HostBooks Limited Case: AI-Powered Finance Solutions for Growing Enterprises

Technology |

2026-07-08 21:55:49

As PW Consulting’s senior strategic advisor and industry lead, I present a focused preview of our latest Tire Cord and Tire Fabrics Market study — an evidence-based roadmap designed to inform high-stakes commercial and capital decisions in 2026. Built on a 2025 base year and projecting through 2032, the study synthesizes historical trends (2020–2025), supplier dynamics, regulatory inflection points and technology adoption curves to deliver actionable guidance. At the market level, the segment has expanded from the mid‑2020s and is projected to grow at a compound annual growth rate of 6.5% across the 2026–2032 forecast window, continuing a recovery and re‑rating that began during the pandemic recovery phase.

Tire Cord and Tire Fabrics Market

Two features make this research essential for 2026 decision cycles. First, the market’s macro trajectory is clear: steady, above‑GDP growth fueled by structural mobility trends and material substitution pressures. Second, the industry sits at a convergence of supply‑side realignment (input price volatility, regional protectionism) and demand‑side disruption (regulatory limits on tire wear, OEM sustainability mandates). The combination elevates strategic questions that cannot be answered with point estimates alone: Do you accelerate investments in recycled and bio‑based feedstocks? Where do you place capacity for low‑emission vehicle tires? How do you protect margins as raw material and regulatory costs migrate?

Tire Cord and Tire Fabrics Market

Growth profile: After a measurable recovery in the early 2020s, the global tire cord and fabric market reached an inflection in 2025 and enters 2026 with renewed momentum. Our top‑line projection shows the industry continuing to expand through the forecast period, reaching materially higher revenue by 2032 under a central scenario consistent with a 6.5% CAGR. For leaders this means a multi‑year runway for capacity and product innovation investments — provided those investments are targeted and adaptive to regulatory and feedstock shifts.

Tire Cord and Tire Fabrics Market

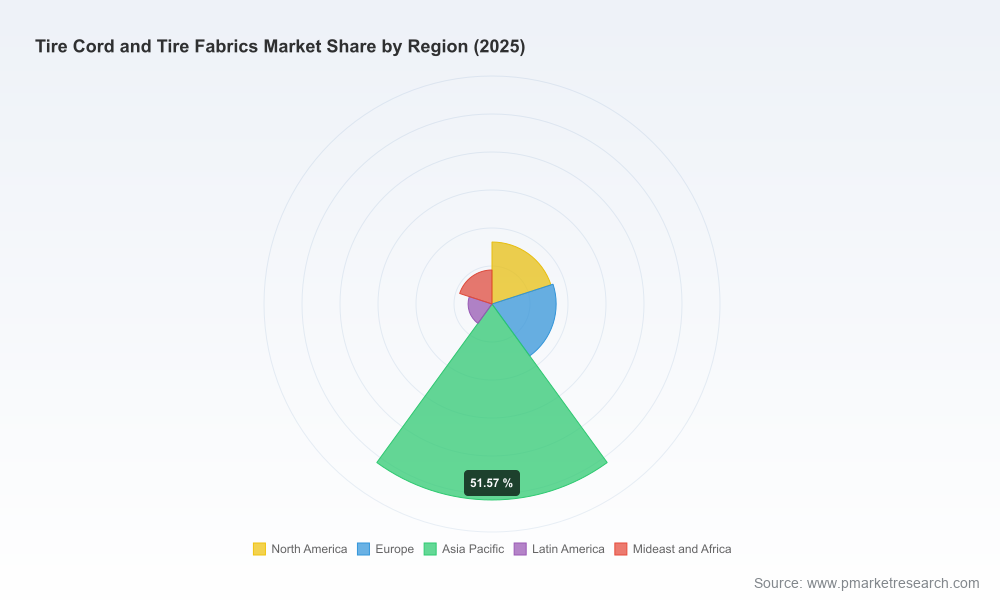

Consolidation and competitive intensity: Industry concentration is meaningful — the largest groups collectively command a majority of global capacity, and the top five firms hold a commanding share of market presence. That concentration creates both barriers and opportunities: scale advantages in raw material procurement and customer contracts, but also active opportunities for regional challengers to differentiate on specialty products, service, or sustainability credentials.

Material and process inflection points: Two supply‑side dynamics are especially consequential. First, polymer feedstock pricing movements — notably downward pressure on Nylon 6 in Asia during the latter half of 2025 — temporarily relieve input cost pressure but can trigger strategic repositioning among producers (inventory strategy, price discipline, and contract renegotiations). Second, regulatory drivers are forcing near‑term process reengineering: formaldehyde restrictions scheduled to take effect in the EU and U.S. in 2027 require reworking adhesive/dipping formulations and qualifying alternative chemistries before mandated timelines.

Regulatory shockwaves and product design: The advent of Euro 7 and related measures matters beyond emissions reporting — Euro 7’s introduction of particle emission thresholds for tire wear creates a direct design-to‑cost imperative for tire fabric suppliers. OEMs will increasingly demand low‑abrasion yarns and fabric constructions that demonstrably reduce particulate release. Suppliers pre‑positioning with validated low‑wear solutions will secure stronger OEM partnerships and premium pricing.

Trade and input security: Recent determinations by the U.S. International Trade Commission to maintain antidumping and countervailing duties on certain steel and alloy imports highlight that import protection remains an active lever. For tire cord and fabric makers — who depend on a mix of synthetic polymers, specialty fibers, and reinforcing wires — trade measures and tariff uncertainty should be explicitly modeled into sourcing and capex options.

