Material Jetting in 2026: Strategic Imperatives from PW Consulting’s Market Preview

As PW Consulting’s lead industry analyst, I present a concise, decision-focused introduction to our new Material Jetting (MJ) Market study. This briefing is designed as a strategic “trailer” — to surface the critical trends, risks, and commercial questions that every executive facing 2026 planning cycles should resolve — while preserving the proprietary subsegment tables and granular forecasts that materially alter vendor selection, capex timing, and go-to-market tactics. If you want the full set of segmented scenarios, supplier shares, and price curves, the complete report and datasets are available on our source page.

Material Jetting (MJ) Market

Why Material Jetting matters to corporate strategy in 2026

Material Jetting has transitioned from an R&D and low-volume prototyping technology to a capability that influences product design cycles, regulatory pathways, and short-run production economics. Our market model (base year 2025) shows an established revenue base and a sustained compound annual growth rate (CAGR) of 8.45% across the 2026–2032 forecast horizon. This trajectory reflects a combination of incremental material innovation, increasing acceptance in regulated healthcare applications, and selective industrial deployments where multi-material, high-resolution outputs provide unique value.

Material Jetting (MJ) Market

- Portfolio managers: MJ can reduce time-to-validated prototypes and accelerate product iterations — but not uniformly. Adoption choices materially affect R&D calendar and inventory strategies.

- Operations leaders: MJ’s high-resolution, multi-material capability changes assembly and secondary-process needs (e.g., fewer assembly steps for multi-material components), which impacts capacity planning and sourcing.

- Commercial and regulatory teams: The technology’s adoption in medical and dental use-cases introduces compliance pathways that must be actively managed, not assumed.

Market trajectory — what the macro numbers imply for 2026 decisions

Between our historical window and the forecast, the MJ ecosystem demonstrates steady expansion, driven primarily by improvements in photopolymer performance and system-level usability. The reported CAGR of 8.45% is not merely a vanity metric; it translates into persistent investment opportunities across materials, service bureaus, and appliance manufacturers. For budget cycles starting in 2026, that means:

Material Jetting (MJ) Market

- Capex timing matters. Buyers that postpone investments risk higher acquisition costs in later phases of the cycle and loss of early-mover benefits in regulated verticals.

- Vendor selection is strategic. Given the technology’s rapid material evolution, choosing a supplier with a clear roadmap for material compatibility and qualifications (e.g., biocompatible or durable materials) reduces rework and certification risk.

- Service-layer economics will expand. As printers become more capable, the most attractive opportunities will shift to value-added workflows (post-processing, certification, and digital inventory services) rather than hardware alone.

Operational realities and structural constraints

Data from sector analyses and standards bodies shows that MJ’s strengths are offset by pragmatic constraints that influence adoption speed and return on investment:

- Material economics: Resins for MJ systems are materially more expensive than comparable photopolymers used in other additive processes. This cost delta must be accounted for in part-cost models and total cost of ownership (TCO) calculations.

- Throughput trade-offs: Process speed limitations, documented in industrial studies, mean MJ often has higher per-part production times compared with some powder-bed technologies. This converts into different capacity planning and labor models.

- Regulatory momentum: Regulatory bodies in healthcare have cleared an increasing number of 3D-printed devices, and MJ is frequently cited for high-precision and biocompatible outputs. For regulated-product teams, this creates both an opportunity (faster clinical model availability) and an obligation (maintaining validated material/process chains).

- Adoption barriers for smaller firms: Cost of ownership — both capital and consumable — remains a major inhibitor for small manufacturers, necessitating alternative go-to-market strategies (partnerships, outsourced production, or print-as-a-service models).

What the PW Consulting report delivers — practical, executable content

We designed the report as an operational playbook for 2026 decisions. Highlights include:

- Decision frameworks: Buyer personas and procurement checklists that map capability needs to printer classes, material families, and process validation requirements.

- Investment scenarios: Three granular capex/timing scenarios that show NPV-sensitive breakpoints for internal production versus outsourcing across different volumes and part complexities.

