Dental Clinic in Dubai for Cosmetic Smile Makeover

Health |

2026-06-18 06:46:25

As PW Consulting’s lead industry analyst, I present a concise strategic preview of our new Biological Indicators Market study. Between 2020 and 2025 the market demonstrated steady expansion, growing from USD 583.5 Million to USD 704.0 Million (base year 2025). Our forecasted trajectory sees continued momentum into the next decade, with the market projected to exceed USD 1.13 Billion by 2032, driven by a compound annual growth rate (CAGR) of 7.2% across the 2026–2032 forecast window. For executives planning 2026 budgets, product roadmaps, or M&A activity, this market profile highlights where value is consolidating and where operational friction will shape winners and laggards.

Biological Indicators Market

Acceleration from validation automation: Rapid-readout biological indicators and integrated incubator-readers are transitioning from nice-to-have innovations to standard elements of sterile-processing suites. The combination of regulatory pressure and labor optimization is compressing validation cycles and changing procurement priorities.

Biological Indicators Market

Regulatory inflection points: Recent and pending 510(k) activity, along with refreshed ISO compliance expectations, is raising the technical bar for suppliers and creating short windows for regulatory-first movers to capture share.

Biological Indicators Market

Service-layer disruption: Outsourced spore-testing workflows and third-party incubation services are under stress from rising labor costs and supplier exits, forcing facilities to re-evaluate in-house vs. outsourced validation economics.

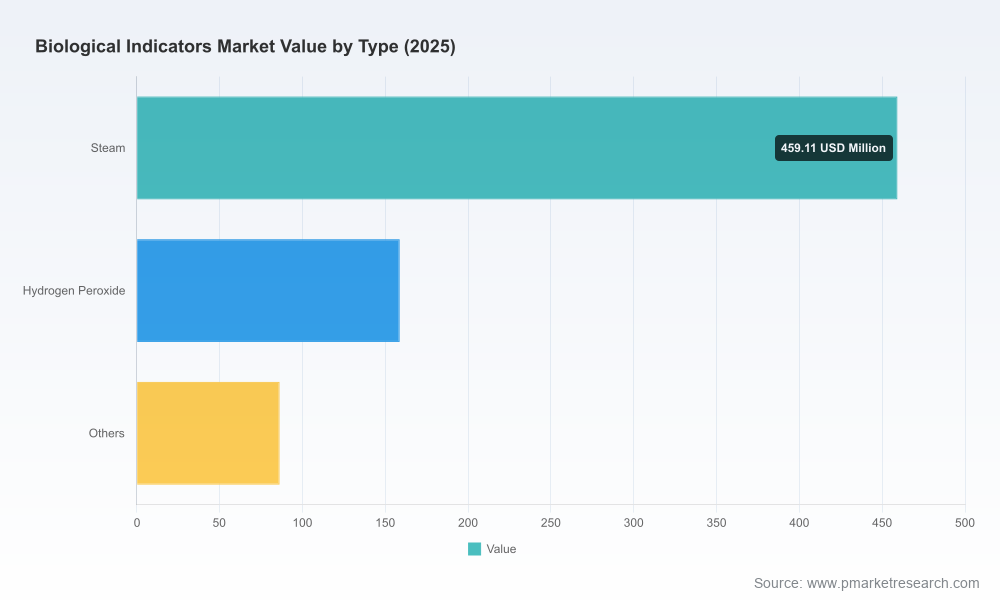

Historical momentum shows consistent expansion in demand for biological indicators, interrupted briefly by cyclical dips tied to procurement and supply-chain timing in 2024, then recovering into 2025. Our base-year analysis recognizes USD 704.0 Million in 2025 as the inflection point for a higher-growth phase: under our central forecast the market advances at a 7.2% CAGR (2026–2032) to surpass USD 1,138.3 Million by 2032. This growth is not uniform — it is concentrated among new rapid-readout formats, validated challenge packs for low-temperature sterilization, and integrated monitoring solutions — but this article intentionally omits granular subsegment numbers to preserve the tactical value of the full report.

Strategic frameworks: Decision trees for procurement, validation automation, and capital investments that translate market signals into year-1 and year-3 actions.

Commercial playbooks: Pricing pressure scenarios, package/consumable bundling strategies, and channel optimization paths for manufacturers and distributors.

Regulatory tracker: A rolling matrix of ISO and FDA touchpoints (including recent 510(k) filings and clearances), with timeline estimates and documentation checklists for accelerated submissions.

Operational models: Labor and cost sensitivity analyses that quantify the break-even points for in-house incubation versus outsourcing, factoring recent service exits and wage inflation.

Technology roadmaps: Comparative assessment of rapid-readout chemistries and auto-reader integration options, including validation burdens and time-to-deployment estimates.