The supplier ecosystem is diverse and strategically differentiated. Major incumbents combine scale manufacturing with active product portfolios spanning nylon, polyester, rayon, aramid and specialty treated fabrics. Recent competitive moves underscore two themes: sustainability as a purchasing criterion, and deepening technological specialization.

Technology and materials leadership: Several established players are accelerating R&D and piloting next‑generation fibers (including high‑performance aramids and engineered polyesters) to meet OEM demands for durability and reduced mass. Firms with longstanding polymer science platforms and in‑house dipping/adhesive expertise hold a time‑to‑market advantage in qualifying formaldehyde‑free processes.

Sustainability as differentiation: The public launches of recycled and bio‑based PET solutions earlier in the 2025–2026 window — including a notable demonstration by a major petrochemical supplier in early 2026 — signal that circularity credentials are transitioning from marketing points to procurement requirements. Automotive OEMs and tier‑1s are beginning to incorporate recycled content thresholds into supplier selection, suggesting first‑mover benefits for suppliers with validated mass‑balance and tracing systems.

Regional specialization: Manufacturers based in Asia and select European hubs continue to compete on cost and scale. At the same time, niche producers in Europe and North America are focused on high‑value specialty segments (e.g., aramid‑reinforced fabrics, rayon cord for classic tire applications) where margin resilience is higher. For prospective investors and partners, the interplay of local regulation, logistics, and customer proximity should drive geographic strategy.

Representative players profiled in the study include large integrated fiber and textile producers, specialty cord makers, and industrial textile firms with global footprints. Each profile evaluates R&D capabilities, product pipeline, recent investments, capacity positioning, and go‑to‑market motion — enabling comparative assessment without revealing proprietary market shares in this preview.

Product innovation: Early 2026 saw a public showcase of bio‑based and recycled PET solutions targeted at tire fabric applications — a concrete signal that polymer producers are scaling alternatives to virgin feedstocks in response to both OEM demand and regulatory pressure on tire particulate emissions.

OEM commitment to recycled content: Late 2025 activity from a major global tire OEM expanded commercial use cases for recycled PET‑based reinforcements, validating supply chain pilots and creating referenced case studies buyers can adopt.

Raw material pricing trends: In Asia, Nylon 6 prices moved downward through the second half of 2025, creating transient margin relief and prompting opportunistic inventory actions by large buyers.

Regulatory timelines: Formaldehyde restrictions in key markets and Euro 7’s tire wear thresholds create hard deadlines that affect process, product testing and supplier qualification pipelines.

Trade rulings: Determinations by trade authorities in 2025–2026 have sustained certain duties that continue to shape cost and sourcing strategies for reinforcing wires and related inputs.

The full PW Consulting report is structured to drive immediate use in boardroom scenarios, procurement negotiations and R&D roadmaps. Key deliverables include:

Top‑down market sizing and scenario forecasts (base year 2025; 2026–2032), with sensitivity runs that reflect oil‑price, trade and regulatory shock scenarios.

Supply‑chain maps and margin waterfall models that quantify where value accrues across fiber producers, fabric weavers, dippers, and tier‑1 integrators.

Regulatory impact assessments translating Euro 7 and formaldehyde constraints into product cost and testing timelines, with recommended mitigation pathways for suppliers and OEMs.

Competitive intelligence packages: comparative capability matrices for each major supplier, recent strategic moves, and a watch‑list of likely M&A targets and acquirers.

Commercial playbooks: supplier scoring templates, raw material hedging strategies, and commercial negotiation checklists tailored for both OEMs and materials suppliers.

CapEx and location decision framework that aligns capacity additions with projected demand pockets and regulatory exposure, including a time‑phased investment prioritization matrix.

Prioritize adhesive reformulation and qualification programs: With formaldehyde restrictions and Euro 7 timelines, R&D teams should run parallel qualification tracks for alternative dipping chemistries and secure pilot lines with strategic OEM partners.

Lock down upstream supply options: Even where polymer costs have eased, implement multi‑year frameworks and optionality for recycled feedstocks to secure predictable margins and support sustainability targets.

Segment go‑to‑market by value: Reserve investment for high‑value specialty segments (e.g., aramid and engineered polyester offerings) while automating and optimizing cost positions for commodity cord supply.

Embed regulatory scenario planning into product roadmaps: Map Euro 7 compliance timelines against product certification cycles to avoid last‑minute costly reworks.

Monitor consolidation opportunities: Given industry concentration dynamics, develop M&A playbooks for bolt‑on acquisitions that close capability gaps (e.g., dipping chemistry, recycled feedstock traceability, localized finishing capacity).

This preview highlights the decision levers that will determine winners in the tire cord and fabric market over the next planning cycle. The full report contains the granular segmentation, supplier benchmark tables, and country‑level demand breakdowns that corporate strategy, procurement, and R&D teams need to operationalize these recommendations. If your 2026 planning requires scenario modeling, supplier diligence, or a tailored market entry blueprint, PW Consulting can provide rapid‑turn custom analyses and facilitation workshops to convert the report’s insights into executable programs.

Reach out to our market team to schedule a briefing and access the full dataset and appendices. The detailed segmentation and confidential company matrices are reserved for report subscribers and bespoke client engagements — precisely the elements that turn a high‑level view into a 2026 winning strategy.

For detailed analysis of this topic, please visit the official page:Tire Cord and Tire Fabrics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com