Global Limestone Market Growing at 3.9% CAGR Through 2032

Other |

2026-06-19 10:05:37

The global vacuum degasser market has entered a sustained expansion phase. After growing from an estimated USD 163.15 million in 2020 to USD 215.0 million in 2025 (base year), the market is projected to advance to approximately USD 344.8 million by 2032. This trajectory reflects a compound annual growth rate (CAGR) of about 6.98% across the 2026–2032 forecast window. For executives planning 2026 investments, procurement cycles and product roadmaps, these aggregate dynamics translate into predictable demand growth, shifting buyer expectations and a widening set of commercial opportunities — but also into operational and regulatory complexity that needs to be actively managed.

Vacuum Degasser Market

Capital allocation: With market volumes rising consistently, capital planning for equipment upgrades, factory automation and aftermarket service capacity must move from ad-hoc to strategic multi-year budgeting. The 2026 planning window is a critical inflection point to lock in suppliers and avoid equipment lead-time risk as order backlogs grow.

Vacuum Degasser Market

Supply-chain positioning: Procurement teams should reassess single-supplier dependencies for pumps, control systems and vacuum chambers. Early 2026 sourcing decisions will determine the 2026–2028 delivery cadence.

Vacuum Degasser Market

Regulatory and safety compliance: Recent regional shifts toward stricter metallurgical and environmental standards are driving adoption. Companies that incorporate regulatory-driven specs into product design and installation planning now will avoid costly retrofits and project delays.

Competitive playbooks: Given the market’s structure, there is room for both technology-led premium plays and low-cost scale plays. Firms must choose between niche specialization, vertical integration, or bolt-on consolidation — and begin executing in 2026.

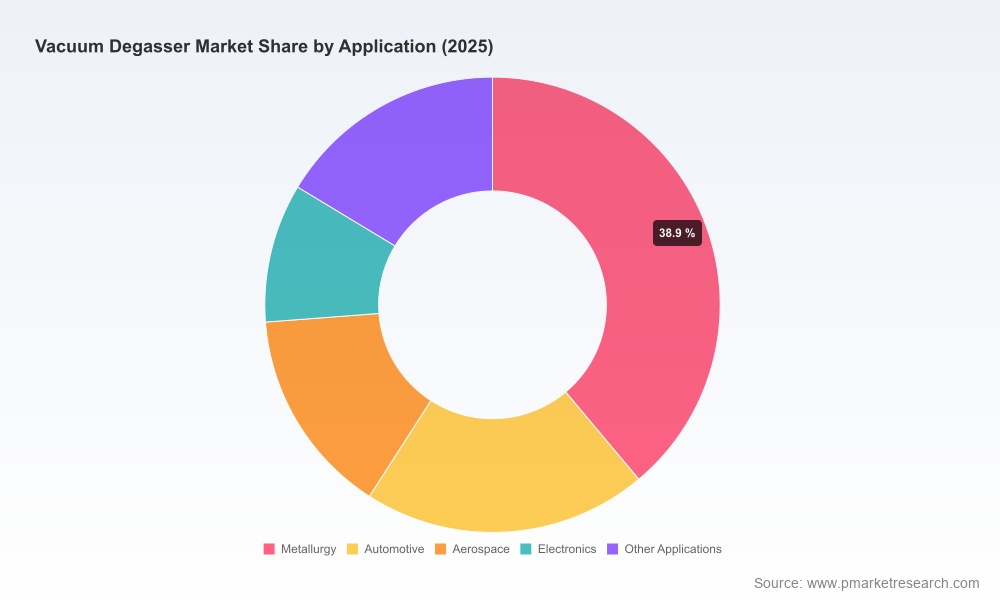

Demand drivers are multi-disciplinary: metallurgy and steel refining practices continue to push for higher material purity; the automotive and aerospace sectors require lighter, higher-integrity metal components; and industrial process and laboratory applications demand precision degassing for quality and repeatability. These end-market dynamics collectively underpin the steady market growth observed through 2020–2025 and the forecasted expansion to 2032.

On the supply side, the market remains characterized by a diverse set of equipment providers — from heavy industrial integrators supplying vacuum tanks for secondary steel refining, to compact membrane degassing modules for analytical and laboratory use. Recent industry developments illustrate both demand momentum and supply-side scaling: selected equipment manufacturers announced factory capacity expansions and new production batches to meet growing orders, while deliveries of drilling-oriented degassers into the oil & gas sector underscore cross-industry applicability.

Regulatory shifts are a material dynamic. For example, standardization efforts and regional regulations have raised the baseline specification demands in some foundries, accelerating retrofits and new system purchases. At the same time, a non-trivial share of installations experienced scheduling delays in recent years due to heightened compliance checks — a practical constraint that buyers and suppliers must price into project timelines.

The vacuum degasser market displays a low concentration profile: the combined share of the top three and top five suppliers remains limited, indicative of a fragmented competitive landscape. This fragmentation creates both opportunities and hazards. On one hand, buyers can negotiate on capability and service terms with multiple specialized suppliers; on the other, suppliers face margin pressure and the constant need to differentiate through service, technical performance, or integration capability.

