Modified Wood Market 2026: Strategic Imperatives from PW Consulting

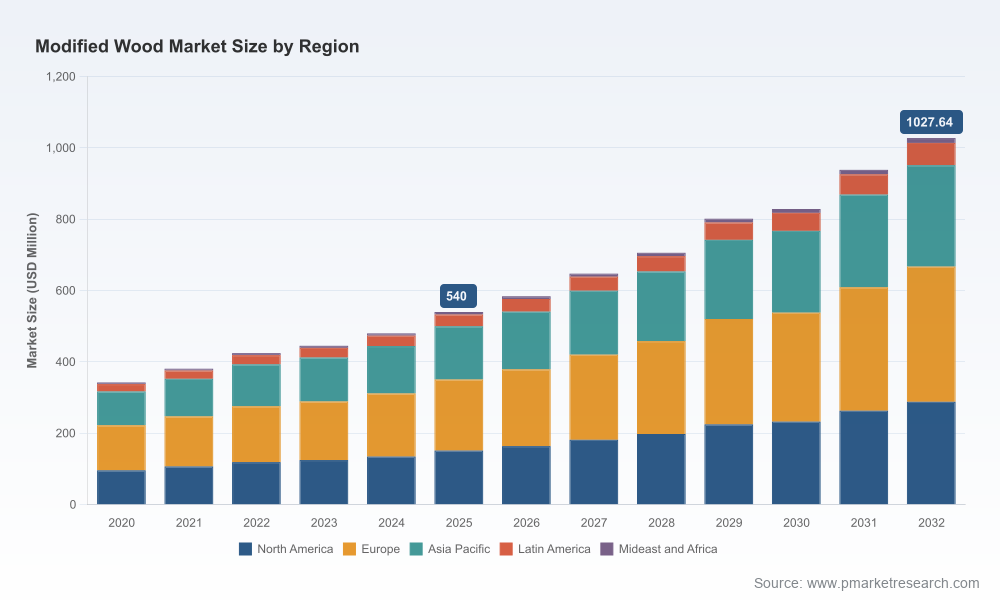

As companies prepare budgets, capital plans, and go-to-market strategies for 2026, the modified wood sector presents a rare combination of robust growth and tactical complexity. PW Consulting’s latest market study — anchored on a 2025 base year and extending forecasts through 2032 — shows a market that expanded from roughly USD 342.5 million in 2020 to USD 540.0 million in 2025 and is projected to exceed USD 1.0 billion by 2032, growing at a compound annual rate of 9.7%. This preview explains why that trajectory matters, what strategic decisions it should trigger across the value chain, and what actionable intelligence you will unlock by accessing the full report.

Modified Wood Market

Why this research matters for 2026 decision-makers

- Investment timing and sizing: A near-term step-up in demand and sustained mid-term growth at a high single-digit CAGR compresses the window for capacity investments and M&A to secure feedstock, IP, and channel access.

- Risk management: Trade-policy volatility (notably U.S. softwood tariff dynamics) and feedstock availability create asymmetric downside for market entrants that do not hedge supply or diversify production footprints.

- Product and commercial strategy: Differentiation through chemical-free thermal processes, patented acetylation, extended warranties, and sustainability credentials increasingly mediates price realization and channel acceptance.

- Procurement and cost control: Control points in raw-material chemistry and logistics (for example, access to acetic anhydride streams, or optimization of thermal-modification kilns) materially affect gross margins.

What the full report delivers — practical, monetizable outputs

- Validated market sizing & forecast: Historical time series (2020–2025) and scenario-driven forecasts to 2032 with sensitivity to price, feedstock constraints, and trade-policy shocks.

- Segmentation and growth pockets: Multi-dimensional segmentation by region, product type, and application, with growth elasticity models and demand drivers mapped for each node. (Note: detailed split tables are intentionally withheld in this preview.)

- Competitive maps and capability matrices: Comparative analysis of process IP, warranties, certifications, and production footprints for incumbent and emerging players.

- Raw-material and cost base analysis: Feedstock flows and price drivers, including chemical inputs for acetylation, thermal-energy costs, and logistics. We model chemical-recycling levers and substitute feedstocks.

- Regulatory and trade impact modeling: Quantified P&L sensitivity to tariff escalations and regional regulatory shifts, with mitigation playbooks for different exposure profiles.

- Go-to-market & distribution diagnostics: Channel economics for builders, distributors, and specification channels, plus strategies to accelerate adoption among architects and large-volume contractors.

- M&A and partnership roadmaps: Valuation ranges, synergy capture models, and prioritized target lists by strategic rationale (feedstock, IP, market access).

- Tools and deliverables: Interactive Excel models, scenario dashboards, executive slide decks, and a set of 10 operator-level implementation checklists.

