Smart Grid Modernization Creating New Opportunities for Split Transformer Industry

Other |

2026-05-08 07:45:30

As companies plan their 2026 strategies in anti-infectives and adjacent therapeutic portfolios, Metronidazole presents a complex mix of low-growth stability, regulatory reclassification risk, and pockets of commercial differentiation. PW Consulting’s new Metronidazole Market study (base year 2025; forecast 2026–2032) combines a granular commercial model with regulatory foresight and supplier-level intelligence to turn routine market visibility into actionable strategy. This preview outlines why the study is strategically valuable for boardrooms and corporate strategy teams preparing investments, M&A, or product lifecycle actions in 2026 — while reserving the full segmentation and tactical playbook for readers of the full report.

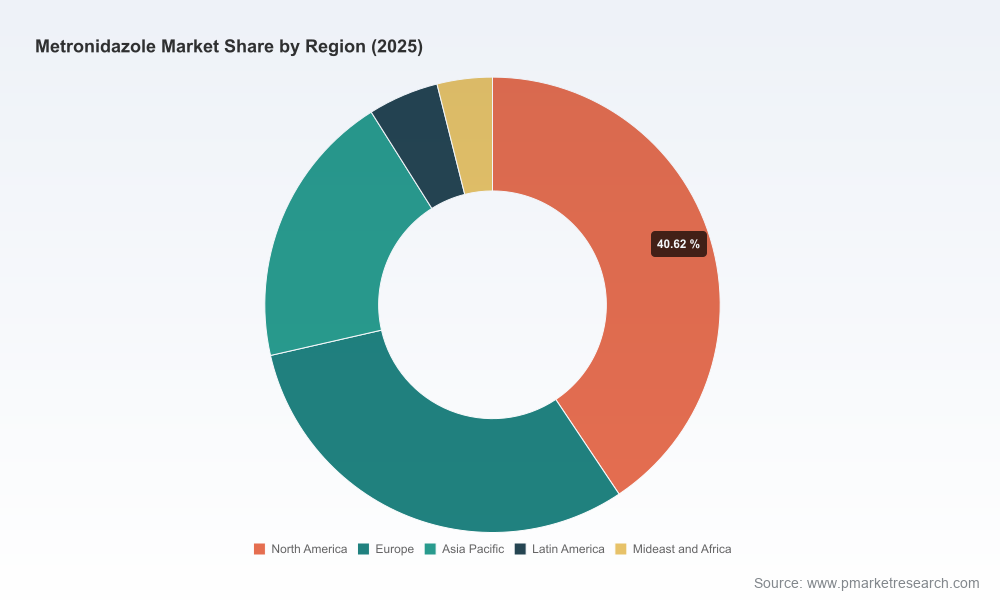

Metronidazole Market

Predictable but not static demand: The market demonstrated steady growth through the early 2020s, rising from the low‑80s (Million USD) in 2020 to just over 104 million USD in 2025, and is forecast to continue expanding to roughly 129 million USD by 2032. The compound annual growth rate over the forecast window is modest at 3.01%, reflecting a mature therapeutic category with resilient baseline demand.

Metronidazole Market

Concentration and competitive dynamics: Market concentration indicates meaningful scale advantages. The three-largest players account for roughly half of market value, while a broader top-five cohort captures around two‑thirds. That structure creates space for mid‑tier competitors to compete on manufacturing cost, differentiated formulations, or targeted branded offers.

Metronidazole Market

Regulatory and stewardship pressures are reshaping value: Recent regulatory events — from label revisions and new approvals to global antimicrobial classification changes — are changing how payers and hospitals think about utilization and procurement. These developments create both headwinds (stewardship-driven volume constraints) and opportunities (differentiated, targeted formulations with stronger clinical narratives).

Regulatory signals matter more than ever. Two discrete signals in 2024/2025 require strategic recalibration: first, regulatory confirmations that legacy tablet products remain on market registries; second, the WHO’s reclassification of nitroimidazoles as “Highly Important Antimicrobials.” Combined with label updates (including recent revisions to injection labeling), these signals are increasing scrutiny on prescribing and hospital formulary placement. Companies must bake stewardship risk into volume projections and model shorter, more volatile demand cycles for some indications.

Generic approvals shift pricing dynamics. The FDA’s approvals of generic vaginal and topical metronidazole formulations in 2024 have accelerated substitution patterns where branded premiums once prevailed. For manufacturers and marketers, this means faster lifecycle erosion for undifferentiated products but also clearer paths to scale via AB-rated generics — if cost and supply can be optimized.

API and CDMO strategy is a persistent lever. A handful of established API producers and CDMOs supply the bulk of synthesis and finished-dose manufacturing. This supply-side concentration creates procurement leverage for large buyers but exposes mid-sized players to supply risk if quality or geopolitical pressures materialize. CDMOs that offer sterile capabilities and regulatory-compliant facilities (including recent investments in GMP capacity across Europe and Asia) are increasingly attractive partners for downstream players looking to reduce capital intensity.

