Positron Emission Tomography (PET) Scanners Market — Strategic Preview for 2026 Decision-Making

Executive summary

PW Consulting’s latest market intelligence on Positron Emission Tomography (PET) scanners synthesizes five years of historical performance (2020–2025) with a forward-looking forecast horizon (2026–2032) to support strategic investment, product, and commercialization decisions in 2026. The global PET scanners market has demonstrated steady expansion, increasing from roughly USD 508 million in 2020 to an estimated USD 688 million in our 2025 base year, and is projected to grow at a compound annual growth rate (CAGR) of 5.9% over the 2026–2032 forecast period. By 2032 the market crosses the USD 1 billion threshold, reflecting both sustained clinical demand and accelerated product innovation.

Positron Emission Tomography (PET) Scanners Market

Why this study matters for 2026 strategic plans

- Timing. 2026 is a pivot year: regulatory clarity in major markets, successive product launches and manufacturing scale-ups are converging to reshape competitive positions.

- Capital allocation. The market’s mid-single-digit CAGR signals predictable growth, enabling more disciplined multi-year investment planning for R&D, capacity expansion, and service networks.

- Competitive dynamics. A concentrated vendor landscape — with the top three and top five firms controlling a substantial portion of global supply — intensifies the importance of portfolio differentiation, strategic partnerships, and targeted commercial plays.

Market trajectory and macro dynamics

Our analysis positions the PET scanners market as a technology-led medical imaging subsegment with consistent demand driven by oncology diagnostics, neurology and cardiology applications, and the increasing clinical adoption of advanced PET form factors (total-body PET, digital PET, and PET/MRI hybrids). From a macro perspective, the sector’s fundamentals remain solid: an established clinical value proposition, expanding reimbursement support in select markets, and capital availability for manufacturers scaling production or entering new geographies.

Positron Emission Tomography (PET) Scanners Market

Key macro datapoints in the report provide the backbone for scenario planning: historical sizing through the 2025 base year, a 2026–2032 forecast window, and a 5.9% CAGR for the forecast period. These metrics are modeled in parallel scenarios — conservative, base, and accelerated — to stress-test capital investments, manufacturing scale decisions, and pricing strategies under differing adoption speeds for next-generation platforms.

Positron Emission Tomography (PET) Scanners Market

Technology and clinical adoption trends

Several technical and clinical trends are reshaping demand patterns and value propositions:

- Total-body and extended axial-length PET systems are changing throughput economics and enabling new clinical protocols by imaging larger anatomical volumes in a single session. Recent product launches have placed these platforms at the center of vendor roadmaps.

- Hybrid imaging (PET/CT, PET/MRI) and improvements in digital detector technology are improving image sensitivity and quantitative accuracy, which expands PET’s clinical utility and supports more complex diagnostic and therapy-monitoring workflows.

- Radiopharmaceutical developments and closer integration between imaging devices and tracer supply chains are increasingly strategic. Manufacturers that can align scanner capabilities with practical radiochemistry and logistics have competitive advantages in certain clinical niches.

Competitive landscape — positioning and recent moves

The market is concentrated: the top three firms capture a significant majority of sales and the top five further consolidate supply. This concentration raises barriers to entry for new hardware players but creates opportunity for niche innovators and service providers that can partner with incumbents.

Leading and relevant players analyzed in the full study include:

- GE HealthCare Technologies Inc. — notable for its Omni Legend and long-axial Omni 128 cm total-body PET/CT platforms, with recent manufacturing capacity expansion in Wisconsin to support higher-volume installations.

- Siemens Healthineers AG — maintains a broad PET portfolio including advanced PET/CT and PET/MRI systems; strategic M&A and regulatory wins have strengthened its molecular imaging capabilities.

- Koninklijke Philips N.V. — leverages its Vereos and Ingenuity TF platforms, focusing on digital PET performance and integrated clinical workflows.

- Canon Medical Systems Corporation, Shimadzu Corporation, Neusoft Medical Systems, and regional vendors — each pursue differentiated technical trade-offs and regional market approaches, from high-performance hybrid systems to cost-competitive clinical scanners.

- Specialist and emerging players such as Positron Corporation, Mediso Ltd., MinFound, and RefleXion Medical — these firms are notable for targeted product designs (preclinical-to-clinical bridges, compact systems, and real-time tumor-tracking PET/CT) and recent financing or regulatory developments that could accelerate commercial rollouts.

Recent developments underscore dynamic repositioning: GE’s U.S. manufacturing expansion and milestone installations; Siemens’ regulatory clearance for next-generation PET/MRI and strategic acquisition of a radiopharmaceutical business; and targeted funding rounds for smaller clinical system vendors. These moves not only reflect company-specific strategies but also signal where OEMs expect the clinical and commercial opportunities to emerge in 2026 and beyond.

Regulatory and reimbursement environment — implications for 2026

Policy developments in 2025–2026 materially affect near-term strategic choices. Highlights covered in the report include:

- Regulatory modernization efforts and device/drug interface clarifications in major jurisdictions that streamline approval and lifecycle processes for PET drugs and imaging platforms.

- Updates to national coverage determinations and reimbursement listings that directly impact clinical adoption economics for PET procedures.

- Targeted policy initiatives in large emerging markets to accelerate approval and reimbursement for high-end imaging equipment.