Competitive dynamics — the players and what to watch

The sector’s competitive topology is defined by technology diversity (thermal modification vs. acetylation vs. hybrid treatments), certification and warranty claims, and geographic production footprints. Key incumbents exemplify different strategic positions:

Modified Wood Market

- Accoya (Accsys Technologies): The global leader in acetylated wood operates a patented chemical-modification process that confers long-term durability and dimensional stability — characteristics that underpin premium pricing and specification in high-value exterior and structural applications. Vertical control over chemical inputs and the ability to re-use acetic acid streams are meaningful margin and sustainability advantages.

- Thermowood specialists (Thermory, Lunawood, SWM-Wood, Novawood, Karava): These producers leverage chemical-free heat-and-steam processes and long-established product families for cladding, decking, and interiors. Their strengths are brand recognition in architectural channels, distributed production in Europe (and in some cases the U.S.), and product portfolios tailored to local timber supplies.

- Kebony: Differentiates via a bio-based ‘dually modified’ process that achieves tropical-hardwood performance without harmful chemicals — a strong positioning in sustainability-conscious markets and for green procurement mandates.

- Arbor Wood Co. and specialized U.S. producers: Domestic Thermowood certification and local production allow these firms to capture builders and specifiers seeking U.S.-sourced compliance and shorter lead times; Arbor’s acceptance into the International ThermoWood® Association in mid‑2025 is a case in point.

Complementary to these producers, the channel and distribution landscape is evolving: recent product launches and distribution alliances show firms moving to broaden assortments and accelerate market penetration. Examples we track include new thermally modified siding and decking lines from specialty millwork brands, strategic distribution partnerships to combine processing technology with national networks, and supplier network expansions to address availability constraints.

Modified Wood Market

Market structure and strategic implications

The modified wood market remains commercially attractive but structurally fragmented. Market concentration is low relative to heavy industrial commodities, meaning national and regional players retain outsized influence in local channels. For established firms, this creates room to extract premium pricing through brand, warranty, and spec-driven channels. For new entrants, the barriers are technological IP, certification, and securing stable feedstock and chemical inputs.

Two external factors will disproportionately affect 2026 outcomes:

- Trade policy shifts: Current U.S. softwood measures impose a material tariff that raises landed costs for some imports; potential escalations scheduled for 2027 could further compress margins for import-dependent models. Strategic response options include relocating processing, securing tariff-exempt supply corridors, or moving upstream into raw-timber procurement.

- Raw-material and chemical supply chains: For acetylation-based producers, access to acetic anhydride and the operational capability to recycle acetic acid byproducts are critical operational levers. For thermal-process producers, access to consistent softwood feedstocks and energy-efficient kilns dominates unit economics.

2026 playbook — prioritized actions by stakeholder

- Manufacturers: Lock in feedstock contracts with staged take-or-pay clauses; invest in certification and warranty programs that shorten sales cycles with architects and large specifiers; evaluate near-market micro-facilities to hedge tariff risk.

- Distributors & builders: Diversify supplier panels to include chemically modified and thermally modified options; negotiate volume-based price collars; co-develop specification guides and warranty-backed test cases for large projects.

- Investors & acquirers: Prioritize targets with proprietary process IP (or long-term supply agreements), low-cost feedstock access, and established distribution partnerships. Use scenario-based valuation that stresses tariff and feedstock shocks.

- Raw-material/chemical suppliers: Expand recycling capabilities and partner on feedstock integration to capture downstream value; offer bundled supply-and-technical-support contracts for acetylation customers.

- Architects & specifiers: Demand transparent lifecycle and maintenance data; prioritize suppliers with long-form warranties and verifiable sustainability certifications.

What we deliberately withhold here — and why you should download the full study

This introduction demonstrates the analytical framework and strategic insights embedded in PW Consulting’s full report. To preserve the commercial value of our primary analysis and to encourage direct engagement, we have not reproduced detailed regional, type, and application splits in this preview. The full study provides those granular tables, downloadable models, and interactive dashboards so you can:

- Drill into regional demand trajectories and assess market share opportunities at country level;

- Compare unit-cost curves across thermal and acetylation processes under multiple energy-price scenarios;

- Evaluate application-level growth (decking, cladding, siding, fenestration) with pricing and margin ladders;

- Access company-level revenue estimates, production capacities, and licensing footprints that support M&A due diligence.

Next steps

For executives preparing 2026 strategies, the decision levers are clear: secure feedstock and chemical inputs, defend and grow specification channels through certification and warranty differentiation, and structurally de-risk exposure to trade-policy shocks via footprint diversification. PW Consulting’s full Modified Wood Market study delivers the granular, model-driven intelligence to quantify these choices and to convert them into board-level investment decisions and operational plans. Visit our release page to download the full report, interactive models, and a tailored briefing kit for leadership teams.

For detailed analysis of this topic, please visit the official page:Modified Wood Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com