PW Consulting: Synthetic Diamond Grit Market to Reach USD 3,065.05 Million by 2032 at a 5.2% CAGR — Asia Pacific Leads with USD 1,100.25 Million as Top‑5 Firms Hold 52.4%

Other |

2026-07-02 17:23:54

As PW Consulting’s Senior Strategy Consultant and Chief Industry Analyst, I present a forward-looking, executive-grade preview of our latest Ethernet Controller Market research. This briefing synthesizes the dataset and actionable interpretations that senior leaders will need to shape product roadmaps, procurement and M&A decisions, and cross-functional investment plans in 2026. The study is grounded in robust historical tracking (2020–2025), uses 2025 as the base year, and projects the market through a 2026–2032 forecast horizon.

Ethernet Controller Market

Timing: 2026 is a pivot year. Organizations are balancing near-term deployments (edge, factory automation, and data center refreshes) with multiyear investments in next-generation in-vehicle and hyperscale networking. Our preview highlights where to accelerate and where to defer capital allocation.

Ethernet Controller Market

Signal clarity: The Ethernet controller landscape is being reshaped by both optical and single-pair copper advances, deterministic low-latency requirements, and a tightening regulatory fabric around automotive functional safety and network security. Leaders need a synthesis between technological capability and commercial viability — which this research delivers.

Ethernet Controller Market

Risk calibration: The market exhibits moderate-to-high concentration among a handful of strategic suppliers (CR3 ~55%, CR5 ~65%), creating supplier-dependency risks as well as consolidation opportunities. Procurement, strategic sourcing, and alliance managers should use these concentration metrics as a starting point for scenario planning.

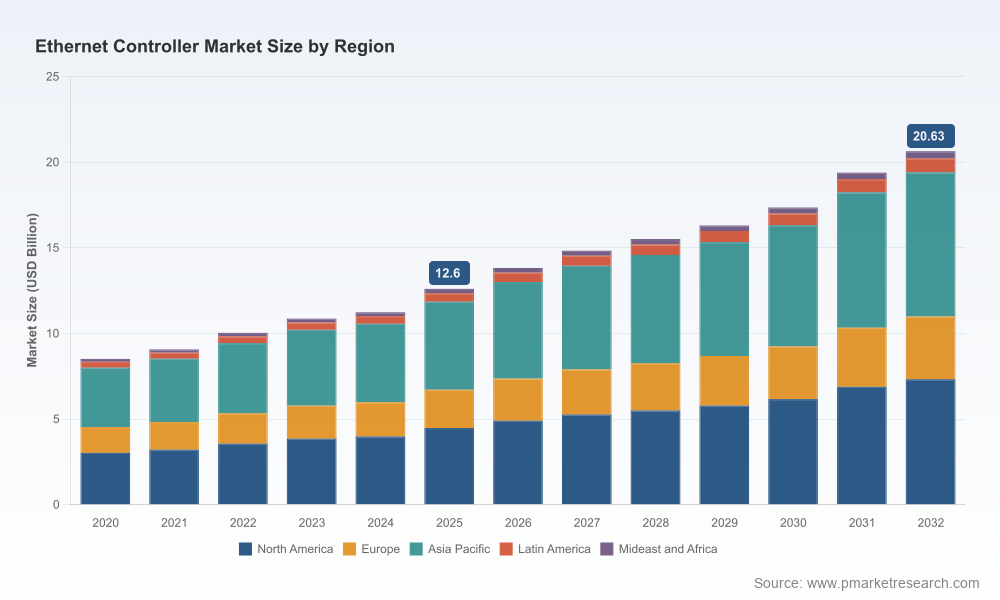

Our market sizing tracks an established growth path. The Ethernet controller market expanded from approximately USD 8.5 billion in 2020 to about USD 12.6 billion in 2025. Looking ahead, our base-case forecast anticipates a continuation of healthy expansion, with the market moving into the mid-teens in the late 2020s and reaching just over USD 20 billion by 2032. The compound annual growth rate across the forecast window is 7.3% — a rate that reflects steady, technology-driven adoption across data centers, industrial automation, automotive networks, and edge consumer/enterprise applications.

