The Ultimate Guide to 1/36 Scale Diecast Cars and 1/38 Scale Diecast Cars

Other |

2026-06-18 18:21:44

As public- and private-sector capital rebalances toward resilient, low-carbon infrastructure, concrete fibers are moving from niche specification items to central elements of structural design, constructability strategy, and lifecycle cost management. PW Consulting’s Concrete Fiber Market study (base year 2025; historical window 2020–2025; forecast period 2026–2032) synthesizes this structural shift into an actionable intelligence package for leaders planning through 2026 and beyond.

Concrete Fiber Market

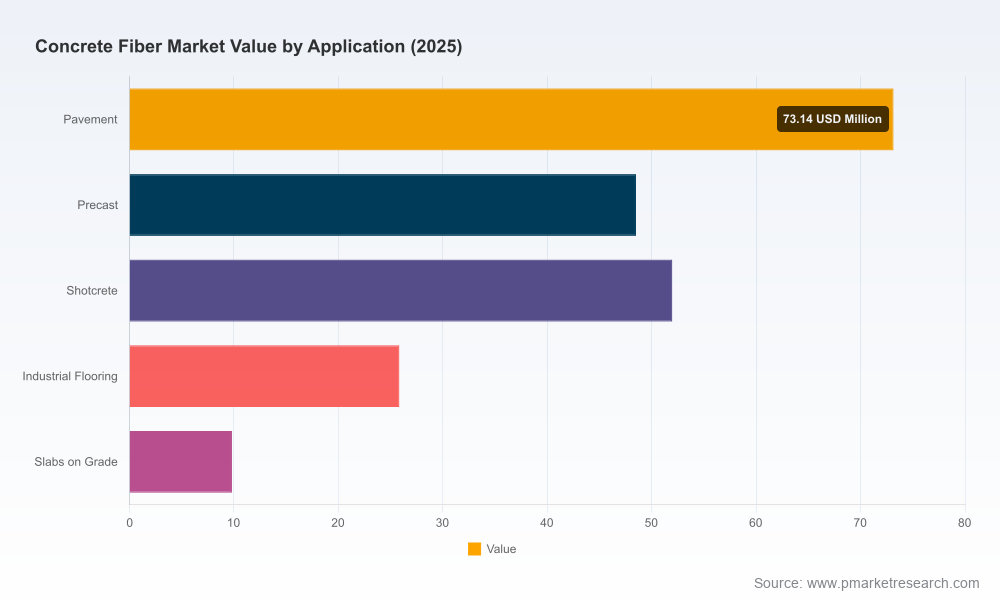

At the macro level, the market tracked by the study grows from a mid‑hundreds million USD base in the early 2020s to a projected market substantially larger by 2032, underpinned by a compound annual growth rate of 8.98% across the forecast window. Our market-concentration analysis shows a moderately fragmented supplier base (CR3 ~28.4%, CR5 ~35.7%), which creates both opportunity and risk for incumbent suppliers and new entrants: scale matters, but technical differentiation and go‑to‑market execution can still move share quickly.

Concrete Fiber Market

Capital deployment: Infrastructure stimulus and private industrial expansion in major markets are renewing demand for durable, fast‑constructing concrete systems. Fiber reinforcement is being specified to reduce labor, speed topping installations, and limit dependency on welded wire mesh and secondary steel placement.

Concrete Fiber Market

Sustainability & procurement: Environmental Product Declarations (EPDs) and life‑cycle thinking are now procurement table stakes for large owners and contractors. Leading suppliers have already published product-specific EPDs and are leveraging these into spec wins; the pace of EPD adoption will materially affect product selection and commercial differentiation in 2026 procurement cycles.

Standards & acceptance: ASTM compliance and product‑level certifications increasingly determine whether fibers are accepted for shrinkage control, temperature reinforcement, or primary structural roles. This drives demand for datasheets, test evidence, and spec language that translates into enforceable procurement clauses.

Constructability & labor pressures: Owners and general contractors facing skilled labor shortages are prioritizing solutions that reduce on-site labor intensity and schedule risk — a core selling point for macro synthetic fibers and engineered fiber systems when paired with clear dosing and placement protocols.

This study is designed to be operational from day one. It combines a transparent demand model, scenario-driven forecasting, and tactical toolkits that translate market insight into executable actions:

Demand model and scenarios — bottom‑up market-sizing for 2026–2032 with alternative scenarios reflecting higher adoption, accelerated standards harmonization, and slower-than-expected specification uptake.

Procurement and specification playbooks — sample spec language, acceptance test protocols, and contract clauses that reduce ambiguity between owners, designers, and contractors.

Commercial due diligence templates — vendor scorecards, margin and pricing benchmarks, and a checklist for technical audits and factory capability assessments.

Go‑to‑market materials — buyer personas for specifiers, designers, and contractors; value‑pricing frameworks; and sales playbooks aligned to project lifecycle timing.

