Timing Belt Market 2026: Strategic Imperatives from PW Consulting

As companies position for growth and resilience in 2026, timing belt manufacturers, suppliers, and end-users face a market shaped by structural contraction in the early 2020s and a clear, data-backed recovery through the early 2030s. PW Consulting’s latest Timing Belt Market study (base year 2025; historical coverage 2020–2025; forecast 2026–2032) synthesizes macro trajectories, competitive positioning, regulatory shocks, raw-material volatility, and technology trends into an actionable playbook for C-suite and investment teams. This preview highlights the study’s strategic value for decisions in 2026 without disclosing the granular segment intelligence that drives our premium insights.

Timing Belt Market

Market Trajectory: what the headline numbers mean for strategy

The timing belt market experienced a material contraction from the early 2020s into 2025, reflecting demand shocks in automotive production, supply-chain interruptions, and raw-material price movements. PW Consulting’s modeling shows a turning point in 2026 and a consolidated recovery through 2032 at a compound annual growth rate (CAGR) of 5.1%—a trajectory that converts near-term stabilization into multi-year opportunity.

Timing Belt Market

For executives, the headline implications are straightforward: 1) near-term priorities must focus on margin protection and working-capital agility during residual volatility, and 2) medium-term investments in product differentiation, production flexibility, and aftermarket capture are justified by predictable growth to 2032. The market’s recovery pace supports strategic bets—selective capacity increases, targeted R&D into energy-efficient belt materials and designs, and M&A to accelerate access to adjacent channels.

Timing Belt Market

Report composition: what the full study provides

- Methodology and baseline: transparent assumptions, base-year benchmarking (2025), and scenario-based forecasts through 2032 that stress-test demand and pricing under alternative macro paths.

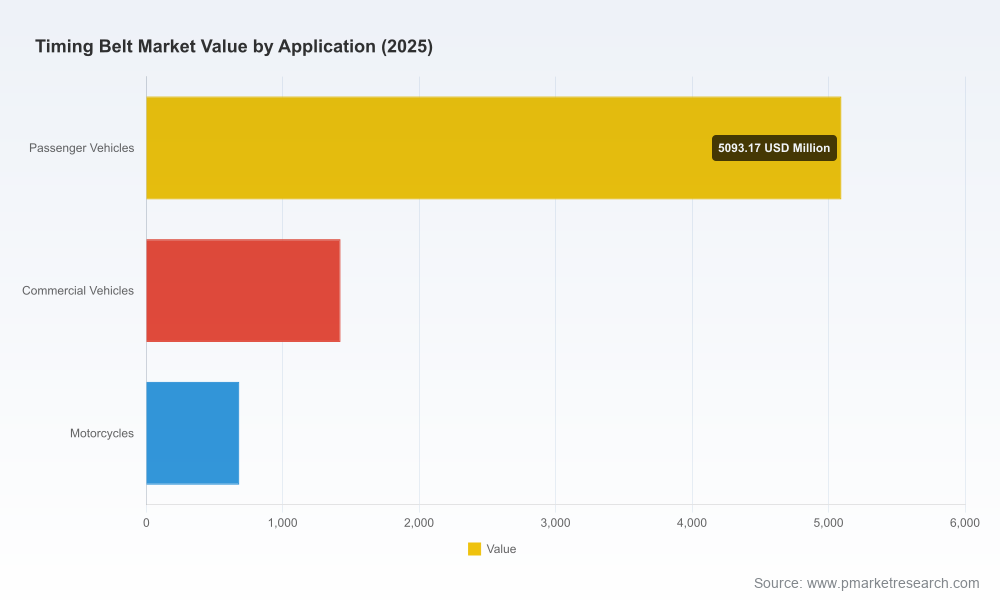

- Demand-side diagnostics: drivers across automotive OEM, aftermarket, commercial vehicles, motorcycles, and industrial automation with quantified sensitivity to vehicle production, replacement cycles, and energy-efficiency mandates.

- Supply-side mapping: factory footprints, capacity utilization, lead-time dynamics, supplier risk scoring, and logistics overlays that identify single-source dependencies and regional chokepoints.

- Cost and pricing model: detailed input-cost pass-through models that incorporate rubber and polyurethane feedstock dynamics, freight, and labor variance—presented as scenario outputs to guide procurement and pricing strategies.

- Regulatory and technology impact analysis: assessment of durability mandates, emissions and efficiency regulations, and the commercial implications of innovations like timing-belt-in-oil (TBIO) and advanced polyurethane formulations.

- Competitive intelligence and capability benchmarking: a structured view of market concentration, product portfolios, channel strengths, and near-term strategic moves across leading players.

- Go-to-market playbooks: tailored actions for OEM suppliers, aftermarket specialists, and industrial players—including partnership templates, aftermarket conversion strategies, and M&A screening criteria.

- Executive dashboard and investment memo: prioritized initiatives, expected ROI timelines, and a “fast-decision” checklist for 90-, 180-, and 360-day plans.