M&A and partnership diagnostics: Heatmaps identifying attractive targets by capability, regulatory status, and geographic reach, plus integration risk checklists.

Buyer’s checklist: A pragmatic procurement scorecard for healthcare facilities and pharmaceutical manufacturers—covering compliance, total cost of ownership, and operational resilience.

The market remains moderately diversified with a mix of global platform players, specialized suppliers, and regional manufacturers. The competitive dynamic is bifurcating along two axes: (1) providers that bundle biological indicators with integrated rapid-readout systems and validation services, and (2) specialized consumables suppliers focused on cost-efficient challenge packs and niche chemistries.

3M Company — A strategic incumbent that combines broad product coverage with regulatory muscle. Recent FDA clearances underline 3M’s playbook of pairing new indicator chemistries with cleared rapid-readout formats for hospital and pharma validation workflows.

STERIS plc — A technology-integrator focusing on rapid-readout incubation and readout automation. Product introductions in 2025 signal an aggressive push to reduce time-to-result and embed recurring revenue through incubator consumables.

Solventum Corporation — Specialist supplier leveraging “super rapid” indicator chemistries and packaged challenge-packs that address low-temperature sterilization challenges; recent launches suggest a move to capture pharma and device customers seeking combined biological+chemical indicator solutions.

Mesa Laboratories, Propper, Tuttnauer, Getinge, Terragene and Andersen — A mix of globally-recognized device makers and regional specialists that compete on service breadth (mail-in testing, integration with autoclaves), regulatory compliance, and price-performance in established institutional accounts.

Taken together, the most important commercial inference for 2026 is this: product differentiation will be defined less by basic spore formats and more by system-level integration, speed-to-read, and validated workflow services that lower the customer’s labor and compliance burden.

Product launches and FDA momentum: New rapid 20-minute readout biological indicators and cleared super-rapid steam products have moved from R&D pipelines into commercial release in 2024–2025. These create urgency for facilities to plan upgrade paths to avoid being audited against newer validation standards.

Service-provider exits: Notable discontinuations of third-party spore-testing services are elevating the operational risk for networks that relied on external incubation. Facilities must model contingency plans and potential capital outlay for in-house capabilities.

Standards and submissions: Renewed attention to ISO 11138-series compliance and several high-profile 510(k) submissions for integrated incubators underscore the regulatory premium on validated, automated solutions.

Reimbursement and compliance linkages: Sterilization validation is increasingly treated as an auditable element in infection prevention reimbursement frameworks, making non-compliance a downstream revenue and reputational risk.

Manufacturers and OEMs: Prioritize modular rapid-readout platforms that can be certified for multiple sterilant chemistries. Invest in regulatory dossiers early — being first-to-market with a cleared system delivers outsized adoption in large hospital networks.

Distributors and service providers: Re-evaluate service mix toward hybrid offerings (equipment + managed validation services). Where third-party incubation capacity is declining, create “white-label” or co-branded solutions to capture displaced demand.

Hospital sterile processing and pharma QC teams: Conduct a resilience assessment of current validation workflows; run a short-term scenario comparing outsourced testing vs. capex for on-site automation to hedge against service discontinuities and labor constraints.

Private equity and strategic buyers: Target firms that combine rapid-readout consumables with software-enabled subscription economics — these assets offer defensible recurring revenue and easier integration into large account contracts.

Regulatory and quality leaders: Re-prioritize documentation and sample archiving to align with updated ISO expectations and expect auditors to reference recent FDA clearances when assessing validation protocols.

Week 1–2: Run an executive briefing using our procurement scorecard to identify top 3 short-term exposure points (supply, labor, compliance).

Week 3–6: Validate vendor roadmaps against the regulatory tracker and prioritize one pilot for rapid-readout integration with defined KPIs (time-to-result, cost per validated cycle).

Week 7–12: Build or update a three-year sourcing strategy that explicitly models the impact of reduced third-party incubation capacity and includes a go/no-go capex threshold.

The full report includes granular segmentation by sterilant type, application, and region, proprietary models quantifying labor and outsourcing impact, competitive company scorecards with capability matrices, and a prioritized list of playbook items tailored to buyer type. In keeping with the “preview” intent of this article, we have not disclosed subsegment financial splits or detailed regional allocations here; these data points and the underlying Excel models are provided exclusively in the downloadable report to preserve actionable advantage for subscribers and clients.

Biological indicators are evolving from consumable testing products into system-enabled compliance tools. For leaders making 2026 decisions, the core strategic question is whether to compete on marginal product innovation or to re-architect offerings around validated workflow services that reduce customers’ labor and audit exposure. PW Consulting’s Biological Indicators Market study gives you the data, regulatory timelines, and commercial playbooks to choose — and to act — with conviction.

For detailed analysis of this topic, please visit the official page:Biological Indicators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com