Malocclusion Market Overview: Key Drivers and Challenges 2025 –2032

Health |

2026-06-08 08:52:31

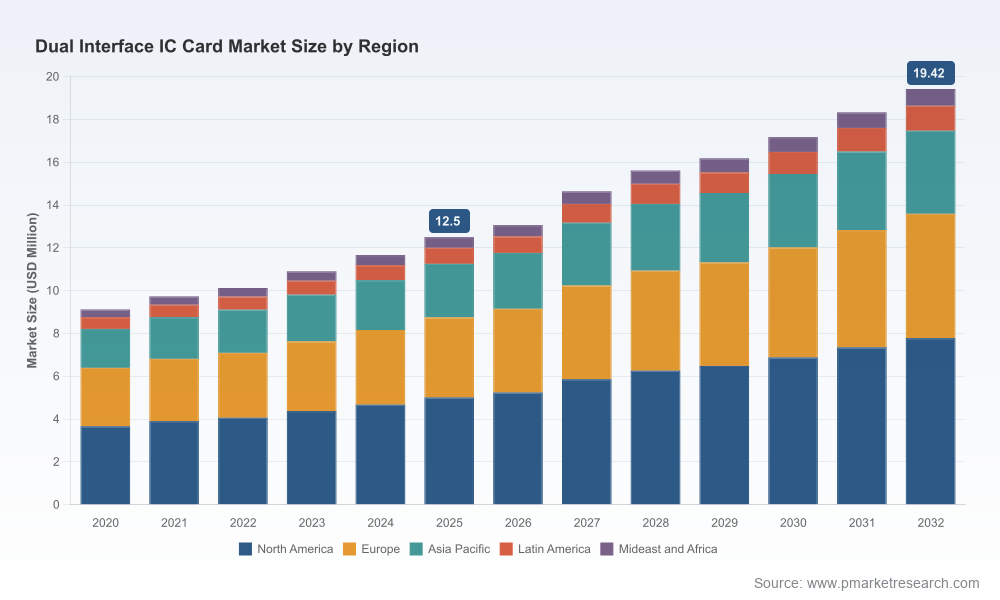

As organizations map strategy for 2026 and beyond, the Dual Interface IC Card market represents a blend of steady growth, structural complexity and tactical risk. Our latest PW Consulting market study tracks the market from 2020 through a 2026–2032 forecast window and shows a resilient expansion trajectory: the market grew from roughly USD 9.1 million in 2020 to about USD 12.5 million in 2025 and is projected to approach USD 19.4 million by 2032, implying a mid-single-digit compound annual growth rate (CAGR) of approximately 6.0% over the forecast period. These headline dynamics mask important inflection points — from supply-chain reconfiguration to product-level differentiation — that will determine winners and laggards in the next three to five years.

Dual Interface IC Card Market

Capital allocation and M&A: Persistent, predictable market growth invites targeted investments, but the industry remains sufficiently fragmented: market concentration remains low by global industry standards. Executives must therefore choose between organic scale-up, bolt-on acquisitions, and strategic partnerships to secure volume, shorten time-to-market and capture higher margin segments.

Dual Interface IC Card Market

Product and technology roadmaps: Dual interface designs (contact + contactless) are becoming baseline for payment, identity and transportation cards. Roadmaps must prioritize module packaging, antenna integration approaches and chip security features — but with careful assessment of supplier resilience and certification timelines.

Dual Interface IC Card Market

Sourcing and manufacturing footprints: The combination of tariff uncertainty and protracted lead times for critical components requires scenario-based sourcing strategies and selective nearshoring to protect time-sensitive programs.

The market’s historical trajectory shows steady adoption across payment, identity and transit use cases, with technology upgrades and renewals driving recurring demand. Our base-year calibration (2025) and forecast (2026–2032) reflect three structural demand drivers: technology refresh cycles tied to security standards, migration to multifunction cards (payment + ID + access), and service-led growth from personalization and on-demand issuance. The 6.0% CAGR to 2032 therefore reflects an equilibrium between broader digitization tailwinds and intermittent supply-side constraints that intermittently compress short-term growth.

Two related stressors will shape supplier economics and program risk in 2026:

Tariffs and trade policy: Recent escalations in tariffs and a newly initiated Section 232 inquiry into semiconductors create plausible scenarios for duties or export restrictions that could be implemented as early as 2026. These measures affect not only chips themselves but also manufacturing equipment and substrates — categories that are fundamental to dual-interface card production.

Component availability: Extended lead times for discrete MOSFETs and other semiconductors — now regularly exceeding 52 weeks in benchmark industry reports — materially increase schedule risk for card assemblers, especially for projects with tight go-live windows (e.g., bank reissues, government ID rollouts).

Combined, these factors argue for three operational priorities: build multi-sourced RFQ pipelines, validate alternate BOMs for critical sub-assemblies, and model tariff scenarios into unit-cost sensitivities for 2026 procurement cycles.

