Minimalist Silver Jewellery: Timeless Elegance and Modern Style

Other |

2026-06-02 10:15:12

As companies plan capital allocation, sourcing strategies and go-to-market moves for 2026, an evidence-based, scenario-ready view of the Potassium Phosphate Monobasic (KH2PO4 / MKP) market is now a strategic imperative. Our PW Consulting study — built on an audited base year of 2025 and a granular historical series from 2020–2025 — synthesizes market dynamics, supplier economics, regulatory headwinds and demand-side shifts into an actionable playbook. At the macro level, the global market reached approximately USD 800.0 Million in 2025 and, under our baseline trajectory (2026–2032), the market is projected to grow at a compound annual growth rate (CAGR) of 3.5%, surpassing the USD 1 Billion threshold during the forecast window. This report is designed to convert that macro-line into concrete, risk-calibrated actions for buyers, producers and investors.

Potassium Phosphate Monobasic Market

Timing of capacity investments: modest, steady growth (CAGR ~3.5%) implies capacity additions must be selective and aligned to differentiated end-markets rather than broad-based volume plays. Overbuilding risks margin erosion in a market that is neither hyper-growth nor entirely commoditized.

Potassium Phosphate Monobasic Market

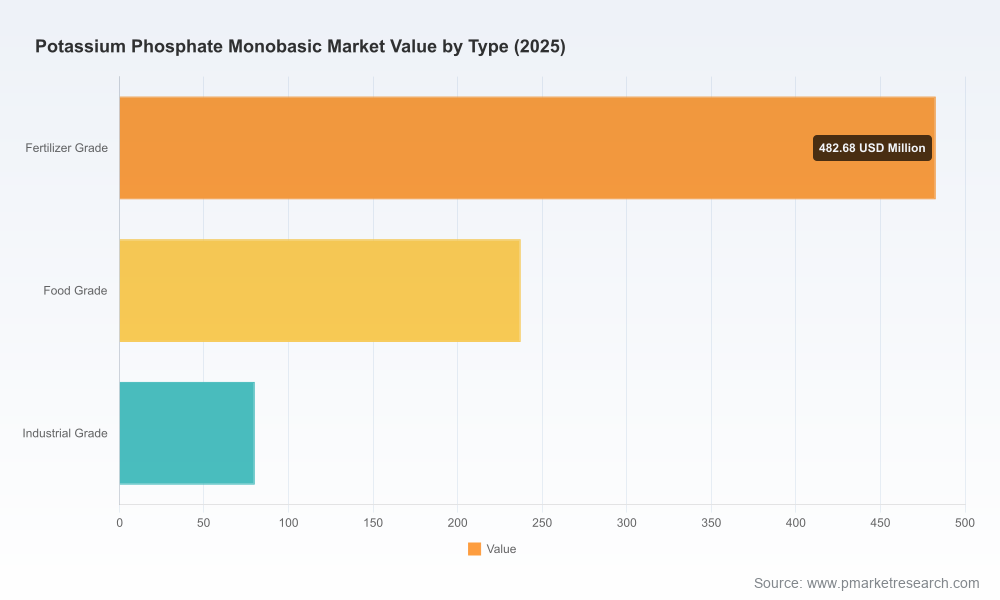

Portfolio prioritization: KH2PO4 serves at least three distinct demand pools — crop nutrition, food & beverage and pharmaceuticals — each with different margin profiles, regulatory regimes and supplier requirements. Strategic focus, not breadth for its own sake, will drive superior returns.

Potassium Phosphate Monobasic Market

Sourcing resilience: supply concentration and logistics exposures mean procurement leaders should shift from lowest-cost buys to supplier scorecards that embed quality, lead times and regulatory certifications.

The KH2PO4 market sits at the intersection of agricultural modernization, specialty food ingredients demand and pharmaceutical ingredient supply chains. Key dynamics shaping 2026 decisions include:

Gradual agricultural shift to specialty fertilizers: Farmers and agribusinesses are allocating incremental spend to water-soluble and foliar nutrients. This sustains steady demand for high-purity MKP variants but also raises expectations on traceability and product performance.

Premiumization in food & beverage: KH2PO4’s role as a buffering and nutrient additive in select food segments supports steady, quality-driven demand growth rather than bulk-volume expansion.

Regulatory and quality uplift in pharma: Pharmaceutical-grade KH2PO4 requires tighter quality systems and supply continuity. This raises barriers for commodity suppliers but rewards those who invest in quality certifications and validated manufacturing processes.

On the supply side, feedstock and energy price volatility, trade policy frictions and logistical bottlenecks intermittently compress margins. These factors, combined with a market concentration profile where the top three players account for roughly 45% of supply and the top five roughly 60%, favor regional specialists and integrated suppliers who can control costs and quality across the value chain.

