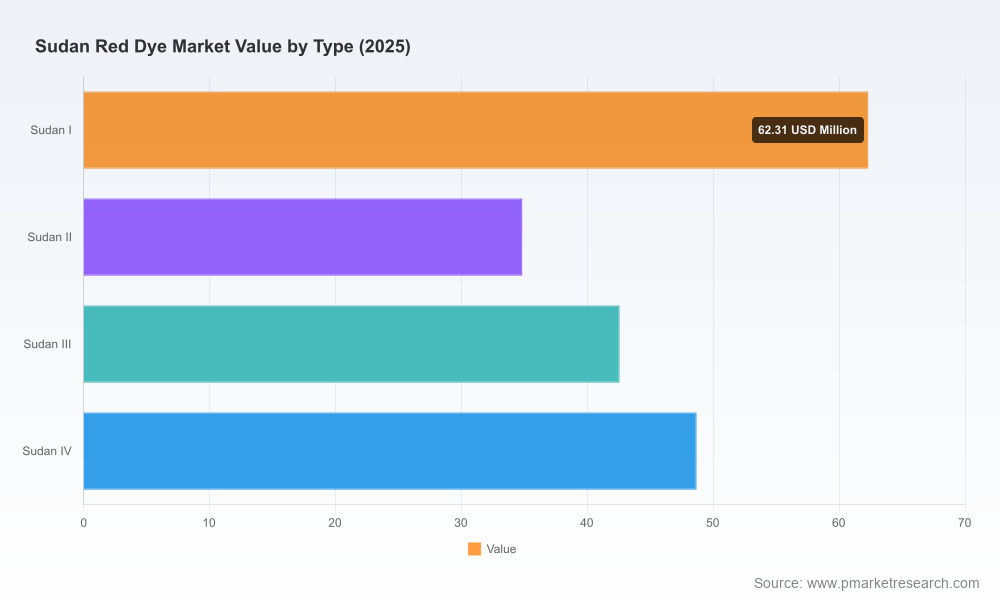

PW Consulting Forecasts Sudan Red Dye Market to Expand from USD 188.4 Million in 2025 to USD 250.44 Million by 2032 at a 4.15% CAGR

Other |

2026-07-07 06:30:53

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused briefing to orient executive decisions in 2026 around the Deep Brain Stimulation (DBS) devices market. This short-form insight synthesizes the market trajectory, competitive dynamics, regulatory and reimbursement inflection points, and the practical, decision-grade outputs contained in our full Deep Brain Stimulation Devices Market report. It is intentionally diagnostic and directional — designed to demonstrate our analytic depth while preserving the granular segment intelligence that is reserved for our full report.

