Exosome Research Products Market Growth Driven by Rising Demand for Non-Invasive Diagnostics

Other |

2026-06-24 15:20:38

As PW Consulting’s lead industry analyst, I present an executive briefing on the Ion Exchange Membrane (IEM) market that frames the near-term strategic choices facing producers, equipment integrators, investors, and policy teams in 2026. This is not a datasheet: it is a decision-oriented synthesis designed to show the analytical depth underpinning our full market study while directing readers to the primary report for the granular segment-level intelligence that will inform capital allocation, product development, and regulatory strategy.

Ion Exchange Membrane Market

The IEM market sits at the intersection of three structural trends that will determine commercial winners in the next strategic cycle: decarbonization-driven demand for electrolyzers and fuel cells; accelerating non-fuel applications such as advanced water treatment and electrodialysis; and rising regulatory pressure on fluorinated chemistries. Our base-year assessment (2025) places the global market at approximately USD 1.09 billion, following steady growth from roughly USD 850 million in 2020. Under the trajectory model used in our study, the market expands to roughly USD 1.6 billion by 2032, representing a compound annual growth rate of approximately 5.5% over the forecast window.

Ion Exchange Membrane Market

That steady, mid-single-digit growth conceals important inflection points. Demand is being reshaped by the ramp-up of green-hydrogen projects, municipal and industrial desalination upgrades, and an expanding set of electrochemical separation use-cases. At the same time, supply-side dynamics — raw material volatility, potential PFAS restrictions, and regional policy incentives — are creating both risk and opportunity for incumbents and challengers alike.

Ion Exchange Membrane Market

Our report is built to be operationally useful for strategy teams in 2026. It blends market sizing and scenario modelling with procurement-level intelligence and project economics, so that executives can move from high-level insight to tangible decisions. Highlights include:

The full report supplements these tools with downloadable models and a proprietary decision rubric we use when advising clients on entry, expansion, or exit scenarios.

Market concentration is moderate. The top three firms account for under forty percent of industry revenues, and the top five approach roughly half of the market — a structure that supports competition but also rewards scale and specialized IP. This balance creates scope for both regional champions and specialized technology leaders to coexist.

Key corporate archetypes in the market include:

Representative players discussed in the study (selected for their strategic relevance rather than exhaustive coverage) include multinational chemical firms known for perfluorinated products and membrane franchises, Japanese and European hydrocarbon specialists, and North American polymer innovators pursuing next-generation AEM and ionic polymer platforms. Each has differentiated routes to market, IP portfolios, and exposure to regulatory risk from emerging PFAS restrictions and supply-policy proposals.

For buyers and OEMs, these developments mean that supply assurance, certification pathways, and qualification timelines must be revisited in 2026 procurement cycles. For producers, momentary advantage will accrue to firms that can scale low-risk chemistries quickly while maintaining margins on high-performance fluorinated offerings where regulation still permits.

We distil the market intelligence into four priority plays that senior executives should consider when setting 2026 plans:

Secondary but material actions include building a regulatory monitoring cell to translate evolving PFAS-related legislation into production and product strategy, and setting aside targeted discretionary capital for opportunistic M&A should valuation windows open during policy-driven dislocations.

Our comprehensive study provides the full analytic stack behind this briefing: granular segmentation across membrane types, applications, and regions; supplier-level revenue and capacity estimates; supply-chain maps with supplier-level concentration analysis; technology readiness assessments; and downloadable financial models that translate membrane demand into plant economics under alternative scenarios.

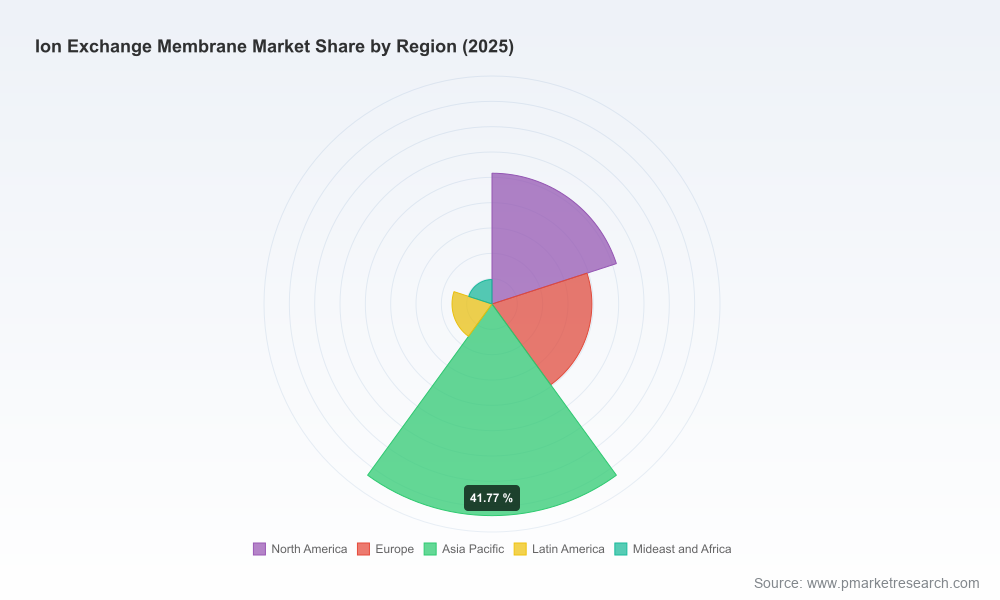

We intentionally withhold the fine-grained segment tables and region/application revenue splits in this briefing to preserve the strategic integrity of the study and to ensure that clients engaging the full report obtain the actionable line-item intelligence necessary for investment and procurement decisions.

For executives making strategic decisions in 2026, the window to act is now. The market trajectory indicates steady growth, but near-term winners will be those that convert regulatory and raw-material headwinds into differentiated supply positions, validated alternative-chemistry products, and secure OEM relationships for the hydrogen and water-treatment value pools. The choices made this year — particularly around chemistry diversification, capacity flexibility, and partnership models — will determine whether a firm captures the high-margin early-adopter business or competes in commoditized volume later on.

To convert these insights into a tailored action plan, request the full PW Consulting Ion Exchange Membrane Market study. The report supplies the segment-level analytics, supplier scorecards, and financial templates you will need to underwrite investments and negotiate long-term supply contracts with confidence.

For detailed analysis of this topic, please visit the official page:Ion Exchange Membrane Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com