Anti-tumor Drug Market — 2026 Strategic Brief

Executive snapshot

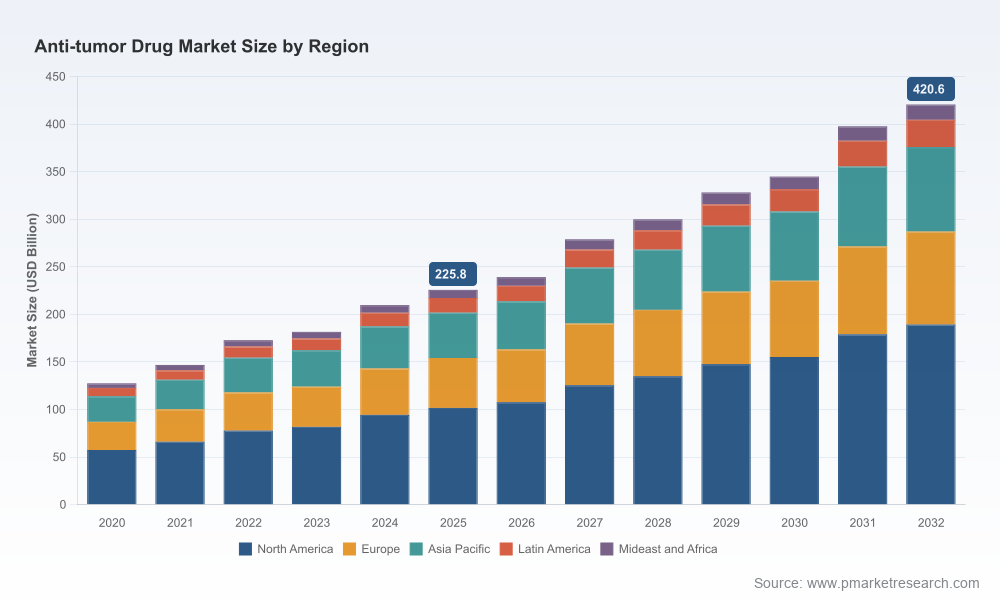

The global anti-tumor drug market is accelerating into a new phase of growth and strategic reconfiguration. Our PW Consulting market model (base year 2025; historical window 2020–2025; forecast period 2026–2032) projects a compound annual growth rate of 9.28% through 2032. The market expanded from roughly USD 127.5 Billion in 2020 to USD 225.8 Billion in 2025, and under our base forecast it reaches approximately USD 420.6 Billion by 2032. These aggregate dynamics create an environment in which selective scale, differentiated clinical value, and payer-savvy pricing strategies will determine winners and losers in 2026 and beyond.

Anti-tumor Drug Market

Why this report matters for 2026 corporate decision-making

- Rapid, sustainable growth — The market’s mid-high single-digit CAGR masks pockets of accelerated adoption driven by immuno-oncology combinations, targeted therapies informed by next-generation sequencing, and a rising tide of biologics and precision modalities. Executives planning R&D allocation, commercial launches, and M&A activity must align portfolios to capture both durable base growth and episodic uplifts from new approvals.

- Increasingly fragmented competitive economics — Market concentration remains modest (CR3 ≈ 25.4%; CR5 ≈ 29.7%), underscoring that beyond a few platform leaders, much of the market value is distributed among mid-sized innovators, specialty biotechs, and regional players. This fragmentation creates acquisition opportunities but also implies intensified pricing and distribution competition in many indications.

- Policy and supply fragility — A cluster of regulatory, patent, and reimbursement developments is compressing strategic timetables. Patent cliffs around flagship agents and evolving Medicare inflation-linked rebate rules create both revenue downside risk and windows for biosimilar/generic entrants. Simultaneously, recent FDA manufacturing interventions highlight operational dependencies that can delay approvals or restrict launches — an acute risk for companies preparing 2026 launches.

- Clinical and commercial interplay — Therapeutic value now hinges on clinical differentiation that translates into real-world outcomes and payer willingness to reimburse. New ERA approvals and altered clinical endpoints are changing the calculus for trial design and go-to-market sequencing. Our report provides the translation layer between trial readouts and commercial uptake.

What PW Consulting’s Anti-tumor Drug Market study delivers — the practical toolkit

This research is structured to be immediately actionable for C-suite leaders, corporate development teams, and commercial strategy groups preparing decisions in 2026. Highlights include:

Anti-tumor Drug Market

- Forward-looking revenue model (2026–2032) built from indication-level demand drivers, adoption curves, and dynamic pricing assumptions. The model is scenario-enabled to stress-test launch timing, trial outcomes, patent cliffs, and payer reforms.

- Clinical-to-commercial impact matrices that map trial endpoints to expected formulary positioning and likely reimbursement levels under three payer archetypes.

- Launch playbooks and sequencing frameworks for first-in-class and best-in-class assets, including recommended attrition budgets, sample strategies, and key opinion leader engagement templates.

- M&A and partnering scorecards identifying attractive acquisition targets by strategic fit, development-stage, and commercialization readiness — with a prioritized shortlist for buyers pursuing near-term scale vs. long-term platform building.

