Switch Mode Power Supply Transformers Market — Strategic Preview for 2026 Decision-Makers

As PW Consulting’s senior industry analyst, I present a concise, insight-rich preview of our full Switch Mode Power Supply (SMPS) Transformers Market study. This briefing is designed to clarify the strategic value the full report will deliver to corporate leaders making critical investment, product and sourcing decisions in 2026. It demonstrates the depth of our analysis while preserving the proprietary granularity available only in the full report.

Switch Mode Power Supply Transformers Market

Why this report matters for 2026

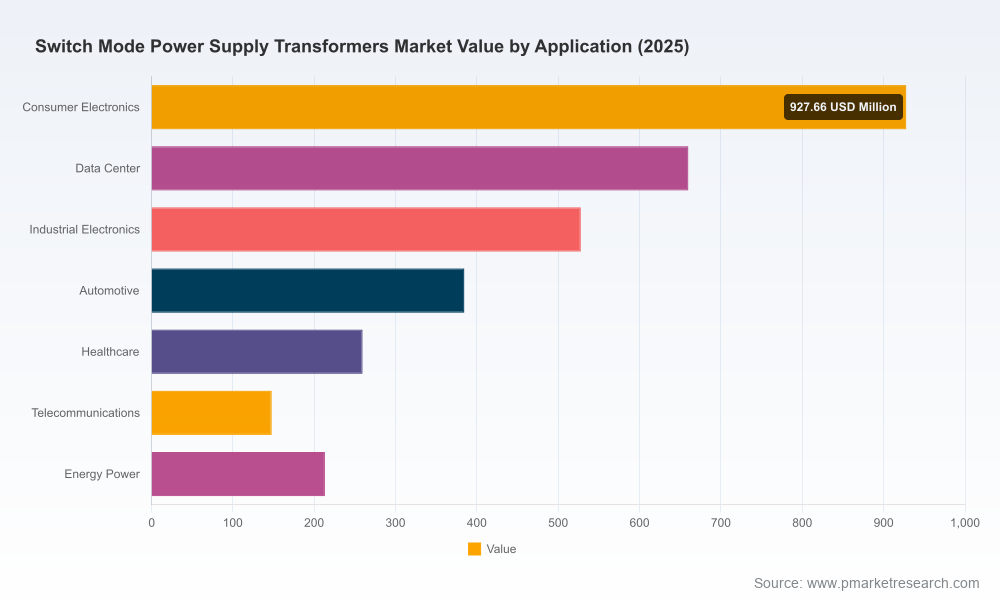

- The SMPS transformers market has moved from a mid‑single billion base in the early 2020s to an expanded industry scale today. After growing from roughly USD 2.5 billion in 2020 to about USD 3.12 billion in our 2025 base year, the market is forecast to continue expanding at a 4.9% CAGR through the 2026–2032 horizon, approaching roughly USD 4.36 billion by 2032.

- These macro dynamics matter: the market’s steady, above‑GDP growth rate signals persistent OEM demand across consumer, industrial, data center and automotive segments, while enabling new entrants and component specialists to scale niche technologies (planar, GaN/SiC‑optimized magnetics, high‑frequency miniature designs).

- For any 2026 strategic plan — whether launching a new product line, committing to factory investments, evaluating M&A targets, or negotiating long‑term supplier contracts — understanding the market trajectory, supplier concentration and technology inflection points is essential to de‑risk capital allocation and capture upside.

What the full study delivers (actionable elements)

Our full report is structured to move beyond description into prescriptive guidance. It contains:

Switch Mode Power Supply Transformers Market

- A transparent market model (base year 2025; historical 2020–2025; forecast 2026–2032) with bottom‑up revenue build and sensitivity scenarios that let you stress test revenue and margin outcomes under alternative demand, pricing, and input‑cost pathways.

- Technology roadmaps that map transformer topologies (from legacy flyback and forward designs to planar and resonant approaches) to application roadmaps (consumer, telecom, data center, automotive, healthcare, industrial). These bridge product R&D priorities to near‑term revenue opportunities.

- Supply chain and BOM analytics, including raw material exposure, component lead‑time stress testing, and recommended hedging or dual‑sourcing strategies to preserve gross margins under volatility.

- Commercial playbooks for OEMs and suppliers: product positioning, price‑architecture recommendations, and go‑to‑market segmentation strategies tuned for 2026 procurement cycles and two‑to‑five year roadmap horizons.

- Comparator dossiers and a deal‑sourcing matrix for M&A and JV activity, highlighting strategic fits based on technology, capacity, geography and customer overlap.

- Regulatory and reliability risk assessment: compliance touchpoints for safety standards, EMC/EMI trends, and qualification timelines that often dictate product launch calendars in mission‑critical end markets (data centers, healthcare, automotive).

Market structure and concentration — implications for strategy

The market exhibits a moderate concentration profile: the top three players cumulatively control a meaningful but not dominant share of industry revenues, while the top five extend that position further. This structure creates a marketplace where:

Switch Mode Power Supply Transformers Market

- Large incumbents maintain pricing power for high‑reliability, high‑volume contracts, particularly where qualification cycles and after‑sales support are decisive.

- Mid‑tier and specialized suppliers can win by offering tailored designs, rapid prototyping, and flexible manufacturing—advantages that matter for customers seeking differentiated miniaturization, higher switching frequencies, or bespoke isolation solutions.

- Private equity or strategic buyers can potentially consolidate specialized niches to build scalable platforms — provided they align technology roadmaps and manufacturing footprints effectively.

