Cyber-Physical Systems Market: Strategic Imperatives for 2026 — PW Consulting Brief

Executive snapshot

The cyber-physical systems (CPS) market is entering a decisive growth phase that will shape capital allocation, architecture decisions, and M&A agendas for industrial and enterprise buyers in 2026. PW Consulting’s latest study uses 2025 as the base year and projects the market through 2032; our high-level modelling shows the market accelerating from a mid‑triple‑digit million dollar base in 2025 to a substantially larger ecosystem by 2032, driven by a sustained compound annual growth rate of 13.72% over the 2026–2032 forecast horizon. The trajectory since 2020 reflects rapid adoption across manufacturing, energy, aerospace, healthcare and adjacent sectors, and the next two to three years will determine which technology stacks and go‑to‑market motions dominate long term.

Cyber Physical System Market

Why this matters to executives in 2026

For senior leaders tasked with portfolio decisions in 2026, CPS is no longer an exploratory item — it is an operational and strategic imperative. The market expansion we model creates three concrete consequences for decision makers:

Cyber Physical System Market

- Scale and timing of investment: With market size roughly doubling since the early 2020s and continuing to expand materially through 2032 under a 13.72% CAGR, organizations must prioritize where to invest now to secure position in the value chain rather than chasing catch‑up later.

- Vendor and architectural lock‑in risk: As CPS solutions move from pilots to plant‑floor and grid‑scale deployments, early architecture choices — cloud provider, edge compute fabric, digital twin framework, and cybersecurity posture — will determine total cost of ownership and upgrade trajectories for years.

- Operational resilience and regulatory exposure: Adoption across critical infrastructure increases both systemic benefits and systemic risk. Standards and public funding programs are converging on CPS integration and assurance, making compliance and traceable assurance mechanisms a board‑level concern.

Market dynamics shaping 2026 decisions

Three interlocking forces define the near‑term CPS landscape:

Cyber Physical System Market

- Technology convergence: The maturation of edge AI silicon, deterministic networking, and high‑fidelity digital twins is collapsing latency and fidelity barriers that previously limited CPS use cases to large incumbents. This convergence is creating new product categories at the intersection of OT and IT.

- Security and visibility: As CPS endpoints proliferate, visibility across OT and IoT domains is becoming a prerequisite for safe scale. Recent market activity — including new funding rounds for specialist CPS security vendors and launches of OT asset discovery capabilities — underscores the premium buyers place on unified exposure management and continuous assurance.

- Standardization and public programs: National and international bodies are formalizing CPS frameworks and funding models that lower technical risk for adopters. Examples include updated guidance for cross‑domain interoperability and federal grant programs that prioritize tight integration between computational and physical systems. Leaders will embed these frameworks into procurement and integration blueprints to accelerate deployment and reduce compliance friction.

Strategic plays for 2026

Companies should consider three pragmatic moves to convert market momentum into sustained advantage:

- Adopt a modular “protectable” architecture: Design CPS estates as composable layers — deterministic edge compute, secure networking, a normalized data fabric, and platform‑agnostic digital twins — so upgrades and supplier changes can occur without wholesale rip‑and‑replace.

- Prioritize visibility and risk remediation: Invest in discovery and exposure management early. The acceleration of specialist players and feature launches in 2026 makes it possible to gain enterprise‑grade OT and IoT visibility within quarters, materially reducing breach windows and operational downtime risk.

- Construct ecosystem plays: Rather than competing in isolation, seek partnerships that combine domain OEMs, cloud platform capabilities and cybersecurity specialists. Strategic alliances accelerate time to value while distributing implementation risk across partners.

Competitive landscape — what to watch

The CPS vendor ecosystem combines legacy industrial incumbents, networking and cloud platform leaders, silicon and semiconductor suppliers, and a rapidly consolidating security layer. Market concentration is moderate: the three largest providers account for a meaningful but not dominant share of revenue, and the top five expand that share by only a few percentage points — a structure that favors both scale players and nimble specialists.

Key competitive archetypes and representative firms include:

- Industrial integrators and automation leaders — Companies with deep systems integration capabilities and plant‑level credibility continue to lead major brownfield modernization programs. Their strengths lie in domain expertise, industrial control systems, and turnkey delivery for manufacturing and process industries.

- Cloud and enterprise software platforms — Hyperscalers and platform vendors provide the scalable IoT backplane, cloud analytics and security services. Their strategic advantage is the breadth of platform services and go‑to‑market reach into enterprise IT.

- Networking, edge compute and silicon suppliers — These firms deliver the determinism and performance necessary for real‑time CPS use cases. Edge AI processors and validated hardware platforms are becoming a competitive choke point for latency‑sensitive applications.

- Security and visibility specialists — Focused vendors deliver OT/IoT discovery, exposure management and CPS‑specific threat detection. Their recent funding and product launches reflect rising investor and buyer appetite for specialized protection layers.

Representative companies profiled in the PW Consulting study include industrial stalwarts deploying digital twins and factory automation, networking and cloud leaders providing secure edge compute and platform services, silicon vendors enabling low‑latency inference at the edge, and specialist CPS security firms expanding exposure management capabilities. Each is evaluated in the report across technical depth, go‑to‑market reach, integration maturity, and ecosystem partnerships.