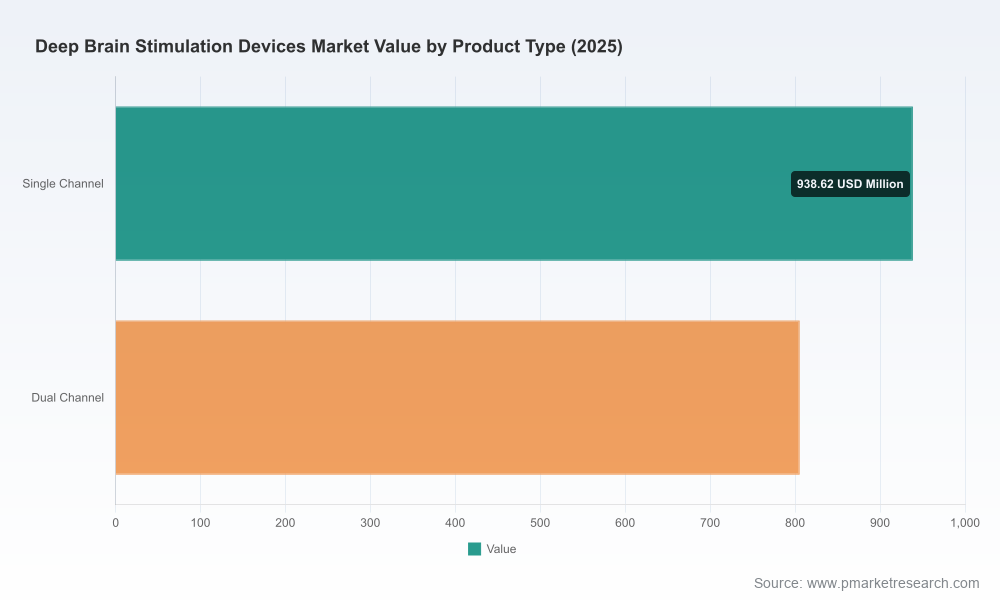

Deep Brain Stimulation Devices Market

The DBS market has moved from niche clinical adoption to a phase of scalable, technology-led expansion. By the base year 2025 the market reached approximately USD 1,744 million, following a sustained compound expansion through the historical period. Our forecast, anchored on a 10.4% compound annual growth rate (CAGR) for the 2026–2032 window, projects a near doubling of market value by the end of the forecast horizon. That quantitative momentum is underpinned by converging drivers — clinical evidence expansion, adaptive and closed-loop device approvals, growing capacity in emerging supplier geographies, and evolving payer frameworks.

Deep Brain Stimulation Devices Market

Investment timing: The market’s mid-decade inflection creates a narrow window in which late-stage R&D or capacity investments can convert into meaningful market share gains before consolidation dynamics intensify.

Deep Brain Stimulation Devices Market

Portfolio prioritization: Companies must decide whether to double down on hardware differentiation (lead design, directional contacts, battery tech) or on software-enabled differentiation (closed-loop algorithms, sensing and analytics, remote programming ecosystems).

M&A and partnership strategy: With a moderately concentrated market structure and a handful of incumbents controlling the majority of revenues, targeted acquisitions or alliances — especially for sensing, AI-driven programming, and regional go-to-market access — are among the fastest routes to scale.

Reimbursement and regulatory playbooks: Regulatory approvals for adaptive/closed-loop therapy and clarity in national reimbursement coding are key gating items that can accelerate adoption curves or, conversely, create localized barriers to uptake.

Technology evolution: The February 2025 U.S. FDA approval of the first Adaptive DBS system marked a watershed moment — validating closed-loop approaches and setting a new clinical expectation for real-time sensing and stimulation. This change shifts competitive bets from incremental lead or battery improvements toward systems integration and data-driven therapy optimization.

Payer signaling: National and national-adjacent reimbursement guidance issued through 2026 — including Medicare documentation and manufacturer-specific reimbursement guides — introduces both opportunity and complexity. Payers’ willingness to recognize differential value for adaptive systems and remote-programming capabilities will materially affect commercial uptake rates across markets.

Supply and quality dynamics: Product-level recalls and sterilization pathways illustrate that manufacturing and sterilization controls remain strategic imperatives. Device recalls — including notable Class 2 actions in the past 18 months — have immediate effects on surgical throughput and hospital contracting behavior, and they increase the value of robust post-market surveillance and supplier diversification.

Clinical adoption and referral networks: DBS adoption is not solely a function of device performance; it is equally dependent on multidisciplinary center experience, neurosurgical capacity, and referral pathways from movement disorder clinics. Investments that lower the operational burden of DBS (remote programming, simplified perioperative workflows) correlate with faster center-level adoption.

The market architecture combines legacy medtech leaders with nimble regional innovators. At a high level, the market demonstrates moderate concentration: the top three global vendors command a majority share of revenues, and the top five increase that concentration further. This structure creates a two-track competitive environment — one focused on sustaining clinical leadership via continuous product development, the other on cost and access plays in price-sensitive geographies.

Medtronic plc — A global leader with a recently FDA-approved adaptive DBS system and broad clinical footprint. Its strategic advantage lies in integrated sensing capability and a wide installed base that accelerates clinical validation and post-market data collection.

Abbott Laboratories — Competes with compact, rechargeable IPGs and remote programming features that appeal to movement-disorder centers focused on patient convenience and procedural efficiency.

