switches) and prevailing NEMA/ANSI commissioning standards impose clearer performance and testing baselines. These changes raise the bar for vendor qualification and acceptance testing; procurement teams must demand evidence of compliance and updated test reports rather than relying on legacy certifications alone.

Public procurement and localization requirements: Critical infrastructure projects in several jurisdictions are subject to Buy‑Local and Build America/Buy America rules. This has immediate implications for suppliers and integrators seeking public-sector work, and for OEMs that must demonstrate local content or supply‑chain traceability to remain eligible.

Technology spectrum and architecture implications: The market is seeing parallel investments in traditional contactor and circuit‑breaker ATS architectures and in solid‑state alternatives. Solid‑state evolution offers faster transfer, reduced wear points, and better harmonics behavior with power-electronic‑rich environments, but it brings new commissioning, thermal, and lifecycle considerations.

Installation and service economics: ATS units are typically installed in under a day by qualified electricians, reducing labor intensity versus larger electrical retrofits. That said, commissioning to ANSI/NETA ECS standards and coordination with generator controls adds project time and skilled labor needs — a growing source of schedule and cost risk for fast-paced deployments.

Price and supply signaling: Recent product catalog and price list releases from leading manufacturers underscore active portfolio updates and commercial re‑positioning in 2024–2025. Buyers should anticipate periodic price adjustments tied to commodity cycles, regulatory compliance costs, and premium positioning for features such as remote monitoring or integrated controls.

The ATS market exhibits a mixed structure: established global incumbents with broad portfolios coexist with specialist vendors and regional manufacturers addressing project and cost niches. Market concentration is meaningful but not prohibitive — a handful of large players command a sizable share, while a long tail of specialists competes on customization, speed-to-delivery, or price.

Eaton Corporation and Schneider Electric: These multi‑technology players offer comprehensive UL‑listed portfolios that span residential, commercial, and mission‑critical segments. Their strength is in integrated systems — ATS paired with power distribution and monitoring — plus deep channel and service networks. Expect them to continue leveraging portfolio breadth and modernization offerings into 2026.

ABB Electrification and Siemens: Positioning is centered on compact industrial designs, integrated controllers and digitaling features for plant automation. Both vendors compete strongly where ATS is part of a larger electrification or medium‑voltage strategy.

Generator-aligned OEMs (Generac, Kohler, Cummins): These firms differentiate by close integration of ATS with generator sets and turnkey backup power solutions — a crucial advantage in commercial and residential‑oriented projects and in federal procurement where generator pairing and compliance matter.

Mission-critical specialists (ASCO, Russelectric, Lake Shore, Socomec): These vendors emphasize high‑reliability designs, bypass/isolation options, and tailored solutions for data centers, healthcare and industrial facilities. Their value proposition centers on engineering depth, service contracts, and long product lifecycles.

Regional and low‑cost manufacturers (select China-based and North American bespoke builders): These suppliers compete on price, rapid project turnaround, and project-oriented approaches; they often win in volume-sensitive segments and projects with in-country manufacturing preferences.

For buyers, the strategic choice is whether to prioritize integrated system suppliers with global service reach, specialist vendors for mission-critical performance, or local manufacturers for cost and delivery. Each route implies different trade-offs in life-cycle cost, warranty & service, and compliance assurance — and PW Consulting’s vendor scorecards in the full report expose these trade-offs in operationally useful terms.

Standards-driven redesign risk: The solid‑state standard revision and evolving UL expectations create a retrofit and obsolescence risk for older ATS fleets. Organizations should inventory ATS assets and prioritize replacement based on interoperability and testing gaps.

Supply and pricing volatility: Component and raw material swings will continue to affect the OEMs differently; long lead-time components can create project slippage. Strategic buyers should negotiate price‑protection clauses and tiered delivery schedules where possible.

Service & commissioning scarcity: Qualified commissioning resources are increasingly a gating factor. Early procurement of commissioning services and specification of ANSI/NETA ECS‑compliant testing in contracts will reduce schedule overruns and performance claims.

Integration and software opportunity: ATS with advanced controllers and digital interfaces unlock remote health monitoring, predictive maintenance, and faster turnarounds for staged black‑start or microgrid operations. There is a commercial upside for suppliers and integrators that can package ATS hardware with EMS/BMS services and SaaS monitoring.

To support 2026 decision cycles, the PW Consulting ATS study combines quantitative modeling with operational playbooks. Highlights include:

Validated market sizing and base‑year reconciliation (2020–2025) plus scenario forecasts through 2032 (CAGR 5.51% base case), presented with transparent assumptions and sensitivity levers.

