Capacitance Diaphragm Vacuum Gauges Market: A Strategic Primer for 2026 Decision-Making

As companies position themselves for the next wave of capital allocation, product development, and M&A activity, a crisp understanding of the capacitance diaphragm vacuum gauges market is no longer optional — it is strategic. This primer, prepared by PW Consulting’s senior strategy and industry analysis team, synthesizes the market’s trajectory, competitive dynamics, regulatory contours, and practical implications for executive decisions in 2026. It deliberately showcases analytical depth while preserving the detailed sub-segmentation and proprietary tables found in the full report — a focused “trailer” designed to build confidence and drive readers to the complete dataset and playbooks.

Capacitance Diaphragm Vacuum Gauges Market

Market at a glance — what the numbers tell us

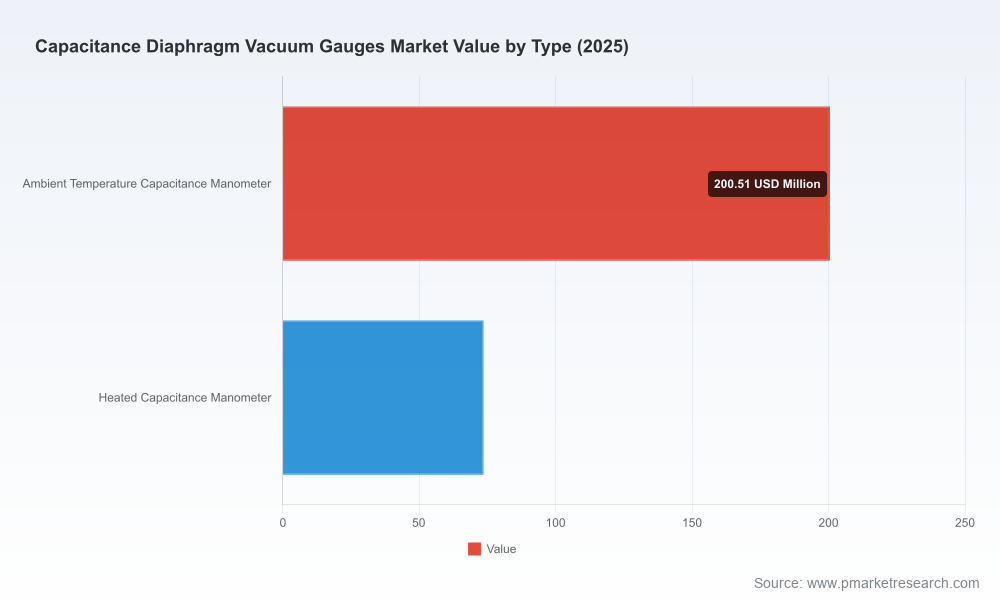

The market for capacitance diaphragm vacuum gauges has demonstrated steady expansion through the early 2020s and remains on a growth path as of 2026. On a macro basis, PW Consulting’s model shows the market expanding from a multi-hundred-million-dollar base in 2020 to an estimated figure in 2025, with the base-year for our study set at 2025. Looking forward, the market is projected to grow at a compound annual growth rate (CAGR) of approximately 4.05% over the 2026–2032 forecast window, culminating in a larger market size by 2032. These headline trajectories reflect durable demand across semiconductor manufacturing, industrial vacuum systems, advanced coatings, and research instrumentation.

Capacitance Diaphragm Vacuum Gauges Market

Two structural features are central to understanding near-term opportunities and risks. First, product differentiation around temperature compensation, gas-independent absolute pressure measurement, and corrosion-resistant materials is driving purchasing decisions in critical end-markets. Second, market concentration is material: the three largest suppliers account for a clear majority of revenues, while the top five suppliers capture an even larger share — a dynamic that shapes pricing power, channel strategies, and M&A signaling.

Capacitance Diaphragm Vacuum Gauges Market

Key demand drivers shaping strategy in 2026

- Semiconductor process intensity: Continued node development and integration of high-value packaging processes sustain demand for high-accuracy, gas-tolerant gauges in vacuum furnaces and etch/CVD environments.

- Process integrity and yield economics: As fabs push for tighter process windows, measurement certainty (absolute, gas-independent pressure) becomes a lever for yield improvement and cost reduction.

- Materials and high-temperature processes: Adoption of ceramic and sapphire diaphragm technologies for corrosive and high-temperature processes is accelerating demand for heated and high-temp tolerant gauge variants.

- Aftermarket and service growth: Lifecycle service, calibration, and instrument retrofits provide recurring revenue opportunities as installed bases age and fabs expand.

Competitive landscape — what leading suppliers are doing

The market features established instrument OEMs, specialized component manufacturers, and a set of regional players focused on customization. Key firms included in our competitive coverage are MKS Instruments, INFICON, Agilent Technologies, Pfeiffer Vacuum, Setra Systems, Kurt J. Lesker, Leybold, Edwards Vacuum, ULVAC, Nor-Cal Products, Canon Anelva, Azbil Corporation, and InstruTech. Their positioning can be summarized as follows:

- MKS Instruments (Andover, MA): A recognized leader with the Baratron family that emphasizes temperature compensation and high absolute accuracy for fabs and vacuum tool OEMs. MKS’s scale and channel relationships make it a bellwether for pricing and spec trends.

- INFICON (Bad Ragaz, Switzerland): Known for temperature-compensated and ceramic-based gauge variants designed for corrosive, high-temperature semiconductor processes. Recent product introductions reinforce INFICON’s focus on process-specific robustness.