GN Solids Control (China): GN’s ZCQ series targets drilling fluids and mud-gas separation, offering API-certified and explosion-proof models. The firm has been active in delivering systems to the oil & gas sector and scaling production capacity to meet demand.

SMS group (Germany): A systems integrator in secondary steel refining, SMS embeds vacuum tank degassers into molten-metal workflows to tackle dissolved gases (oxygen/hydrogen/nitrogen). Their solutions are positioned for heavy industrial customers seeking integrated furnace-to-casting control.

Spirotech (United Kingdom): Known for its S600 and S250 vacuum degassers, Spirotech focuses on HVAC/hydronic system gas removal with fully automatic controls — a strong play in building services and industrial fluid loops.

Stourflex (United Kingdom): Offers vacuum degassers with smart control units, often integrated into demanding piping and filtration applications where compactness and control are priorities.

AVE Applied Vacuum Engineering (United Kingdom): Specialized in vacuum degassing chambers, pumps and kits for industrial, biotech and laboratory solvent-degassing applications — a supplier that caters to high-precision, small-batch users.

Biotech Fluidics (Sweden): Producer of stepper-motor vacuum pumps and controllers for inline membrane degassing, particularly geared to analytical HPLC and mixed aqueous/organic fluids — a niche technology vendor with strong product-level integration.

Leybold (Germany): Provides vacuum pump systems and engineered solutions for metallurgical degassing processes, supporting high-spec steelmaking and refining operations.

These firms exemplify the breadth of the market: from large systems integrators working at the furnace scale to specialist vendors addressing analytical and hydronic niches. Strategic decision-makers should map their preferred supplier archetype (integrator vs. specialist) and align procurement, service and product roadmaps accordingly.

Robust market sizing and transparent methodology explaining how historical data (2020–2025) was reconciled with forecast scenarios (2026–2032).

Demand tomography by application and region (note: detailed segment tables are reserved for the full report), with adoption curves and replacement cycles modelled for strategic CAPEX planning.

Supplier scorecards and a validated vendor matrix that capture product performance, service footprint, certified standards and aftermarket economics.

Procurement playbooks and contract templates designed to minimize lead-time and compliance risk, including supplier SLAs, warranty structures and spare-parts policies.

Unit-level CAPEX/OPEX models, total cost of ownership calculators and sensitivity analyses on key inputs (energy cost, installation delays, component lead times).

Regulatory and safety compliance checklist with practical mitigation strategies — aligned to recent standardization activity and reported installation impacts.

Innovation radar cataloguing emerging degassing technologies, materials improvements and automation opportunities for predictive maintenance and remote monitoring.

M&A heatmap and strategic options for consolidation, bolt-on acquisition targets and partnership playbooks for 2026–2028 value capture.

Client-ready slide decks, procurement-ready appendices and raw data tables for integration into corporate planning systems.

For OEMs: Prioritize modular, serviceable designs and build aftermarket subscription offerings (maintenance + analytics). This increases lifetime revenue per installation as volumes grow.

For foundries and steelmakers: Treat degasser procurement as a systems integration project. Early involvement of controls and emissions compliance teams reduces retrofit risk and installation delays.

For services & rental firms: Expand rapid-deployment fleets and train field teams in dual-domain competencies (mechanical + vacuum controls) to capture short-term upticks driven by project backlogs.

For investors and M&A teams: Target technology-rich niche players with defensible IP or sticky aftermarket relationships; consolidation can drive scale advantages in procurement and service delivery.

For component suppliers: Lock in long-lead components via multi-year agreements and invest selectively in localized production to reduce logistics risk and meet regional certification timelines.

Regulatory-induced schedule slips: track permit approval times and compliance audit outcomes as leading indicators (recent data shows a meaningful share of installations have faced compliance-related delays).

Order book and backlog velocity: an acceleration in closed orders versus delivered units is an early signal of tightening capacity and potential price pressure.

Supplier capacity announcements and factory expansions: new production lines and announced batches are forward signals of supply-side scaling; conversely, production disruptions are downside triggers.

Energy and raw-material input costs: monitor for margin pressure on vacuum pump and chamber manufacturers, and stress-test TCO models under energy price volatility.

This preview was designed to orient boardrooms, strategy teams, procurement heads and investors ahead of the 2026 planning cycle. It highlights the macro foundations — steady historical growth, a forecast path to 2032 and a fragmented competitive set — while teasing the practical tools and data tables that large buyers and investors will need to execute with confidence.

PW Consulting’s full Vacuum Degasser Market report contains the segment-level tables, regional adoption curves, benchmarking matrices and model templates that are intentionally excluded from this preview. For access to the complete dataset, vendor scorecards and executable go-to-market playbooks, please consult our report page or contact PW Consulting directly.

For detailed analysis of this topic, please visit the official page:Vacuum Degasser Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com