Building Management System Market: Strategic Imperatives for 2026 Decision‑Makers

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present an executive primer for executives, investors, and technical leaders preparing to make consequential decisions in 2026. Our latest Building Management System (BMS) Market study synthesizes five years of historical performance with forward-looking scenario analysis, demonstrating how a fast‑maturing, regulation‑intensive market will reshape product roadmaps, capital allocation, and go‑to‑market strategies over the 2026–2032 forecast horizon.

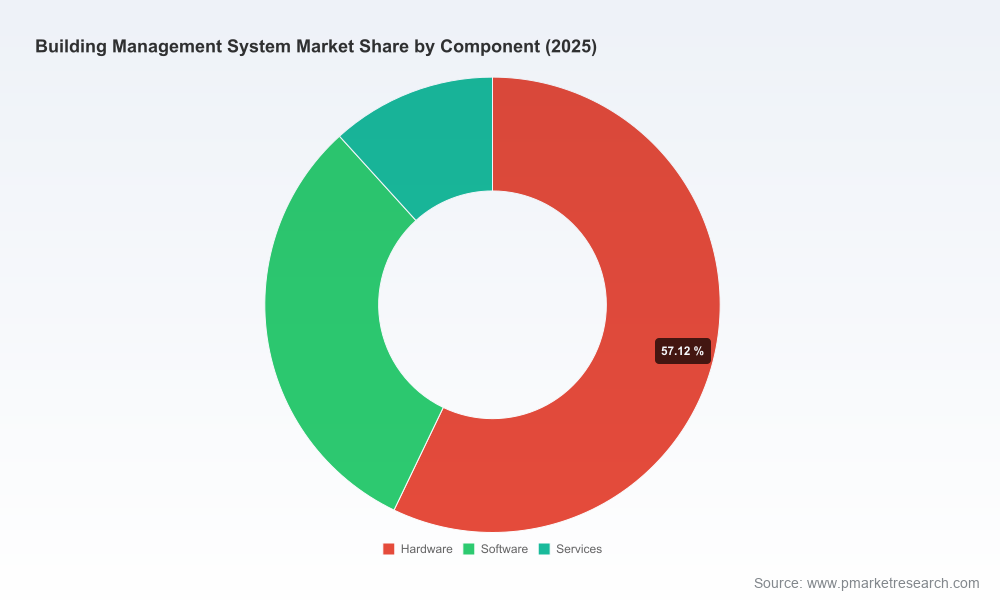

Building Management System Market

Market trajectory at a glance

The BMS market has moved from an early‑adoption phase into a scaled growth cycle. Our base‑year analysis shows the market expanding steadily between 2020 and 2025, and the forecast indicates sustained acceleration through 2032 at a compound annual growth rate of 14.87%. The scale and momentum implied by this trajectory are not academic: they translate directly into addressable revenue pools for software publishers, hardware vendors, service integrators, and systems‑level platform players—and into practical implications for capex cycles, retrofit programs and software subscription strategies.

Building Management System Market

Why this study matters for 2026 decisions

- Regulatory demand is forcing architecture choices. New European and U.S. rules advancing life‑cycle carbon accounting, stricter energy performance calculation methodologies, and tax incentives tied to BMS integration mean compliance is now a product and procurement requirement—not a feature. Organizations that bake compliance into their early design and procurement choices will avoid expensive retrofits and capture incentive value.

- Procurement and financing windows are tightening. With energy regulations and incentive programs moving quickly, procurement teams face compressed decision cycles. Vendors that can offer measurable compliance pathways, predictable TCO outcomes and subscription/licensing flexibility are advantaged.

- Technology convergence changes partnership economics. IoT, AI, edge analytics and cloud orchestration are blurring lines between hardware vendors, software publishers and service providers. The winners will be those who combine interoperable platforms with outcome‑focused services and scalable security models.

- Retrofit opportunity equals operational complexity. The bulk of near‑term revenue growth will be tied to modernization of existing assets rather than greenfield projects. That creates large install‑base monetization potential—but also elevates integration risk and demand for modular upgrade paths.

What the PW Consulting BMS report delivers (practical, decision‑grade outputs)

- Transparent market sizing and growth model covering 2020–2025 historicals and 2026–2032 forecasts, including sensitivity scenarios that isolate regulatory, technology and macroeconomic impact vectors.

- Vendor benchmarking and strategic profiles that map product architectures (edge/cloud balance, openness, device scale), go‑to‑market models (hardware sales, SaaS, managed services) and M&A posture.

- Actionable procurement and implementation playbooks—vendor selection scorecards, retrofit risk matrices, and a TCO model you can adapt to your portfolio.

- Regulatory impact assessment tied to regional policy levers, fiscal incentives and compliance timelines, with recommended compliance roadmaps for building owners and developers.

- Technology deep dives on AI analytics, wireless sensor economics, cybersecurity frameworks and interoperability standards, plus implementation checklists for phased migrations.