Technology and product trends to watch in 2026

- High‑frequency topologies and planar transformer designs: Pushing power density while reducing magnetic volume remains a core R&D theme. Expect customers to trade BOM complexity for smaller board area and improved thermal performance.

- GaN/SiC adoption at the converter level: As switching devices migrate to wide‑bandgap semiconductors, transformer designs are evolving to support higher dV/dt and higher operating frequencies. This creates product opportunities but also imposes stricter EMI and insulation design requirements.

- Resonant architectures (LLC) for efficiency: Demand from data centers and premium consumer electronics is accelerating adoption of resonant approaches where efficiency gains justify higher engineering cost.

- Customization vs. standardization tradeoffs: For high‑volume consumer lines, standard modules retain an economic edge. In industrial, automotive and medical segments, customized transformers command higher margins due to specialized specs and qualification hurdles.

Competitive landscape — what the players are doing and what it means

The study rigorously profiles leading and emerging suppliers. A selection of strategic positions observed across the competitive set:

- TDK Corporation (Tokyo) — combines broad design and manufacturing scale with deep application expertise. Their strategy centers on high‑power, high‑reliability solutions for industrial and data center customers where integration and lifecycle support are premium selling points. (See product lines: https://product.tdk.com/en/products/transformer/transformer/ac_dc-converter/index.html)

- Sumida Corporation (Tokyo) — emphasizes flexible manufacturing and a mix of custom and catalog offerings, making it attractive to customers needing rapid design cycles and moderate volumes. (https://www.sumida.com/)

- Wurth Elektronik (Waldenburg) — European strength in high‑frequency magnetics and a focus on automotive and industrial reliability parameters; well positioned for OEMs prioritizing certification and supply continuity. (https://www.we-online.com/)

- Murata Manufacturing (Kyoto) — compact, high‑power‑density modules for space‑constrained applications; strong in consumer and portable device markets. (https://www.murata.com/)

- Pulse Electronics, Bourns, Vishay, Coilcraft, Tamura, and others — a mix of niche specialists and diversified passive component houses offering differentiated value in planar designs, prototyping speed, and GaN/SiC‑ready solutions.

- Delta Electronics and Eaton — bring system‑level integration capabilities, bundling transformers with power modules and power distribution solutions; attractive for customers seeking turn‑key power platforms. (https://www.deltaww.com/, https://www.eaton.com/)

Across this set, common strategic actions include investing in planar manufacturing capability, expanding testing labs for wide‑bandgap qualification, and deepening customer co‑engineering collaborations. The players’ strategies are detailed in the full report alongside partner/opportunity maps for OEM procurement teams.

Commercial and supply‑chain playbook for 2026

- Supplier segmentation: class suppliers by capability (custom engineering, high‑volume standard parts, system integrators) and map procurement levers for each — qualification timelines, price elasticity, and service level tradeoffs.

- Capacity planning: stress‑test your production and supplier network against scenarios (demand surge, lead‑time normalization, tariff shifts). The report includes a scenario matrix with recommended mitigation actions and cost implications.

- Localization vs. centralization: evaluate near‑shoring, dual‑sourcing and regional inventory strategies against total landed cost and warranty exposure; our model shows where incremental logistics spend is justified by reduced time‑to‑market and lower qualification friction.

- Product roadmap alignment: prioritize engineering resources to transformer topologies that unlock the largest margin uplift in your target end markets; the study ranks topology/segment pairings by expected return on R&D investment.

How boards and executive teams should use this intelligence in 2026

- Investment committees: use the report’s bottom‑up projections and sensitivity analysis to size capital investments and to set realistic payback timelines for factory tooling or planar conversion projects.

- M&A teams: apply the competitor dossiers and deal matrix to shortlist targets that close capability gaps (e.g., planar manufacturing, GaN/SiC readiness, or regional assembly networks).

- Product and procurement leaders: adopt the playbooks to renegotiate supplier contracts with indexed pricing clauses, qualification milestones, and collaborative R&D roadmaps tied to volume ramps.

- R&D and systems architects: leverage the technology roadmaps to prioritize platform designs that de‑risk certification timelines in regulated end markets (automotive, healthcare, data center).

What we intentionally withhold here (and why you should read the full report)

This preview demonstrates the analytical depth and the practical takeaways. To preserve the value of our primary research and to provide the complete decision‑ready evidence base, we have not published the granular segment tables, regional and application splits, or supplier revenue breakdowns in this summary. The full report contains detailed tables, downloadable model files, supplier scorecards, and tailored scenario outputs that are essential for procurement negotiations, P&L modeling, and M&A diligence.

Next steps — how to convert insight into action

- Commission a tailored briefing: we offer a 90‑minute executive workshop that uses your product mix and customer portfolio to apply our model to your specific P&L scenarios.

- Acquire the full report and model: access to the downloadable forecast model lets you run custom scenarios (pricing shocks, technology adoption curves, regional demand shifts) and export decision‑grade outputs for board review.

- Engage our advisory team for rapid due diligence: if you are evaluating an acquisition or capacity investment, PW Consulting can deliver a sprint diligence pack that combines our quantitative model with supplier audits and on‑site checks.

For procurement and strategy teams preparing fiscal 2026 commitments, this market environment offers both predictable growth and critical inflection points driven by technology transitions and evolving qualification demands. PW Consulting’s full SMPS Transformers Market study equips leaders with the market model, competitive intelligence, and executable playbooks required to turn 2026 choices into durable competitive advantage. Request the full report and model to unlock the granular evidence that supports high‑stakes decisions.

For detailed analysis of this topic, please visit the official page:Switch Mode Power Supply Transformers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com