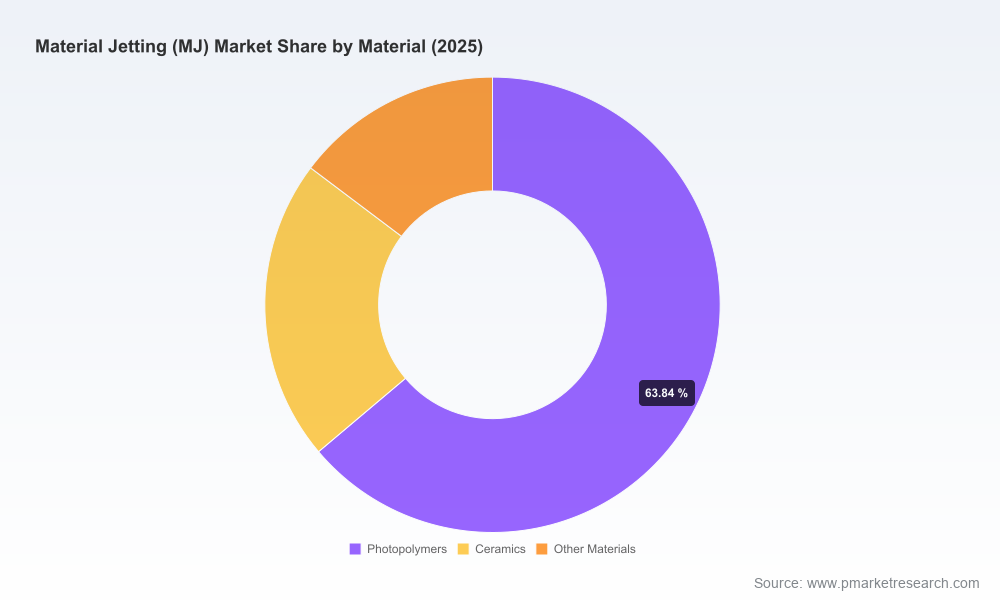

- Material and process playbooks: Qualification roadmaps for common photopolymers and ceramic blends — including suggested test matrices to accelerate internal validation.

- Supplier engagement guide: Tender templates, evaluation scorecards, and a negotiation primer focused on service-level agreements (SLAs) for consumables and on-site support.

- Regulatory and quality checklist: A compliance starter pack for medical and dental applications, highlighting documentation, traceability, and material control best practices.

- Scenario-based risk models: Sensitivity analyses that show how changes in resin prices, throughput, and regulatory timelines shift the production case for MJ versus alternative AM technologies.

Competitive landscape — what incumbent and challenger moves mean for buyers

The MJ supplier landscape blends long-established AM vendors and focused specialists. In our work, we profile the market participants most relevant to strategic buyers and map their strengths by technology, material roadmap, and service orientation.

- Stratasys Ltd. (Israel) — Known for PolyJet and the J-series family, Stratasys continues to push the functional-prototype and multi-material envelope. Recent product moves in April 2026 — including the launch of new ToughONE materials and the J850 Core platform — signal a deliberate product stratification: premium, feature-rich systems for advanced users, and lower-cost cores for engineering teams that need functional prototyping without the premium feature set.

- 3D Systems Corporation (United States) — With its ProJet lineage, 3D Systems remains a strong contender for high-resolution prototypes and select end-use parts. Their emphasis on integrated software and validated material-process stacks helps reduce qualification timelines for regulated customers.

- HP Inc. (United States) — HP’s approach blends MJ photopolymer systems with industrial Multi-Jet Fusion strategies. Their scale and service infrastructure make them an attractive option for manufacturers who plan to bring short-run production in-house at scale.

- Vader Systems (United States) — As a smaller, specialized player, Vader focuses on multi-material and multi-color MJ innovations. These niche capabilities can be decisive in consumer-facing and design-led product segments.

- Xjet Ltd. (Israel) — Xjet’s high-resolution solutions are positioned where surface quality and fine feature fidelity are non-negotiable. Their systems are often chosen when aesthetic or precision tolerances are critical.

- EnvisionTEC GmbH (Germany) — EnvisionTEC bridges stereolithography and MJ capabilities, appealing to dental and jewelry applications that require both fine detail and material-specific performance.

For decision-makers, the key takeaways are: match supplier roadmap to your validation horizon; differentiate between vendors offering material breadth versus those offering process control and certification support; and anticipate bundled services (consumables + software + maintenance) as the locus of future vendor differentiation.

Strategic playbook for 2026 — five recommended actions

- Run a 12-month qualification sprint for mission-critical parts. Use a compact test matrix that prioritizes material compatibilities and sterilization/biocompatibility where applicable.

- Adopt a hybrid sourcing model. For most organizations, a mix of strategic in-house capacity and third-party production will minimize risk while enabling learning and capability build-out.

- Negotiate SLAs that include consumable pricing bands and upgrade pathways. Consumable cost volatility is a primary margin lever and should be contractually addressed.

- Invest in post-processing and inspection tooling. High-resolution prints demand commensurate secondary processes to achieve repeatable quality at scale.

- Embed regulatory and quality teams early. For any application moving toward end-use or clinical deployment, regulatory validation drives timelines and must be resourced upfront.

Risks and watch items

- Consumable price shocks — given the higher relative cost of MJ resins — can erode planned unit economics; hedging strategies or long-term supplier agreements can mitigate such shocks.

- Throughput constraints — process speeds may be a gating factor for specific part families; alternative AM pathways should be modeled concurrently.

- Vendor consolidation or IP shifts — new material launches and platform expansions (like the April 2026 Stratasys moves) can quickly change competitive dynamics; remain agile in supplier governance.

How to use this preview and next steps

This article is a strategic orientation intended to accelerate your 2026 decision cycle. PW Consulting’s full MJ Market report includes the detailed segmentation, regional and application splits, supplier market shares, price curves, and downloadable model files that procurement, engineering, and regulatory teams need to execute confidently. The full analysis also contains actionable annexes — including a procurement RFP pack and a 36-month implementation roadmap tailored for enterprise rollouts.

If your 2026 plan includes material investments, supplier consolidations, or new product launches that depend on additive manufacturing, treat this preview as your early-warning system. The complete dataset and deep-dive chapters are available through our report page; access will provide the granular metrics you will require to finalize budgets and supplier commitments.

PW Consulting remains available to run tailored workshops, vendor due-diligence sessions, and TCO stress-tests to translate these insights into an executable 2026 strategy.

For detailed analysis of this topic, please visit the official page:Material Jetting (MJ) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com