Interpreting those totals for strategy: a 7.3% CAGR over 2026–2032 implies expanding absolute opportunity even as pockets of the market experience bifurcation — high-volume, low-margin connectors for embedded devices coexist with high-value, feature-rich controllers targeted at hyperscale and safety-critical in-vehicle networks. This dynamic demands differentiated GTM and engineering plays rather than one-size-fits-all approaches.

Automotive safety and qualification: Functional safety certifications (e.g., ASIL B) and automotive qualification standards (AEC-Q100) are not optional for in-vehicle Ethernet PHYs when they connect to safety-critical systems. Product roadmaps must be aligned to these timelines to capture the vehicle OEM design-wins that begin to scale mid-decade.

Single-pair Ethernet (SPE): SPE is enabling lower-cost, sensor-level connectivity in smart factories and software-defined vehicles. Its economics and form-factor advantages are accelerating adoption at the edge, converting previously proprietary fieldbus deployments to Ethernet-based fabrics.

Time and security protocols: IEEE 1588 Precision Time Protocol and MACsec encryption are becoming baseline expectations for next-generation optical PHYs and long-reach links in enterprise and telco networks. Compliance and feature parity will be selection criteria for hyperscale and service-provider customers.

Co-packaged optics and higher lane rates: Integration of 200G/lane SerDes and co-packaged optics is unlocking 1.6T transceiver applications inside data centers, with implications for power budgets, thermal design, and switch architecture. These advances favor suppliers with systems-level roadmaps across silicon, optics, and reference platform partnerships.

Deterministic low-latency: Industrial and smart-manufacturing requirements now mandate deterministic behavior for Ethernet PHYs, placing a premium on silicon with both low jitter and predictable queuing behavior. This trend has direct commercialization implications for vendors and systems integrators targeting Industry 4.0 projects.

The market’s competitive topology is anchored by a combination of established semiconductor majors and specialist PHY vendors. The following players are central to the strategic picture for 2026:

Texas Instruments (Dallas, Texas, United States) — https://www.ti.com. TI’s strength lies in industrial- and automotive-qualified Ethernet PHY transceivers that emphasize high immunity, low latency, and integrated protection. Their product approach targets deterministic industrial use-cases and multi-protocol factory networks.

Analog Devices (Wilmington, Massachusetts, United States) — https://www.analog.com. ADI focuses on robust industrial PHY solutions engineered for time-critical communications in harsh environments, addressing the intersection of analog front-end performance and digital determinism.

NXP Semiconductors (Eindhoven, Netherlands) — https://www.nxp.com. NXP’s portfolio emphasizes scalable automotive and industrial transceivers, including single-pair Ethernet PMDs and offerings with ASIL B safety support and optional MACsec — a strategic fit for OEMs pursuing software-defined vehicle architectures.

Infineon Technologies (Neubiberg, Germany) — https://www.infineon.com. Infineon’s automotive-focused Brightlane PHY family delivers multi-gigabit copper connectivity for in-vehicle networks and supports automotive OEMs targeting high-bandwidth sensor domains.

Microchip Technology (Chandler, Arizona, United States) — https://www.microchip.com. Microchip is extending into next-gen optical PHYs up to 25 Gbps and emphasizes protocol features such as IEEE 1588 PTP and MACsec for long-reach networking and precision-timed systems.

Broadcom (San Jose, California, United States) — https://www.broadcom.com. Broadcom’s portfolio goes after hyperscale and enterprise platforms with high-performance 25G/50G PHY chips and optical DSPs tuned for multi-terabit transceiver applications and extremely low latency.

Intel (Santa Clara, California, United States) — https://www.intel.com. Intel’s controller products have moved toward more programmable networking and storage offload capabilities; their 2025R2 updates improve virtualization-centric offloads for multi-tenant cloud environments.