The sector includes a mix of global system suppliers, chip vendors, card manufacturers and service players. Market concentration metrics indicate a low-to-moderate consolidation level, leaving room for strategic differentiation. Key competitive vectors we highlight are packaging innovation, personalization & issuance services, and programmable security platforms.

Infineon Technologies AG (Germany) — renowned for coil-on-module and dual-interface module packaging technologies. Infineon’s strength lies in providing field-proven, plug-and-play modules with long operational lifecycles, making them a compelling partner for programs emphasizing durability and predictable integration.

IDEMIA Group (France) — a recognized leader in EMV contact and contactless payment solutions. IDEMIA’s breadth across financial and government segments and its work on metal-interface options position it well for premium-tier card programs and national-scale identity initiatives.

Giesecke+Devrient (G+D) (Germany) — combines EMV dual-interface card production with strong personalization services. Their integrated scope from chip to card issuance is a strategic advantage for customers seeking single-vendor accountability for certification and lifecycle management.

CPI Card Group Inc. (United States) — a US-headquartered card manufacturer that recently expanded capabilities through acquisition activity to accelerate on-demand production and personalization. This move underlines a broader industry shift toward fast-turn issuance and localized services.

Eastcompeace Technology (China) and Watchdata Systems (China) — significant manufacturers focused on payment and tolling applications respectively, often competing on scale and cost-efficiency for volume programs.

Kona I (South Korea) — a specialist in Java Card chips supporting advanced security features (DDA, biometrics), relevant for customers incorporating biometric binding or programmability at the card level.

Strategically, buyers should map vendor selection to three program archetypes: high-security national programs (emphasize integrated security and certification), large-volume payment issuance (prioritize scale and unit-cost predictability), and premium/feature-rich cards (value innovation in packaging, biometrics, and personalization). Recent M&A and capability shifts (for example, the 2025 acquisition activity by a US issuer services provider) reinforce the importance of evaluating partners for both manufacturing and issuance agility.

Baseline (moderate growth, persistent constraints) — Expect continued mid-single-digit growth; primary risk driver is extended supplier lead times. Tactical response: extend inventory buffers for critical long-lead components, renegotiate service-level agreements and prioritize projects via an economic-value lens.

Tariff shock — If Section 232 actions or new tariffs are imposed, landed costs could rise meaningfully for suppliers reliant on certain imports. Tactical response: accelerate qualification of alternate manufacturing locations, and deploy hedging (contractual and FX) to dampen margin volatility.

Supply recovery & personalization surge — A softening of supply constraints plus rapid adoption of on-demand issuance could push premium pricing for value-added services. Tactical response: invest in personalization capacity and software-enabled issuance platforms now, while selectively pursuing partnerships with local printers and system integrators.

The study is designed as a playbook for 2026 decision-making. Highlights include:

Actionable forecasting: A bottom-up demand model calibrated to 2020–2025 history and stress-tested across tariff and supply scenarios for 2026–2032.

Vendor scorecards: Comparative assessments across technology, manufacturing footprint, certification readiness and personalization capabilities for the leading vendors and promising challengers.

Supply-chain risk heatmaps: Component-level lead-time and concentration analysis, plus tiered mitigation strategies (second-source lists, safety stock triggers, contract levers).

Commercial playbook: Pricing sensitivity templates, TCO calculators for outsourcing vs. in-house issuance, and negotiation playbooks for multi-year supply agreements.

Regulatory impact models: Ready-to-use templates to quantify potential tariff scenarios and a checklist for certification timing and compliance across major jurisdictions.

Go-to-market and M&A frameworks: Criteria for build-buy-partner decisions, integration roadmaps for acquisitions and a short-list methodology for target screening.

We intentionally present the study as a strategic trailer: the report demonstrates empirical depth and prescriptive tools while preserving granular segment tables and supplier revenue matrices for authorized access. This approach helps executives quickly validate strategic direction while protecting the actionable micro-data reserved for subscribers and clients.

Compile internal demand and pipeline assumptions and map them to our baseline and tariff scenarios to understand exposure.

Run a fast vendor due-diligence using our vendor scorecards to identify at least two qualified second-sources for each critical component line.

Begin a targeted personalization capacity build or partnership negotiation if customer programs require sub-48-hour issuance turnaround.

Incorporate our tariff sensitivity outputs into 2026 budget cycles and update procurement KPIs to include lead-time and concentration metrics.

For executives, the imperative is straightforward: treat growth as certain but execution as conditional. The Dual Interface IC Card market offers reliable expansion underpinned by technology renewal and expanding use cases, yet the operational environment is defined by policy volatility and long-lead components. The right combination of diversified sourcing, vendor selection aligned to program archetypes, and investment in personalization/on-demand issuance will determine which players convert market growth into sustainable margin improvement.

For full access to the detailed segmentation tables, supplier revenue matrices, and the downloadable scenario models that support the forecasts and playbooks summarized here, please consult the full PW Consulting Dual Interface IC Card Market report on our website.

For detailed analysis of this topic, please visit the official page:Dual Interface IC Card Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com