Standards and regulatory tracker with procurement checklists — including UL 1008 revisions, NEMA/ANSI commissioning implications, and public procurement localization rules — to accelerate compliant vendor selection.

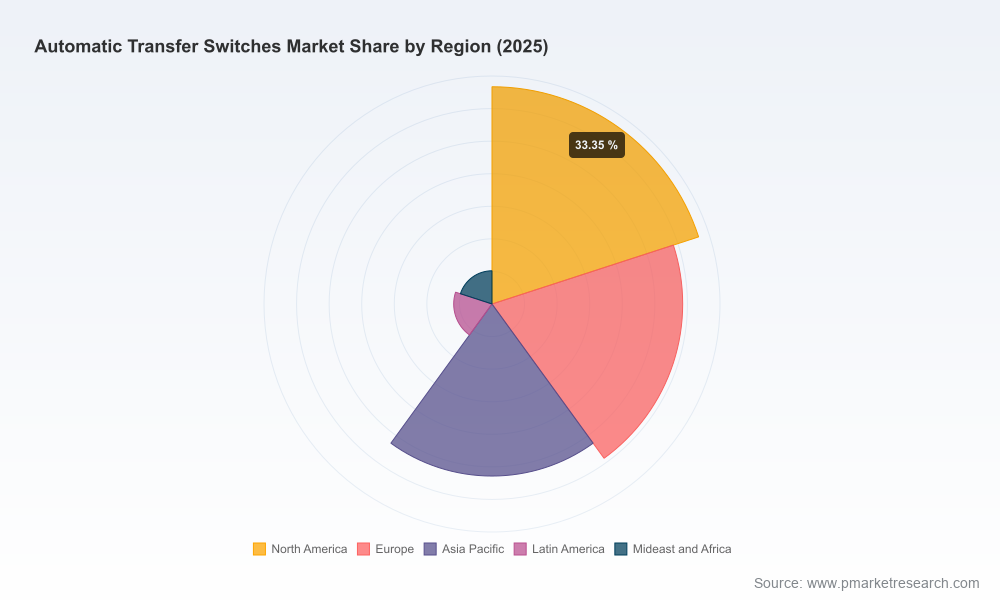

Vendor landscape maps and unbiased supplier scorecards that compare reliability, digital features, service footprint, compliance posture and total cost of ownership. (Note: detailed regional/application splits and vendor volume tables are reserved for the full report.)

Practical decision aids: CapEx vs. lifecycle O&M calculators, retrofit prioritization matrixes for aging fleets, sample RFP language for ATS procurement, and commissioning acceptance templates aligned to ANSI/NETA ECS‑2024.

M&A and partnership opportunity scans for strategic buyers, including pockets of consolidation potential where engineering-heavy specialists may be acquired by system integrators or generator OEMs seeking vertical integration.

Perform an ATS asset health and compliance audit now. Use the audit to prioritize units for replacement based on UL, performance, and integration gaps rather than simple age or failure history.

Define a procurement specification that mandates certifiable compliance, commissioning deliverables, and digital interoperability with your EMS/BMS platforms. Require suppliers to provide commissioning evidence aligned to ANSI/NETA ECS‑2024.

Lock in service agreements or hybrid CapEx/Opex models with vendors that can guarantee response SLAs — especially for healthcare, data centers, and other mission‑critical facilities.

Evaluate the total system economics for solid‑state vs. electromechanical options in your environment. Consider thermal management, harmonics, maintenance cadence, and lifecycle replacement costs.

For public-sector contractors, work with suppliers able to demonstrate local content and supply‑chain traceability to meet Build America/Buy America and related rules.

The ATS market’s steady expansion, underpinned by a mid‑single‑digit CAGR and clear regulatory momentum, makes transfer-switch strategy a consequential element of infrastructure planning in 2026. Our study distills the numeric trends, regulatory changes, supplier strengths and operational levers into tools that procurement, engineering, and executive teams can use immediately. This briefing highlights the strategic contours; the full PW Consulting report contains the granular scenario tables, regional and application splits, and vendor scorecards that operational teams rely on to execute contracts and capital plans with confidence.

To convert market insight into procurement advantage — from specification language to lifecycle modeling and vendor negotiation playbooks — engage PW Consulting for a tailored briefing and the complete report package.

For detailed analysis of this topic, please visit the official page:Automatic Transfer Switches Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com