Animal Wound Care Market Trends and Forecast

Health |

2026-06-02 11:22:42

As healthcare organizations and their external service partners enter a decisive phase in 2026, the role of Business Process Outsourcing (BPO) within healthcare delivery and financing is shifting from cost arbitrage to strategic capability. This PW Consulting briefing frames the market dynamics you need to act on this year: the macro trajectory, the competitive moves redefining delivery models, the regulatory forces compressing margins and raising compliance risk, and the pragmatic levers purchasers and providers should prioritize when scoping partnerships or making investment commitments.

Healthcare BPO Market

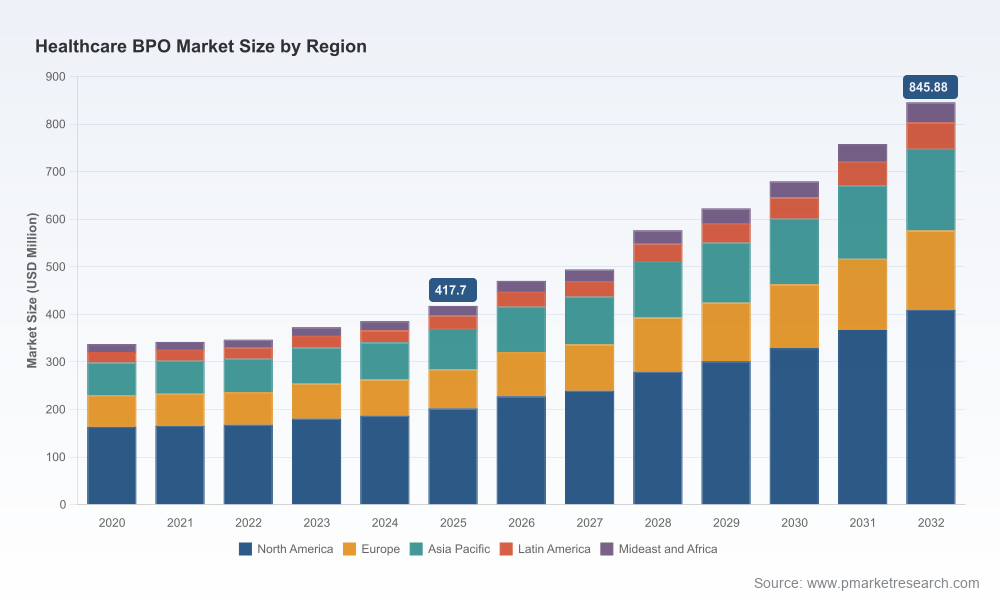

Our research establishes that the global Healthcare BPO market — valued at approximately USD 417.7 million in the report base year (2025) — is on a sustained growth path, projected to expand at a compound annual growth rate (CAGR) of 10.7% through the forecast window. By the end of the forecast period, the market is expected to roughly double from its 2025 baseline. That pace of expansion, combined with a market concentration profile that indicates meaningful scale among the top providers yet ample room for specialist entrants, creates both opportunity and complexity for buyers and investors.

Healthcare BPO Market

For executives making decisions in 2026, the implications are straightforward: the market will continue to reward providers and clients that treat BPO not as an operational commodity but as a strategic extension of revenue cycle, quality, and compliance capabilities. Choices made this year about partner selection, contractual risk-sharing, technology adoption, and talent location will materially influence financial performance and regulatory exposure through the rest of the decade.

Healthcare BPO Market

Regulatory pressure and payment design: Recent CMS policy changes and ongoing programs tied to readmissions and physician fee schedules are tightening revenue levers for hospitals and physician groups. These regulatory shifts elevate the value of BPO partners that can demonstrably improve clinical-coding accuracy, reduce preventable readmissions, and align documentation with evolving reimbursement rules. Expect buyers to prioritize partners with proven compliance protocols and programmatic outcomes over those offering simple cost-offload.

Digitization and automation: The maturation of RPA, AI-assisted coding, and cloud-enabled revenue cycle platforms is enabling providers to reimagine the division of labor between in-house teams and outsourced partners. Strategic outsourcing in 2026 will favor providers who combine people-plus-tech service models that deliver measurable throughput gains and higher clean-claim rates.

Workforce geography and resiliency: Talent location remains critical. Recent capacity expansions by major players reflect continued investment in offshore/nearshore hubs to secure scalable clinical coding and back-office capacity. However, buyers are increasingly evaluating workforce resiliency, multi-site redundancy, and employee retention programs as part of vendor due diligence.

Value-based care and risk alignment: As more payers and providers embrace downside risk, BPO vendors that can support advanced risk adjustment, analytics, and contract performance reporting will command a premium. The most successful offerings will integrate clinical analytics into operational workflows rather than operating as separate reporting functions.