- Supply-chain and manufacturing risk dashboards that quantify probability-weighted delivery risk from single-source biologics and identify mitigation levers (second sourcing, tech transfers, CMO partnerships).

- Regulatory and reimbursement playbooks that translate recent FDA guidance, accelerated approvals, and inflation-linked rebate regimes into operational responses for 2026 filing and launch teams.

Competitive landscape — strategic implications for select incumbents and innovators

The market features a mix of platform incumbents, diversified pharma, and focused biotechs. Our report profiles leading firms and distills strategic choices they face in 2026.

Anti-tumor Drug Market

- Merck & Co., Inc. — With a flagship PD-1 franchise, Merck must navigate lifecycle management amid looming exclusivity pressures on blockbuster immunotherapies. Strategic priorities include label expansion through combination trials, aggressive real-world evidence generation to defend reimbursement, and selective bolt-on acquisitions to broaden modalities beyond checkpoint inhibition.

- Bristol Myers Squibb — An immuno-oncology leader that benefits from diversified oncology assets. BMS’s near-term task is optimizing combination regimens and managing overlap across portfolios to maximize net-present-value across indications while containing development spend.

- F. Hoffmann‑La Roche Ltd — Roche’s integration of diagnostics with therapeutics continues to be a competitive advantage for targeted programs. For Roche, monetizing companion diagnostics and ensuring diagnostic access in key markets will be a central 2026 focus.

- AstraZeneca — Strong in targeted therapies and immune approaches, AstraZeneca must balance rapid launch execution with payer negotiations in indications where rapid uptake is expected. Precision patient segmentation will be critical for premium pricing.

- Eli Lilly, Novartis, Pfizer, Gilead, Amgen, Sanofi, Johnson & Johnson — These diversified players face similar trade-offs: invest in next-wave biologics and ADCs, or pursue inorganic growth to fill modality gaps. For each, our report highlights which assets to prioritize for internal development vs. external sourcing.

- Specialty innovators (Debiopharm, PharmaMar, BeyondSpring, Novocure, Adcentrx, and others) — Smaller players are the primary source of modality innovation (ADCs, tumor treating fields, novel targeted small molecules). Their strategic options in 2026 are clear: retain high-value assets for premium partnership or accelerate exits where manufacturing and commercialization scale is a limiting factor.

Recent catalytic events and what they signal for strategy

- Fresh approvals in late 2025–early 2026 (including targeted agents and novel mechanism approvals) demonstrate continued scientific momentum and provide concrete launch opportunities in 2026. These approvals also underscore the commercial importance of rapid payer engagement and post-marketing evidence strategies.

- Clinical program initiations and new mechanism trials in early 2026 indicate active replenishment of oncology pipelines — an important signal that R&D investment remains strong despite pricing pressures.

- Regulatory decisions tied to manufacturing quality have recently constrained approval pathways, illustrating that regulatory strategy must include manufacturing readiness as a core launch criterion — not an afterthought.

Industry dynamics shaping risk and opportunity

Executives must plan against a composite of structural and event-driven forces:

- Patent cliffs and exclusivity expirations compress revenue horizons for several legacy agents, accelerating the need for either next-generation product lines or strategic partnerships to preserve top-line momentum.

- Evolving regulatory guidance on clinical endpoints requires closer alignment between clinical development teams and commercial leaders earlier in program design.

- Reimbursement policy changes — notably inflation-linked payer rebate regimes — mean that list price alone no longer predicts net revenue; manufacturers must model net realized prices under multiple policy stress scenarios.

- Manufacturing and supply-chain constraints remain a persistent risk, and must be quantified in launch probability models used for portfolio prioritization.

How to use this research in the 2026 planning cycle

- Investment committees: use our scenario-enabled NPV matrices to set R&D allocation ceilings, prioritize phase transitions, and define go/no-go criteria sensitive to reimbursement risks.

- Business development teams: leverage our M&A scorecards to structure offers that reflect realistic commercial potential under constrained reimbursement and patent timelines.

- Commercial leaders: implement the launch playbooks and payer engagement sequences recommended for early-2026 filings to compress time-to-reimbursement and accelerate uptake.

- Manufacturing and supply functions: adopt the risk dashboards to set redundancy budgets and CMO selection criteria that materially reduce delivery risk for critical launch windows.

Trailer — what we deliberately withhold here (and why you should download the report)

This brief intentionally surfaces the strategic narrative and high-level levers that will matter in 2026 while withholding the granular segmentation tables, region- and indication-level revenue breakdowns, and company-level market shares that form the core of deal-ready intelligence. Those datasets — including our full scenario model, detailed payer pricing corridors, and confidential target shortlists — are available in the full PW Consulting Anti-tumor Drug Market report. If you are preparing a 2026 budget, competitive bid, or M&A thesis, that granular layer will materially alter valuation and execution choices.

Next steps

For boards, strategy teams, and deal desks accelerating plans for 2026, PW Consulting’s work offers both a high-resolution forecast and the operational playbooks to convert forecasts into executable outcomes. Contact our team to arrange a briefing where we will walk through the forecast scenarios, stress-test your portfolio, and supply the full dataset and model licensing required for transaction diligence or launch planning.

For detailed analysis of this topic, please visit the official page:Anti-tumor Drug Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com