Spices and Seasonings Market 2026: Strategic Preview for Executive Decision-Making

Executive summary

PW Consulting’s new industry briefing frames the spices and seasonings market as a structurally growing, strategically complex sector entering 2026 from a solid empirical base. With 2025 as the base year and a forecast horizon to 2032, the global market is projected to grow at a steady compound annual growth rate of 5.5%. Our topline projections show the sector expanding from approximately USD 26 billion in 2025 toward the high-30s by the end of the forecast period, underscoring resilient consumer demand, rising premiumization, and expanding application across food categories.

Spices and Seasonings Market

This article functions as a strategic “trailer”: we surface the most consequential trends, competitive moves, regulatory shocks and decision levers that will shape 2026 execution, while intentionally omitting the granular segmentation tables and model outputs that are available in the full report.

Spices and Seasonings Market

Why this research matters for 2026 decisions

- Timing: 2026 is a pivot year for companies deciding where to allocate capital — between near-term margin defense (input-cost pass-through, efficiency) and longer-term growth (innovation, emerging-market penetration).

- Signal-to-noise: Supply disruptions, food-safety incidents and rapid ingredient-cost cycles are increasing the value of forward-looking scenario analytics and supplier-level stress tests.

- Competitive inflection: Market concentration shows a modestly consolidated landscape — the leading firms maintain scale advantages, but there is material room for insurgent strategies focused on flavor innovation, clean-label credentials and regional specialization.

What the full PW Consulting report delivers (practical contents)

- Topline market sizing and a 2026–2032 forecast built on an integrated demand model that fuses household consumption patterns, foodservice flows and industrial offtake.

- Scenario-ready supply-chain maps and supplier risk heatmaps down to production origin (multi-supplier strategies, crop-season windows, freight exposure).

- Commercial playbooks: go-to-market templates for premiumization, private label, and co-manufacturing across retail, foodservice and industrial channels.

- Regulatory and quality-impact assessments including likely inspection vectors and compliance cost scenarios tied to EFSA/RASFF and FDA trends.

- Competitive diagnostics: capability matrices for the sector’s strategic players, plus M&A screening criteria and value-creation blueprints for potential bolt-on acquisitions.

- Actionable KPIs and sample P&L sensitivity models to stress-test pricing strategies under different raw-material and logistics cost regimes.

- Primary research inputs: interviews with manufacturers, spice grinders, global traders, major retailers and quality laboratories, supplemented with proprietary transaction analytics.

Market dynamics: what’s driving growth and disruption

Growth is being driven by three structural forces: culinary premiumization (consumers trading up to heritage and single-origin spices), convenience-led demand (seasoning blends, meal kits and prepared foods), and industrial expansion (processors embedding flavor systems in a wider set of categories). These forces are supported by favorable macro tailwinds but moderated by cyclical pressures on agricultural commodity prices and freight.

Spices and Seasonings Market

At the same time, regulatory scrutiny has intensified. European authorities have repeatedly flagged spices and herbs as a high-risk category in rapid alert systems, and recent enforcement activity shows a non-trivial proportion of analyzed samples facing adulteration or undeclared allergen findings. In parallel, U.S. import controls and focused FDA inspections add a layer of compliance cost and entry friction for exporters. For 2026, companies must factor higher testing frequencies, traceability investments and potential delays at customs into their operational plans.

Competitive landscape: strategic postures and implications

- McCormick & Company: The dominant global flavor house combines consumer brands and B2B solutions. Its increased control in Latin America (recent stake change in a regional subsidiary completed in early 2026) signals a strategic push to consolidate sourcing-to-distribution and to accelerate tailored portfolio plays in growth markets. For peers, McCormick’s move raises the bar for scale-driven cost efficiency and local-market integration.

- Olam International: As a large-origin and ingredient supplier, Olam’s strength is upstream control and logistic capability. Its positioning is attractive to manufacturers seeking supply continuity and transparent origin narratives. Contracts and long-term offtake structures with origin suppliers are likely to increase.

- Kerry Group: Kerry operates at the intersection of flavor and nutrition, playing to premiumization and clean-label transition through customized seasoning systems. Its R&D-led model is a template for players pursuing higher-margin, co-created formulations with industrial clients.

- The Kraft Heinz Company: With scale in branded condiments and ingredient solutions, Kraft Heinz leverages customer reach and marketing to drive shelf innovation; its orientation illustrates the value of combining branded demand stimulation with ingredient-level margin capture.

- Sensient Technologies and Kalsec: These companies exemplify the move toward extract-based, natural solutions and functional spice derivatives — a competitive axis that favors firms able to commercialize standardized, clean-label extracts at scale.

- Fuchs Gruppe, Paulig and Associated British Foods: These regional champions and diversified food companies demonstrate alternative GTM strategies — focused portfolios, brand partnerships and strong private-label channels that can outcompete on service and customization rather than pure price.

Regulatory and safety environment — immediate operational impacts

Recent oversight activity by European agencies and the FDA has concrete implications: expect increased laboratory testing budgets, more conservative supplier acceptance protocols, and potentially longer lead-times for new-supplier qualification. A non-trivial share of herb and spice samples have been highlighted for adulteration and undeclared substances in recent rapid alert reports, elevating the commercial value of validated traceability and chain-of-custody documentation.