Boston Scientific Corporation — Emphasizes directional lead design and programming flexibility to optimize therapy for complex presentation sets; surgical manuals and quality controls remain commercial centerpieces.

LivaNova PLC — Pursues collaboration-led development strategies in targeted neurological indications and is an active player in clinical partnerships and regional market development.

Chinese and Swiss innovators — A cohort of suppliers from China and Switzerland concentrate on electrode design and cost-effective systems tailored for regional markets and international expansion. Their technological specialization (e.g., electrode morphology, lead implantation accuracy) is shifting competitive pricing and choice dynamics in several markets.

Recent developments — including regulatory approvals, industry recognitions, reimbursement guides, and product recalls — are not peripheral; they materially shape near-term commercial prospectuses. For example, the 2025 FDA clearance for adaptive DBS systems and subsequent industry accolades validate the clinical and commercial pathway for closed-loop solutions, but they also raise the standard for competitive product roadmaps. Separately, recall events highlight the reputational and operational fragility of high-complexity implantable device supply chains.

PW Consulting’s Deep Brain Stimulation Devices Market report goes beyond descriptive narratives. It is structured to support executable decisions with the following operational modules:

Market modelling: A transparent demand model capturing historical adoption dynamics (2020–2025) and scenarios through 2032, with sensitivity levers for clinical adoption rates, reimbursement uptake, and pricing evolution.

Commercial playbooks: Go-to-market templates for global and regional launches, including center segmentation, contracting approaches, and surgical pathway optimization to accelerate adoption.

Technology roadmaps: Comparative assessment of sensing, lead, and IPG technologies; R&D prioritization matrices that map incremental revenue potential to technical risk and time-to-market.

Regulatory & reimbursement tracker: Actionable timelines and coding guidance for major payer systems, plus scenario plans for varying reimbursement outcomes.

Competitive intelligence: Strategic SWOT-style profiles of leading vendors, supplier mapping, and M&A target lists with valuation heuristics grounded in market concentration and growth trajectories.

Implementation tools: Financial models, commercial KPIs, and a decision playbook with prioritized initiatives for near-term (12–18 months) and medium-term (3–5 years) horizons.

Importantly, the report preserves detailed split analyses by region, product type, and clinical application in downloadable annexes. These granular tables — intentionally excluded from this briefing — are essential when calibrating pricing, salesforce deployment, or M&A valuations. If your objective is to refine territory-level budgets, identify the most attractive clinical cohorts, or stress-test an acquisition target, those annexes provide the necessary underlying numbers and model inputs.

Re-assess R&D prioritization through a closed-loop lens: Prioritize software/sensing integration over incremental hardware-only enhancements unless the latter directly reduce total cost-of-ownership for high-volume centers.

Design reimbursement-first pilots: Collaborate with payers and leading centers on value dossiers and real-world evidence collection to accelerate positive coverage decisions for adaptive systems and remote programming services.

Mitigate supply and quality risk: Implement supplier redundancy for critical components, upgrade sterilization validation in partnership with contract manufacturers, and embed recall contingency playbooks into commercial contracts.

Pursue focused inorganic plays: Target tuck-in acquisitions for sensing algorithms, cloud-based programming platforms, or regional distributors that substantially shorten market entry time in prioritized geographies.

The DBS market in 2026 is a classic strategic inflection: technological validation and payer clarity are aligning at the same moment that incumbents and challengers are optimizing commercial approaches. For executives, the immediate challenge is not just to invest — it is to invest in the right combinations of capability (sensing and software), market access (reimbursement and centers), and supply resilience. PW Consulting’s full report translates these high-level imperatives into executable plans — with the granular segment models, scenario analyses, and tools required to operationalize a winning strategy.

To access the full dataset, including regional, product, and application-level splits and our downloadable financial models, visit the report landing page. The annexes contain the detailed market tables you will need to finalize 2026 budgets, M&A valuations, and launch roadmaps.

For detailed analysis of this topic, please visit the official page:Deep Brain Stimulation Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com