The market is characterized by a mix of small-to-mid-sized manufacturers and a handful of larger suppliers. Our competitive review highlights the following archetypes and strategic options:

Local specialists with focused capacity: Several firms operate smaller, flexible plants that serve regional demand and specialty niches. Example: M.M. Arochem Pvt. Ltd (Vasai, India) operates a compact, flexible manufacturing line (approx. 20 MT/month), enabling rapid product customization for local customers. These players win on responsiveness, lower overhead and niche product grades.

Export-oriented producers: Certain producers in Asia have built export-oriented models emphasizing cost competitiveness and scale. Their advantage is price-led market capture in less quality-sensitive segments.

Quality- and compliance-focused suppliers: Firms targeting pharmaceutical and premium food markets differentiate through compliance (GMP, pharmacopeia standards) and validated manufacturing. Examples include suppliers that position bulk supply for pharma clients and food-grade customers, emphasizing audited systems and traceability.

For companies evaluating M&A or partnership opportunities in 2026, the market concentration metrics (CR3 ≈ 45%, CR5 ≈ 60%) suggest meaningful value can be unlocked through consolidation at regional levels — especially where product grade and quality accreditation create defensible moats. However, any consolidation thesis must be stress-tested against feedstock exposure and regulatory compliance costs.

We structured the research to be directly usable by strategy, procurement and business development teams. Key deliverables include:

Top-down and bottom-up demand models covering 2020–2032 with scenario analyses (base, upside, downside) that allow users to adjust assumption levers such as fertilizer penetration rates, food-grade premium adoption and pharma demand shocks.

Supply-side maps and a cost-curve framework that ranks facilities by delivered cost zones and highlights short-run marginal cost sensitivities to key feedstocks and energy inputs.

Competitive benchmarking with supplier profiles, capability scorecards and a stewardship assessment that rates suppliers on quality systems, environmental compliance and logistical resilience.

Commercial playbooks: go-to-market options for producers (e.g., contract structures, channel mixes, formulation partnerships) and procurement playbooks for buyers (dual-sourcing templates, quality clauses, price-variation mechanisms).

M&A screening tool: an acquisition heat-map identifying target archetypes, synergies and integration risks, along with a sensitivity matrix that models ROI under alternate regulatory and price environments.

Executive dashboards and DealRooms: one-page KPIs for board reviews and investor decks, plus an interactive model for stress-testing strategic choices.

Align capacity additions with premium end-markets: Prioritize investments that enable food-grade and pharma-grade production or bespoke fertilizer formulations. These segments reward quality certification and supply reliability.

Build supplier scorecards and long-term contracts: For procurement teams, move beyond spot buys. Lock in quality and timing with staggered contracts that include performance KPIs and quality audit rights.

Hedge feedstock and logistics exposure: Use a mix of financial hedges and operational mitigants (dual sourcing, regional buffer stocks) to smooth margin volatility driven by raw-material swings.

Pursue selective bolt-on M&A: Look for regional producers with quality credentials or formulation know-how that can be integrated at low capex. Avoid conglomerate-style roll-ups without a clear integration plan for quality and regulatory systems.

Invest in regulatory preparedness: For suppliers targeting pharma and food chains, early investment in validated quality systems and documentation yields higher contract stickiness and price premiums.

Design a modular pricing model: Adopt contract structures with built-in cost pass-throughs for feedstock and energy to protect margins while keeping commercial offers competitive.

Our approach combines primary interviews, plant-level cost analysis, and demand-side modelling calibrated to observable trade and consumption patterns between 2020 and 2025, then extended via scenario-based forecasts to 2032. We do not offer simple point predictions; instead, we provide levers and dashboards so leaders can tailor the model to their beliefs and risk tolerances. The deliverable pack includes editable models (USD, revenue in Million units), supplier scorecards and an actionable M&A heat map that simplify executive decision cycles.

Operational leaders: request the supplier scorecard module and logistic risk map to immediate integrate into your procurement planning for 2026.

Commercial teams: pilot a dual-contract approach in one priority market (e.g., high-value food or pharma accounts) and measure margin improvement versus spot procurement.

Investors & M&A teams: use our acquisition heat map to shortlist targets and validate the integration ROI under the three forecast scenarios.

To preserve the tactical value of this analysis while enabling a fast review, this article highlights the study’s strategic thrusts and operational levers without disclosing granular segment-level data and proprietary models. For full access — including regional and application breakout models, supplier-level benchmarking, price curves and downloadable scenario models — visit our full report page or contact PW Consulting to schedule a tailored briefing. Our team will walk you through the dataset, validate assumptions against your context, and help convert the insight into your 2026 action plan.

For detailed analysis of this topic, please visit the official page:Potassium Phosphate Monobasic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com