For decision-makers, this means regulatory strategy and reimbursement engagement must be front-loaded in 2026 planning cycles. Proactive regulatory alignment, early payer evidence packages, and pilot reimbursement agreements will accelerate adoption for new platforms and support pricing integrity.

Practical strategic implications and recommended actions for 2026

We translate the market intelligence into prioritized actions for different stakeholders. The full report contains executable templates; here are the headline plays we recommend for 2026:

- For OEMs with scale: accelerate modular manufacturing capacity and field-service capabilities to support faster install cycles and ensure uptime guarantees; pursue tuck-in acquisitions in radiopharma or software to broaden serviceable addressable market.

- For mid-size and regional vendors: focus on niche clinical workflows, cost-to-own optimization, and partnerships with local radiopharmacies and large hospital systems to secure installation pipelines.

- For new entrants and VC investors: prioritize capital allocation toward high-value differentiators (e.g., total-body imaging, AI-enabled quantification, or integrated theranostics workflows) and identify early-adopter healthcare systems as anchor customers.

- For healthcare providers and imaging network operators: re-evaluate procurement decisions against throughput and lifetime operating costs; negotiate bundled agreements that include service, software upgrades, and tracer supply where appropriate.

- For radiopharmaceutical companies and service providers: co-develop evidence packages with imaging OEM partners to support reimbursement submissions and clinical adoption programs.

What PW Consulting’s full report delivers — practical, actionable modules

The complete study goes beyond this executive preview and includes:

- Detailed historical and forecast market models (by product form factor, application class, and region) with scenario sensitivity to adoption rates and pricing curves.

- Actionable go-to-market playbooks: procurement negotiation templates, service network build plans, and capital expenditure models tailored for different organizational profiles.

- Regulatory and reimbursement roadmaps for prioritized markets, including recommended evidence generation and engagement timelines to support 2026 submissions and coverage requests.

- Competitive benchmarking and replace-or-upgrade matrices with supplier scorecards, technology risk assessments, and potential partnership targets.

- Investment and M&A decision support: valuation drivers, target screening criteria, and integration checklists focused on radiopharma and software assets that materially increase scanner value.

Transparency and what we are not disclosing in this preview

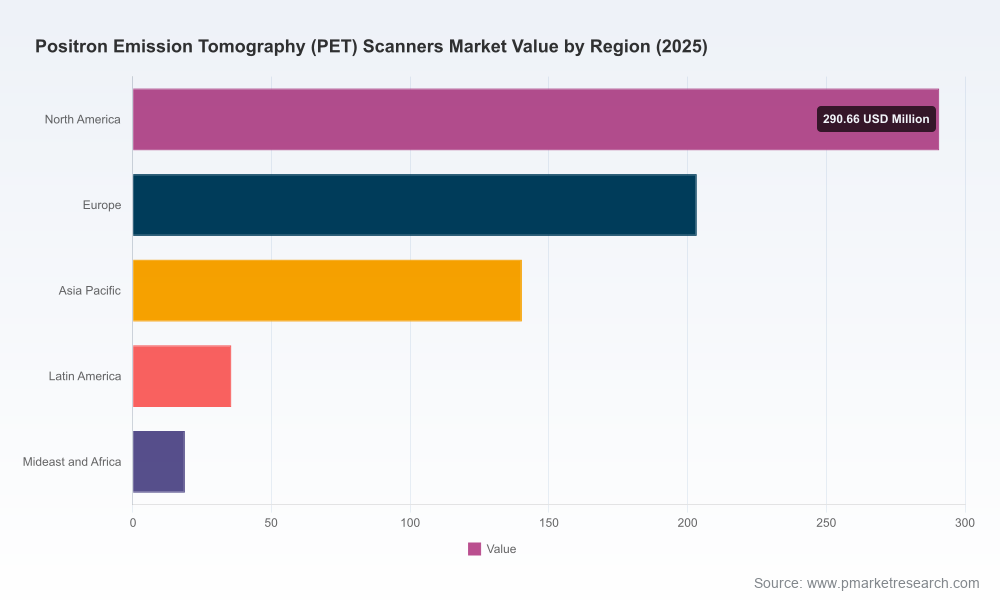

To preserve the strategic integrity of the study and to follow our “trailer” principle, this preview intentionally omits granular segment-level tables, detailed regional splits and application-specific revenue figures that appear in the full report. Those line-item datasets, along with downloadable modeling workbooks and supplier-specific revenue trajectories, are available to clients who access the full deliverable via our report portal.

Conclusion — preparing for decisive moves in 2026

As 2026 unfolds, firms that succeed will combine disciplined capital allocation with focused technological differentiation and proactive regulatory and reimbursement engagement. The PET scanners market offers predictable growth and high-value clinical impact, but competitive intensity and regulatory shifts mean that first-mover advantages and well-orchestrated partnerships will determine market leadership.

PW Consulting’s full Positron Emission Tomography (PET) Scanners Market report provides the empirical models, tactical playbooks, and competitive intelligence needed to convert 2026 strategic intent into measurable commercial outcomes. For teams planning capital, product, or M&A moves this year, the study is structured to accelerate decision cycles and reduce execution risk.

To access the full dataset, scenario models, and prescriptive modules referenced in this preview, please visit the report page. PW Consulting will also schedule bespoke briefings to align insights with your organization’s specific strategic questions.

For detailed analysis of this topic, please visit the official page:Positron Emission Tomography (PET) Scanners Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com