Strategic playbook for 2026 (what smart executives will do)

- Re-prioritize supply resilience: Implement multi-layered sourcing strategies (dual-sourcing, crop forward contracts, origin diversification) and segment SKUs by risk profile. Build inventory buffers for high-risk crops and deploy financial hedges where available.

- Invest in traceability and testing: Short-term investments in third-party laboratories, on-the-ground audits and digital traceability (blockchain pilots or serialized QR code systems) reduce recall exposure and open premium shelf opportunities.

- Accelerate clean-label and extract innovation: Allocate R&D to scalable natural extracts and flavor systems that meet clean-label demands without sacrificing cost discipline; consider JVs with extract specialists to shorten time to market.

- Commercial segmentation and value capture: Differentiate go-to-market by channel — premium branded propositions in retail, cost-optimized blends for private label, and bespoke systems for industrial clients. Use data-driven pricing to capture input-cost swings selectively.

- M&A and partnership hunting: Pursue bolt-on acquisitions in origin markets, testing and extract capabilities; prioritize targets that provide vertical integration benefits or proprietary flavor assets.

- Regulatory readiness as a strategic asset: Convert compliance investments into commercial differentiators — market “tested and compliant” product lines to risk-averse retailers and export customers.

- Operational digitization: Use demand-sensing, order-to-manufacture synchronisation and supplier risk dashboards to reduce working capital and improve fill rates under volatility.

Decision frameworks and KPIs to adopt in 2026

- Short-term: days of cover by crop and SKU, supplier concentration by spend, testing-fail rate trends, customs-delay days.

- Medium-term: revenue share of premium/clean-label SKUs, margin spread between branded vs. B2B flavors, payback period for traceability investments.

- M&A lens: accretion on EBITDA, synergies by logistics consolidation, origin vs. processing arbitrage.

What we are intentionally withholding (and why)

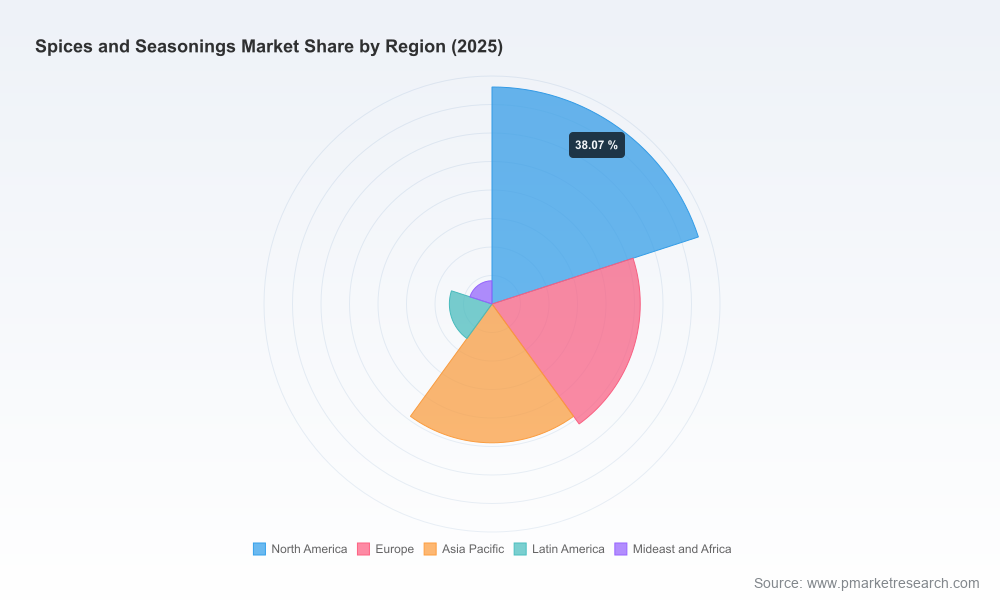

To preserve the strategic value of our primary analysis and to encourage direct engagement, we have not reproduced the granular regional or application-level percentage splits, SKU-level revenue tables, or the full model outputs in this preview. These detailed segmentations, supplier-level risk assessments and downloadable financial models are available in the full PW Consulting Spices and Seasonings Market report and accompanying data pack.

Next steps for executives

Use the next 60–90 days to align capital allocation with the risk scenarios outlined here: shore up high-risk supply lines, accelerate traceability pilots, and prioritize one or two strategic M&A or partnership plays that close capability gaps (origin control, testing, extract technology). Assign a cross-functional team to convert the high-level playbook above into a 100-day action plan — with clear owners, budgets and stage gates. For companies contemplating major portfolio moves, run our sample P&L sensitivity templates against your own SKU set to quantify trade-offs between margin defense and growth investments.

How to access the full intelligence

The full PW Consulting report contains the proprietary models, segment and regional breakout tables, supplier heatmaps, and step-by-step commercial playbooks referenced in this preview. Organizations seeking to operationalize these findings — through custom scenario runs, target-screening for M&A, or traceability implementation roadmaps — should contact PW Consulting to obtain the complete dataset and our tailored advisory engagement options.

For detailed analysis of this topic, please visit the official page:Spices and Seasonings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com