Notable recent movements

- New capital flows into CPS security platforms and expanded product footprints for OT visibility have accelerated vendor maturity, reducing the time‑to‑value for enterprise adopters.

- Platform vendors have launched integrated discovery and exposure management capabilities to reduce the friction consumers face when aligning IT and OT inventories.

- Standards and public funding are aligning with industry needs: updated federated CPS frameworks and targeted research program solicitations have increased the practical pathways for cross‑domain projects, particularly those combining manufacturing and transportation use cases.

What the PW Consulting CPS report contains (practical deliverables)

Our new market research balances executive clarity with operational depth. The full report includes:

- Top‑line market sizing and a granular forecast model covering 2026–2032 (13.72% CAGR), with scenario sensitivity and key demand drivers.

- A detailed competitive heatmap and vendor dossiers that assess technical capabilities, strategic intent, and integration readiness.

- Use‑case taxonomies and validated ROI templates for priority verticals, linked to deployment cadence and risk buffers to inform capex decisions.

- Architectural blueprints and procurement checklists that operational teams can use to scope pilots through scale‑up, with explicit guidance on interoperability and upgrade paths.

- Cybersecurity and assurance playbooks aligned to the latest CPS and IoT standards, and recommended guardrails for compliance and auditability.

- M&A and partner screening criteria, including playbooks for carve‑outs, integrations and strategic minority investments.

- Methodology annex with data sources, modelling assumptions, and sensitivity testing so buyers can inspect and adapt forecasts to their internal scenarios.

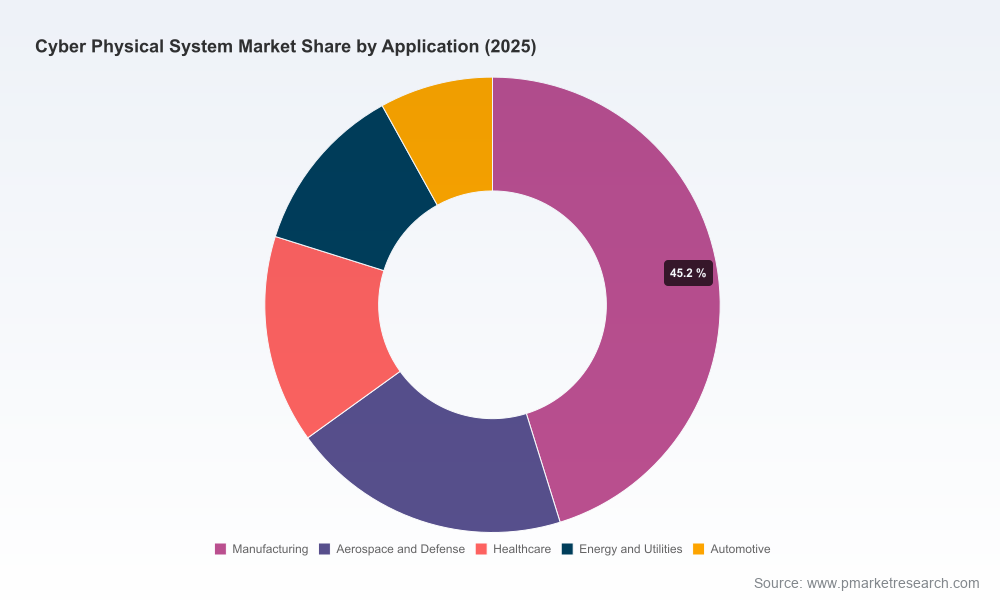

Note: This executive brief intentionally previews thematic conclusions and high‑level market sizing; the full report contains the granular regional and application split data, subsector revenue tables, and vendor scoring matrices that corporate development, strategy and procurement teams use to operationalize investments.

How to use this intelligence in 2026

Practical next steps for leadership teams:

- Run a seven‑week “value mapping” exercise that aligns executive priorities with CPS use cases and produces prioritized PoC charters tied to measurable KPIs.

- Mandate cross‑functional procurement pilots with pre‑defined interoperability checklists and security acceptance criteria to avoid downstream lock‑in.

- Allocate a portion of transformation budgets to visibility and exposure remediation first; our modelling shows this reduces expected downtime and security‑related loss in early scale phases.

- Adopt an ecosystem playbook: select one systems integrator, one platform provider, and one security specialist for each major deployment to compress vendor governance and accelerate delivery.

Closing perspective

The CPS market’s momentum is real and measurable. For executives making 2026 decisions, the central challenge is not whether to adopt CPS technologies but how to adopt them in ways that capture upside while containing risk. PW Consulting’s CPS market study provides the empirical roadmap — from market sizing and vendor strategy to implementation blueprints and risk mitigation — that leaders need to move from pilot activity to durable competitive advantage.

For access to the full intelligence set, including the detailed regional and application breakdowns, full vendor profiles, and downloadable modelling spreadsheets, refer to the PW Consulting report landing page.

For detailed analysis of this topic, please visit the official page:Cyber Physical System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com