- Proprietary scenarios modeling energy savings, capex/opex tradeoffs and payback profiles to support executive investment cases.

Note: this primer intentionally highlights strategic themes and methodology. The full report contains granular segmentation and regional/application splits, detailed vendor scorecards and downloadable datasets to support transaction diligence and procurement negotiations.

Building Management System Market

Competitive landscape — themes and positional analysis

The competitive field in BMS is diverse: global incumbents with broad industrial footprints, specialized automation vendors, and emerging software‑centric challengers. Market concentration metrics indicate a moderate degree of top‑tier influence, but not absolute dominance—creating space for mid‑market players and focused specialists to scale via differentiated offerings and services.

- Johnson Controls (Metasys) — Leverages an open building automation architecture that emphasizes large‑scale device aggregation and integrated energy intelligence. Recent platform updates increase scalability and resilience, making it a default choice for large portfolios seeking standardized control layers.

- Schneider Electric (EcoStruxure) — Positions a comprehensive ecosystem that integrates HVAC, security, power management and microgrids. Recent moves toward subscription licensing and digital‑first services signal a deliberate push from product sales to recurring revenue and centralized software management.

- Honeywell (Forge and EBI) — Focused on AI‑enabled operational platforms for real‑time performance optimisation. Investments in connected solutions and analytics make Honeywell a contender where operational intelligence and digital twin capabilities are priorities.

- Siemens (Desigo CC) — Offers a unified control environment and strong digital infrastructure components, appealing to customers prioritizing system unification and enterprise‑grade integration.

- Trane, ABB, Carrier, Bosch, Legrand, Emerson, Delta, Azbil, Hitachi — Each brings differentiated strengths across HVAC optimisation, power monitoring, electrical integration and regional channel depth. Their approaches range from tightly bundled hardware/software propositions to platform‑agnostic services and cloud integrations.

Recent product and service launches across suppliers illustrate a clear market inflection toward scalable software platforms, managed services and subscription licensing—an evolution that favors vendors who can demonstrate customer outcomes (energy savings, compliance, uptime) rather than only device functionality.

Technology and deployment trends to prioritize in 2026

- Edge‑to‑cloud architectures: Scalable edge controllers combined with cloud orchestration balance latency, resilience and centralized analytics. This hybrid topology supports both real‑time control and enterprise reporting.

- AI and predictive operations: Embedded analytics are shifting the value proposition from monitoring to prescriptive actions that reduce energy use and maintenance costs.

- Wireless sensor economics: Wireless networking is materially lowering infrastructure costs for sensors and controls in commercial retrofits—changing the business case for wide‑scale occupancy and environmental monitoring.

- Security and open APIs: As systems integrate with corporate IT and OT stacks, cybersecurity and well‑documented APIs are minimum viability attributes for platform adoption.

- Service‑led monetisation: Digital‑first service offerings (predictive maintenance, 24/7 monitoring, performance guarantees) are becoming the fastest route to recurring revenues and customer stickiness.

Concrete examples of these trends are visible in industry activity: major vendors have introduced scalable, multi‑server and IP‑dense platform releases; AI‑driven building management suites have moved from pilots to product launches; and subscription/service bundles are being rolled out as primary commercial models.

Five strategic moves for executives in 2026

- Reframe product roadmaps around outcomes. Shift R&D and GTM focus from features to measurable outcomes—energy reduction, compliance readiness, uptime guarantees—and price accordingly (performance‑based contracts, outcome SLAs).

- Invest in interoperability and security early. Make open APIs, standardized data schemas and end‑to‑end cybersecurity foundational requirements for partnerships and customer deployments.

- Build a retrofit playbook. Create modular upgrade packages, financing options and rapid‑deployment sensor kits to capture the retrofit opportunity with predictable ROI for customers.

- Move to subscription and managed services. Where feasible, convert hardware margins into recurring software and service revenue through subscription licensing, digital maintenance offers and outcome‑based services.

- Use scenario modeling for regulatory risk. Run policy‑sensitivity scenarios in capital planning to quantify incentives, compliance timing and potential penalty exposure—then align procurement timing to exploit fiscal windows.

Concluding perspective and next step

The 2026 inflection in the BMS market rewards clarity of strategy: vendors and customers who navigate regulatory pressure, adopt cloud‑edge AI architectures, and pivot to service‑centric commercial models will extract disproportionate value from the growth runway. The data and scenarios in our report convert market momentum into transactional insight—supporting vendor selection, product prioritization and investment cases.

To access the full dataset, granular segmentation (by component, type, application and region), detailed vendor scorecards and our interactive financial models, consult the PW Consulting report page. The downloadable annex contains the exact forecasting assumptions, scenario worksheets and a procurement checklist you can apply directly to your 2026 planning cycle.

For detailed analysis of this topic, please visit the official page:Building Management System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com