Competitive landscape — what differentiates winners in 2026

Our analysis shows a market that is moderately consolidated: the three largest players collectively command a meaningful share of the market, and the top five extend that dominance further. Concentration favors companies that combine breadth of product portfolio with deep channel relationships and operational scale. Below are strategic observations on named market leaders and challengers:

- Gates Corporation — A global leader in power transmission belts with robust exposure to both OE and aftermarket channels. Gates’ scale, brand recognition, and broad product range position it well to defend margin and pursue service-led differentiation (e.g., value-added aftermarket solutions and digital inventory tools).

- Continental AG (ContiTech) — Strong OEM credentials and an emphasis on engineered solutions for synchronization in both engines and industrial machinery. Continental’s advantage lies in design-to-spec partnerships with vehicle OEMs and industrial integrators, enabling premium positioning on reliability and lifecycle cost.

- Dayco Incorporated — A North American leader that has recently expanded TBIO technology into the aftermarket, creating an OE-equivalent service proposition for turbocharged vehicles. Dayco’s rapid product rollout and supply-chain refinements underscore the strategic value of bringing OE technologies into service channels.

- Optibelt GmbH — Specialist positioning in high-precision timing belts for industrial automation. Optibelt’s emphasis on low-friction and efficiency gains appeals to machine-builders seeking energy-optimized drives, and its trade-fair presence signals continued investment in brand-led business development.

- Schaeffler Group — Leveraging INA-branded timing belt kits and integrated service solutions for engine replacement and repair. Schaeffler’s systems approach—combining bearings and belt kits—creates defensible cross-sell opportunities in maintenance ecosystems.

- Winproflex & Xiamen Hee Industrial Belt — Cost-competitive specialists that focus on polyurethane and PVC synchronous belts for industrial transmission. Their agility and material expertise make them attractive partners for industrial OEMs, but they are exposed to feedstock price swings and standards-driven differentiation challenges.

Recent developments shaping near-term decision-making

- Regulatory change in the EU now mandates minimum durability thresholds for passenger-car timing belts—this raises the technical bar for suppliers and shifts economics toward higher-value, longer-life products.

- Dayco’s expansion of TBIO into the North American aftermarket demonstrates how OE tech migration into service channels can unlock large retrofit and replacement pools—an important precedent for players considering aftermarket penetration strategies.

- Trade-show activity and product launches from precision-focused suppliers signal ongoing investment in energy-efficiency and low-friction solutions, aligning with industrial customers’ demand for lower lifecycle energy consumption.

- Raw-material volatility—particularly polyol and isocyanate prices for PU belts—remains a structural risk that requires integrated procurement hedging and supplier collaboration to stabilize margins.

Strategic actions for 2026: prioritized, practical steps

- Revise product roadmaps for durability: Re-prioritize R&D and quality-validation programs to meet tougher durability mandates and to capture premium replacement cycles. Use accelerated life testing to shorten time-to-certification in regulated markets.

- Monetize OE-to-aftermarket technology transfers: Build commercial models to migrate OE innovations (e.g., TBIO) into the aftermarket with warranty-backed propositions and service-partner bundles.

- Hedge raw-material exposure: Establish multi-tier procurement strategies (e.g., long-term contracts, index-linked pricing, and geographic diversification) for rubber and polyurethane feedstocks.

- Enhance supply resilience: Identify second-source suppliers for critical components and consider nearshoring or regional buffer capacity for just-in-case resilience—balanced with cost economics.

- Adopt energy-efficiency as a differentiator: Translate low-friction and efficiency characteristics into quantified lifecycle-cost pitches for industrial customers and OEMs—support claims with independent testing data.

- Prepare M&A and partnership playbooks: Target bolt-on acquisitions that close capability gaps (e.g., PU compounding, TBIO expertise, or aftermarket logistics) and model integration synergies in a 12–24 month horizon.

How PW Consulting’s study accelerates 2026 decision cycles

Executives and investors need concise, credible inputs to allocate capital, set product priorities, and restructure commercial models. Our full report consolidates scenario-tested forecasts, supplier scorecards, and a prioritized action list that reduces decision latency. We present not just “what” is likely to happen, but the “how” of translating each forecast into procurement rules, R&D sprints, pricing guardrails, and M&A checklists—ensuring that teams can execute within 90–180 days of mandate.

Why this is a strategic moment

The intersection of regulatory durability requirements, technology transfers from OE to aftermarket, and the industrial drive for energy efficiency creates a window in which well-timed investments will compound. Firms that move early—by locking in feedstock strategies, validating longer-life products, and building aftermarket trust—will secure outsized returns as the market shifts from recovery to structured growth.

PW Consulting’s Timing Belt Market study is designed to be the operational blueprint for that movement. For readers prepared to translate the macro view into executable plans, the full report contains the detailed segment analytics, regional demand curves, and supplier scorecards necessary to prioritize investments and mitigate execution risk. This overview is intentionally selective: the most actionable intelligence—granular segment shares, regional demand splits, and company-level revenue mapping—is reserved for the full study.

To convert these insights into a tailored 90-day action plan for your organization, request the full Timing Belt Market report and our strategic briefing package. The next 12 months will determine who sets standards for durability, who monetizes OE-to-aftermarket migration, and who controls the most resilient supply chains—decisions that cannot wait.

For detailed analysis of this topic, please visit the official page:Timing Belt Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com