This study is structured to inform both strategic planning and near-term procurement. Highlights include:

Market sizing and trend scaffolding: A clear reconciliation of historic performance (2020–2025) and a granular forecasting framework through 2032, enabling scenario testing for conservative, base, and aggressive adoption pathways.

Buyer playbooks: Contract templates and negotiation checklists tailored for revenue cycle, payer services, and life-sciences outsourcing engagements that align service-level metrics to clinical and financial outcomes.

Provider go-to-market frameworks: Segmentation-based GTM strategies for incumbents and challengers, including value propositions, bundling strategies, and a prioritized roadmap for technology investments that demonstrate return within 12–24 months.

Risk and compliance matrix: A concise, action-oriented compliance and regulatory impact assessment tailored to CMS policy changes, readmission reduction programs, and physician fee schedule updates — mapped to operational controls and audit playbooks.

Due diligence toolkit: Vendor scorecards, integration readiness assessments, and M&A diligence checklists calibrated for both strategic buyers and private equity sponsors considering platform or tuck-in acquisitions.

The market sits between consolidation and specialization. A modest portion of market share is held by the largest players, but vertical specialists and technology-focused mid-market firms are growing rapidly by solving niche, high-value problems.

Optum: As a dominant end-to-end player, Optum leverages scale, integrated technology stacks, and a global delivery footprint to serve complex health systems. Recent expansion of operations in the Philippines underscores its strategy to secure capacity and regional labor arbitrage while embedding offshore talent into higher-value clinical coding and analytics roles. For buyers, Optum’s breadth offers the advantage of integrated solutions but requires scrutiny on contract flexibility and clarity of outcomes measurement.

Ensemble Health Partners: Ensemble’s focus on deep, strategic revenue cycle partnerships with health systems positions it as a premier choice where clinical alignment and long-term performance improvement are prioritized. The company’s recent strategic engagements with sizable regional systems demonstrate market appetite for partnership models where the vendor becomes an operational co-owner rather than a transactional supplier.

TruBridge: TruBridge’s niche strength in community and rural hospital spaces — combining EHR optimization with RCM and financial solutions — makes it a compelling partner for providers focused on operational stabilization and digital modernization. Its positioning highlights an important theme: smaller and rural providers increasingly require tailored outsourcing solutions, not scaled-down enterprise offers.

GeBBS Healthcare Solutions: GeBBS represents the archetype of technology-enabled BPO, with a focus on revenue cycle, risk adjustment, and coding services. Their model showcases how mid-sized vendors can accelerate growth by integrating advanced workflows and outcome-based metrics into client contracts.

Recent moves in the market underscore the competitive momentum: notable partnerships announced in 2025 signal that health systems are seeking deeper, long-term integrations with revenue cycle partners, while capacity expansions by large providers reflect continued investment in delivery scale and geographic diversification.

Shift to outcome-linked contracting: Buyers should tie a meaningful portion of BPO fees to demonstrated improvements in metrics that matter under current reimbursement rules (readmission reductions, documentation accuracy, denial reduction). Providers should be prepared to report at the patient- and contract-level.

Prioritize composable technology: Opt for vendors that expose modular APIs and offer transparent data lineage. This reduces vendor lock-in and accelerates value capture from automation pilots.

Design multi-vector workforce strategies: Balance offshore scale with local clinical expertise to manage regulatory risk and client relationships. Redundancy planning and skills development for clinical coders and clinical documentation improvement (CDI) teams is table stakes.

Embed analytics into operational loops: Rather than periodic reporting, insist on continuous, near-real-time analytics that drive daily workflows — denial routing, prior-authorizations, and CDI interventions.

Use M&A strategically: For investors and strategic acquirers, target assets that add differentiated analytics or domain expertise (e.g., risk adjustment for Medicare Advantage, complex surgical coding) rather than duplicating scale alone.

Run a rapid procurement refresh: use the vendor scorecards to re-evaluate your top three vendors against outcome metrics tied to CMS policy changes.

Execute a tech-gap assessment: map your current RPA/AI capabilities to the five high-impact workflows we identify and prioritize two pilots with clear ROI gates.

Redesign at least one contract to include shared-risk elements and a 12-month performance remediation timeline.

This introduction outlines the strategic contours that will shape outsourcing decisions across health systems, payers, and life-science firms in 2026. PW Consulting’s full Healthcare BPO Market report provides the validated data tables, regional and application breakdowns, vendor benchmarking scorecards, contractual templates, and scenario-based financial models that will turn these insights into executable plans. For buyers, providers, and investors committed to making informed, defensible choices this year, the complete report is the operational playbook you’ll want at the table.

Contact PW Consulting to access the full dataset, proprietary vendor matrices, and bespoke advisory engagements that convert analysis into results.

For detailed analysis of this topic, please visit the official page:Healthcare BPO Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com