Collectively, these incumbents shape product roadmaps, interoperability standards, and supply-chain configurations. Our competitive analysis assesses not only product specs but ecosystem traction: reference designs, silicon-photonics partnerships, and the vendor’s ability to deliver regulatory qualifications on schedule.

Early 2026 — NXP launched production-ready 10BASE-T1S PMD transceivers targeted at low-cost multi-drop topologies for automotive and industrial edge use-cases, signaling increased momentum for SPE-based distributed architectures.

Late 2025 — Broadcom showcased high-bandwidth, co-packaged optics and introduced an industry-leading optical DSP optimized for 1.6T transceiver designs; this underscores a data-center migration toward higher lane rates and integrated optics.

Mid 2025 — Texas Instruments released deterministic 10/100 Mbps industrial PHYs designed for smart-factory latency constraints, highlighting that legacy-rate solutions remain relevant where deterministic behavior is required.

Throughout 2025 — Microchip and other vendors emphasized timing and security features (IEEE 1588 and MACsec) in their optical PHY roadmaps, reflecting customer demand for synchronized and secure long-reach links.

Our full study goes well beyond headline totals. It is built to inform board-level debates and hands-on engineering and procurement decisions with:

Transparent methodology and reconciled historicals (2020–2025) grounded in primary supplier interviews and channel checks.

Detailed forecast models (2026–2032) with scenario toggles for technology adoption rates, regional demand shifts, and alternative ASP trajectories.

Product and feature matrices comparing PHY and controller capabilities (timing, security, latency, power, and qualification status).

Supplier scorecards covering capacity, qualification timelines, roadmap alignment, and ecosystem partnerships.

Go-to-market and procurement playbooks tailored for hyperscalers, OEMs, Tier-1 automotive suppliers, and industrial integrators.

M&A and partnership opportunity maps identifying targets and the value levers they unlock.

Risk registers for supply-chain concentration, qualification delays, and regulatory shifts — with mitigation options and contingency cost estimates.

Interactive dashboards (subscriber access) to model the financial impacts of alternative network-architecture choices.

Note: This preview intentionally does not disclose the report’s fine-grained segment revenue tables or full regional/application breakouts. Those core breakouts are available through our full report portal and are the primary differentiator for companies executing targeted commercial strategies.

Prioritize qualification tracks: If your product or platform enters safety- or time-sensitive domains (automotive, industrial), prioritize suppliers that have demonstrable ASIL qualification plans and IEEE 1588/MACsec support.

Adopt a dual-sourcing strategy for critical PHY families to reduce concentration risk and to maintain negotiation leverage as demand tightens.

Align R&D investment to the bifurcation: invest in high-performance optical and co-packaged architectures for data-center plays while maintaining a cost-optimized SPE and low-latency copper roadmap for edge and automotive segments.

Use scenario modeling to stage capital: align network refresh budgets with the 7.3% CAGR trajectory but stress-test for accelerated adoption of SPE or co-packaged optics that could front-load demand.

Explore strategic M&A or partnership opportunities focused on optical DSPs, single-pair PHY IP, or certification stacks to accelerate time-to-market and reduce compliance risk.

By 2026, the Ethernet controller market presents both predictable growth and disruptive inflection points. The market’s steady expansion — from roughly USD 8.5 billion in 2020 to USD 12.6 billion in 2025 and a forecast surpassing USD 20 billion by 2032 — creates ample runway for incumbents and challengers. Yet success will flow to organizations that translate headline growth into differentiated product and commercial plays: those who align certification, time-and-security features, and optics/copper roadmaps with practical go-to-market and sourcing plans.

PW Consulting’s full Ethernet Controller Market report contains the complete segment-level analytics, vendor benchmarking, and executable playbooks that boards and executive teams need to convert market growth into sustainable advantage. This preview demonstrates the quality and direction of our analysis; access the full report to obtain the segment breakouts, detailed tables, and interactive models necessary for execution.

For detailed analysis of this topic, please visit the official page:Ethernet Controller Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com