Healthcare Generative AI Market: Insights, Key Players, and Growth Analysis

Other |

2026-05-27 11:43:43

PW Consulting’s latest market study on Cancer Treatment Drugs furnishes senior executives and strategy teams with a compact, decision-focused preview of the forces that will shape portfolio outcomes and commercial returns in 2026 and beyond. The global market has experienced sustained expansion through 2020–2025 and—based on our baseline projections—enters an accelerated growth phase across the 2026–2032 forecast window. Our analysis synthesizes macro growth, regulatory shifts, competitive positioning, and near-term clinical and commercial catalysts to enable practical choices on R&D prioritization, M&A, market access, and manufacturing resilience.

Cancer Treatment Drugs Market

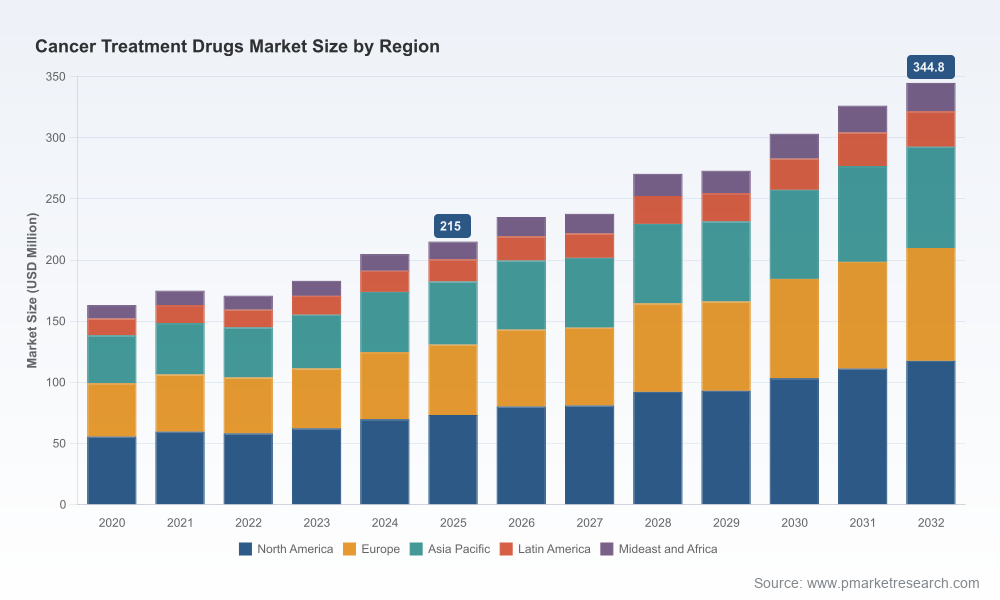

Anchored on a 2025 base year, the market for cancer treatment drugs has moved from a mid-hundreds million-dollar base in 2020 to a larger industry scale by 2025, and is projected to expand significantly through 2032. Our forecast for 2026–2032 assumes a compound annual growth rate (CAGR) consistent with an environment of continued innovation, rising uptake of targeted and immunotherapies, and selective pricing pressures. Specifically, the market’s momentum across the forecast period reflects the combined effect of new molecular entities, label expansions for established biologics and small molecules, and growing clinical adoption of biomarker-driven regimens.

Cancer Treatment Drugs Market

Regulatory and reimbursement actions that took effect or were announced through late 2025 and early 2026 materially affect commercial strategy. Government negotiation mechanisms targeting high-expenditure medicines, adjustments to physician-administered drug reimbursement methodologies, and selective introduction of maximum fair prices for a subset of therapies introduce new pricing volatility. At the same time, the FDA’s continued throughput of novel oncology approvals preserves clinical upside for companies that can rapidly translate efficacy signals into payer-acceptable value propositions.

Cancer Treatment Drugs Market

For 2026 corporate planning, this confluence of forces means companies must simultaneously model lower net price scenarios for certain legacy agents while investing in evidence-generation (real-world evidence, long-term outcomes) that supports premium pricing and quicker formulary uptake for innovations.

Recent shortages of key chemotherapeutic agents have underscored the systemic risk to treatment continuity. These events have prompted institutional buyers and payers to demand stronger supply assurances and contingency plans. For manufacturers, this elevates the importance of diversified sourcing, onshore or regional manufacturing capacity, and contractual commitments that balance commercial flexibility with supply guarantees.

The cancer drugs competitive environment is anchored by established multinational pharmaceutical companies with deep oncology portfolios, biologics expertise, and global commercial infrastructure. These incumbents simultaneously defend high-value franchises and pursue label expansions and combination strategies. At the same time, specialized biotechs and mid-sized oncology players are advancing niche, biomarker-defined candidates and sometimes achieving rapid commercial traction after focused approvals.

These incumbents continue to command strategic influence over market norms—pricing benchmarks, clinical trial standards, and payer negotiation practices. Nonetheless, the emergence of targeted approvals for rare genomic subsets creates windows for smaller players to capture high-margin niches and to become attractive merger targets.

For leadership teams entering the 2026 planning cycle, the blended picture of innovation-driven demand and policy-driven pricing pressure implies several prioritized actions:

Our full research package is designed as an operational toolkit for 2026 strategic planning and includes:

These deliverables are accompanied by an executive dashboard and customizable slide assets to accelerate board and investor communications.

This article is intentionally structured as a strategic trailer: it demonstrates the depth of our analysis and highlights the critical decisions facing industry leaders in 2026, while withholding detailed subsegment tables and specific regional/application splits that form the proprietary core of the full report. Those granulated forecasts and segmentation models are central to tactical decisions—launch sequencing, targeted licensing, and regional commercial investments—and are available in the complete report package.

The cancer treatment drugs market in 2026 presents a paradox: accelerating therapeutic opportunity against a backdrop of tightening price and access dynamics. Companies that move early to align clinical evidence generation with payer needs, secure supply resilience, and prioritize high-value, biomarker-led assets will be best positioned to convert scientific innovation into sustainable commercial performance. PW Consulting’s full report converts these strategic priorities into executable actions—including quantified scenarios and playbooks—to support confident decisions in 2026. For access to the full dataset, segment-level forecasts, and the decision-support toolkit, visit our report page or contact your PW Consulting representative.

For detailed analysis of this topic, please visit the official page:Cancer Treatment Drugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com