Formulation innovation is a differentiator. While tablets remain the workhorse of metronidazole demand, topical and vaginal formulations—especially those with improved delivery or convenience—are the most defensible premium segments. Companies with brand equity in dermatology or women’s health can sustain higher margins by coupling clinical messaging with formulary evidence and local guideline adoption strategies.

Procurement and payer behavior will favor multi-attribute value. Hospitals and large group purchasers are moving beyond price‑only decisions toward multivariate procurement criteria (supply security, sterile manufacturing footprint, regulatory track record, and stewardship alignment). Vendors that can demonstrate continuity of supply and low regulatory friction will win share even at modest price premiums.

The market comprises legacy innovators, high-volume generic manufacturers, and specialist CDMOs. Prominent companies operate across the value chain as API providers, finished-dosage manufacturers, or brand marketers. For strategy teams, mapping competitors by capability (API scale vs. formulation expertise vs. regulatory footprint) is critical; competing on price alone is increasingly a race to the bottom. Instead, participants should evaluate combinations of vertical integration, contractual API security, and product differentiation.

API-centric manufacturers and suppliers remain strategic nodes for securing cost and continuity. Several established API producers in Asia and India continue to hold manufacturing scale and export capacity. Securing long-term API access or investing in co-located finishing capacity can materially de-risk supply chains and improve gross margins.

CDMOs with sterile and complex‑formulation capabilities are gatekeepers for hospital and specialty clinic demand. Outsourcing to qualified CDMOs accelerates time-to-market and mitigates capital outlay for companies seeking to launch differentiated gels, injectables, or other niche formats.

Branded marketers with channel access (dermatology, women’s health) can preserve premium pricing through clinical evidence and guideline inclusion, but must defend against rapid generic erosion once AB‑rated alternatives enter the market.

New generic approvals in 2024 for topical and vaginal formulations have immediate P&L implications. Entry of AB‑rated generics compresses price in those segments; however, it also expands aggregate demand in some channels through formulary substitution. Companies planning 2026 launches need accelerated cost optimization and rapid market access playbooks.

Label revisions and regulatory clarifications during 2024–2025 increase the premium on regulatory intelligence. Changes in injectable labeling, stewardship classifications, and public notices about legacy products necessitate ongoing monitoring and scenario testing in pricing models and hospital contracting.

M&A and partnership windows are open for scale and capability acquisition. Given market concentration and modest growth, strategic deals that add API scale, sterile injectable capacity, or niche branded portfolios can deliver differentiated returns compared with organic expansion alone.

Our full Metronidazole Market report is designed as a decision-support toolkit for 2026 planning cycles. Key deliverables include:

A calibrated market model (2020–2025 historical, 2026–2032 forecast) with scenario toggles for stewardship pressure, pricing shock, and regulatory outcomes.

Supplier and CDMO scorecards that evaluate capacity, regulatory compliance, geographic risk, and lead‑time reliability.

Competitive playbooks for each company archetype (API-specialist, CDMO, generic manufacturer, branded marketer) outlining go-to-market options and likely counters.

Price‑sensitivity and margin simulation tools to stress-test portfolio choices under rapid generic entry or procurement consolidation.

Regulatory risk matrix tied to commercial outcomes — including implications of global antimicrobial stewardship policies and recent label updates.

Target lists and diligence frameworks for M&A activity, with screening criteria aligned to synergy capture and integration risk.

Lock down API continuity. Negotiate multi‑year supply contracts with key API suppliers or secure CDMO slot reservations to prevent production bottlenecks that can erode share during tender cycles.

Prioritize differentiated formulations. Redirect R&D and commercial investment toward topical, vaginal, or sterile formulations that can justify premium pricing and enjoy slower generic substitution.

Build regulatory surveillance into forecasting. Convert regulatory intelligence (label changes, stewardship classifications, approvals) into scenario inputs so budget teams can stress-test revenue and procurement commitments.

Design M&A playbooks around capability gaps. Acquire or partner for sterile injectable capacity and regulatory-hardened manufacturing to access hospital tender opportunities.

Reframe commercial arguments to purchasers. Emphasize supply security, stewardship alignment, and total cost of ownership rather than low upfront price where applicable.

This preview demonstrates strategic line-of-sight without disclosing the granular regional, product-type, or application split tables that drive tactical procurement and launch decisions. PW Consulting’s full report contains the detailed segmentation, unit‑price simulations, supplier contracts mapping, and candidate M&A targets you will need to operationalize the high-level moves described here. Those tables and the interactive forecasting workbook are intentionally gated to ensure clients receive accurate, up‑to‑date modeling tied to our primary-source verification and commercially sensitive datasets.

For 2026 planning, lead teams should begin by running the report’s scenario model on their core products and supply portfolios, then prioritize immediate actions on API contracts and formulation pipelines. PW Consulting can provide an executive briefing and customized model run that maps the firm’s specific exposure and opportunity set into a prioritized roadmap for 2026. To access the full Metronidazole Market study, supplier scorecards, and the interactive forecast workbook, please follow the link on our publications page or contact your PW Consulting account lead.

For detailed analysis of this topic, please visit the official page:Metronidazole Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com