- Agilent Technologies (Santa Clara, CA): Provides high-accuracy gauges targeted at precision process control and research environments, with a strong brand presence in laboratory and fab instrumentation.

- Pfeiffer Vacuum & Edwards Vacuum: European leaders with broad vacuum portfolios; they emphasize compatibility with corrosive gas handling and comprehensive support for industrial vacuum processes.

- Mid-sized and specialized players (Setra, Kurt J. Lesker, Leybold, ULVAC, Nor-Cal, Canon Anelva, Azbil, InstruTech): These firms compete on niches — from custom solutions to regional service and integration capabilities — and are often the preferred suppliers for custom OEM builds or retrofit projects.

Strategically, large suppliers leverage breadth and scale to lock in OEM and aftermarket contracts, while specialist players differentiate on engineering depth, rapid customization, and regional service. These dynamics suggest distinct playbooks for incumbents versus challengers: incumbents should protect margin by expanding services and platform standardization; challengers should pursue product-led differentiation and co-development partnerships with OEMs.

Recent industry moves and regulatory context

- Product innovation continues: INFICON launched a SKY ceramic capacitance diaphragm gauge tailored to high-temperature, corrosive semiconductor processes in early 2024 — a development that validates demand for materials-engineered solutions.

- Performance standards and quality systems: Several market leaders offer products and processes that meet stringent quality and accuracy standards (for example, ISO 9001 and product-level specifications targeting sub-0.1% full-scale accuracy and robust temperature compensation). Compliance and traceability are de facto purchasing criteria in high-value fabs.

- Process safety and handling: Leading suppliers publicize capability to support corrosive gas handling under standard vacuum industry protocols, which is a prerequisite for suppliers targeting advanced etch, CVD, and coating processes.

Practical report contents — what executives will find in the full study

The full PW Consulting report is structured to be immediately actionable for strategy teams, M&A groups, product managers, and procurement. Highlights include:

- Market sizing and forecasting methodology (2020–2025 historicals; 2026–2032 forecast), including sensitivity scenarios and bottom-up validation.

- Segment-level demand drivers (by product type and application) with adoption timelines and inflection-point analysis. Note: granular regional and application share tables are intentionally omitted from this preview and are available in the full report.

- Competitive benchmarking and supplier scorecards (technology, service, channel coverage, margin profile, differentiation levers).

- Technology roadmap and R&D investment implications (materials science, temperature compensation algorithms, sensor electronics, and digital integration for predictive maintenance).

- Go-to-market playbooks for incumbents and challengers — product roadmaps, service monetization, direct vs. channel approaches, and OEM partnership templates.

- M&A screening framework and valuation sensitivity models tailored to the gauge market’s concentration and recurring-revenue dynamics.

- Procurement and operations playbooks — bill-of-material risk, supplier dual-sourcing checklists, and calibration & service network implications.

- Primary interview synthesis and commercial diligence appendices to support deal teams.

Strategic actions PW Consulting recommends for 2026

- Prioritize product differentiation tied to process economics: Invest in materials (ceramic, sapphire), temperature-compensation control, and gas-independent measurement accuracy that directly translate into yield improvements for semiconductor customers.

- Monetize installed base via services: Build calibrated service networks and subscription-based calibration to capture predictable aftermarket revenue and strengthen customer lock-in.

- Pursue targeted M&A and partnerships: Given the market’s concentration, bolt-on acquisitions that add niche capabilities (e.g., high-temp ceramic diaphragms or corrosive gas compatibility) often yield faster path-to-revenue than organic development.

- Harden supply chains: Map single-source risks for diaphragm materials and critical electronics; pursue dual-sourcing and near-shoring for key components ahead of projected capacity expansions in target regions.

- Embed digital monitoring: Add diagnostics, drift detection, and remote calibration features to new instrument families to increase differentiation and service attach rates.

How to use this primer in executive workflows

Boards, investment committees, and product strategy teams can use this brief as a rapid diagnostic. For 2026 planning cycles, we recommend three immediate steps:

- Rapid portfolio review: Map your product and service offerings against process imperatives in semiconductor and industrial vacuum applications; identify the top two features that justify price premiums.

- M&A screening sprint: Apply the report’s acquisition filters to generate a shortlist of targets that close capability gaps (materials, high-temp tolerance, regionally strategic service networks).

- Pilot & scale: Deploy two commercial pilots — one focused on a high-value fab integration, the other on a service subscription test — to validate revenue models and capture early learnings for 2027 scaling.

Closing — why obtaining the full report matters

This primer outlines why capacitance diaphragm vacuum gauges are a strategically significant but technically nuanced segment. The market’s steady growth profile, combined with clear concentration among leading suppliers and accelerating technology demands from semiconductor and advanced manufacturing processes, creates both defensive and offensive opportunities for market participants. However, the most consequential insights — detailed regional and application splits, supplier-level financial proxies, and transaction-term benchmarking — are intentionally withheld from this overview. For teams building investment cases, conducting commercial diligence, or defining product roadmaps for 2026 and beyond, the full PW Consulting report provides the proprietary tables, scenario models, and implementation playbooks required to move from strategy to execution.

Contact PW Consulting or visit our publications page to access the full Capacitance Diaphragm Vacuum Gauges Market report, licensing options, and bespoke advisory engagements designed to translate these insights into measurable actions in 2026.

For detailed analysis of this topic, please visit the official page:Capacitance Diaphragm Vacuum Gauges Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com