Implementation toolkits — dosage calculators, constructability checklists, training curriculum outlines, and pilot project design templates to accelerate field validation.

Risk and monitoring dashboard — KPIs to monitor adoption velocity, quality issues, raw material volatility, and regulatory developments that could alter competitive dynamics.

The competitive map combines global firms with broad formulation and channel reach and smaller, innovation‑focused manufacturers targeting niche applications. Key strategic signals identified in the study:

Sika AG — Sika’s integrated approach (product portfolio, dosage software, and EPD publication) demonstrates how technical content and customer‑facing tools can generate specification momentum. Their second edition of the SikaFiber® handbook and product‑level EPDs exemplify a solutions‑led strategy that removes adoption friction for large specifiers.

The Euclid Chemical Company — Euclid is leveraging project wins and trade presence to bulk up adoption into heavy industrial and commercial slabs. Their project supply activities and regional EPD efforts indicate a playbook focused on credibility and locality — critical when owners demand regional carbon accounting.

Chryso Inc. — The Adfil® Strux rebrand and new sustainable-series launches show how product refreshes tied to sustainability narratives can reset buyer perceptions and create new specification opportunities in architectural and tilt‑up panels where constructability matters.

MAPEI, FORTA, Pioneer (PIONEER® Fibre), Nycon, ABC Polymer and Kratos — each pursues differentiated routes to market: twisted fiber geometries for reduced steel dependence, 3D reinforcement networks for precast, polypropylene offerings for pervious/pavements, and CE/ASTM certifications for infrastructure projects. Collectively they illustrate a market where product form factor, certification status, and channel relationships matter more than raw scale alone.

Strategic implication: with a CR3 well under 30%, the market is open to competitive moves through service bundling, certification investments, and spec‑centric sales motions rather than pure price competition.

Manufacturers: Prioritize EPD completion across key SKUs, invest in clear ASTM/CE documentation, and develop dosage/acceptance tools that embed into specifier workflows. Consider channel partnerships with admixture and precast suppliers to create bundled solutions that reduce friction for adoption.

Contractors & specifiers: Pilot fiber‑first designs on low‑risk projects to build organizational competence; insist on supplier data packages including EPDs and ASTM compliance; and negotiate warranty/acceptance metrics linked to measurable on‑site test outcomes (e.g., crack width, flexural performance).

Investors & M&A: Seek targets with differentiated IP (fiber geometry, polymer chemistry), strong channel access into precast or industrial flooring, and documented EPDs that reduce go‑to‑market cost. Fragmentation creates multiple bolt‑on opportunities to consolidate capabilities and gain scale.

Standards bodies & policymakers: Accelerate alignment between environmental accounting and functional performance metrics to avoid unintended substitution away from fibers that provide lifecycle carbon benefits through reduced steel use and improved durability.

Key risks that should appear on every 2026 board agenda:

Regulatory shift risk — changes in procurement rules or life‑cycle accounting that alter the relative attractiveness of synthetic versus mineral fibers.

Adoption risk — slow uptake in conservative specification environments where engineers are unwilling to substitute long‑standing reinforcement practices without local performance evidence.

Quality and compliance risk — inconsistent factory QA or gaps in certification that lead to field performance failures and reputational damage.

Supply chain risk — feedstock price volatility and regional logistics constraints that affect availability and margins, particularly for extrusion‑based synthetic fibers.

Suggested KPIs to operationalize monitoring: acceptance rate of fiber specifications on bid packages, average time from specification to first project use, warranty/field failure incidents per 1,000 m2, EPD-linked procurement wins, and rolling three‑month raw material cost variance.

The full report contains the granular inputs and tools required to act with confidence in 2026: detailed regional and application forecasts, vendor scorecards, price and margin models, project pipeline analytics, and downloadable procurement/specification templates. PW Consulting’s forecast model (2026–2032) is provided with scenario toggles so commercial teams can stress‑test assumptions against faster or slower adoption curves.

We intentionally present a high‑signal strategic narrative here while reserving the granular segment-level economics and vendor-level revenue detail for the full study. If your 2026 planning requires executable tactics — from pilot design to procurement clause language, or from M&A screening to channel build-out plans — the full dataset and toolkits in the PW Consulting report will reduce execution risk and accelerate time to impact.

For teams making capex, specification, or M&A choices in 2026, the core takeaway is straightforward: the market is expanding at nearly a 9% CAGR through the next decade; competitive advantage will accrue to organizations that pair certified, EPD‑backed product portfolios with field‑ready implementation tools and a spec‑driven commercial motion. Those who move early to close the gap between laboratory evidence and on‑site acceptance will capture the highest‑value opportunities as the market rebalances toward durability, constructability, and carbon accountability.

Contact PW Consulting to schedule a briefing that maps the report insights directly onto your product portfolio, procurement cycle, or deal pipeline. Our client workshops convert these strategic imperatives into 90‑day implementation plans tailored to your organization’s scale and market role.

For detailed analysis of this topic, please visit the official page:Concrete Fiber Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com