Lyocell Fiber Market — Strategic Preview for 2026 Decision-Making

As PW Consulting’s Senior Strategic Advisor and Head of Industry Analysis, I present a focused preview of our full Lyocell Fiber Market study, designed to orient executive decisions through 2026 and beyond. This briefing synthesizes the high-level growth trajectory, competitive posture, supply-side dynamics and strategic implications you must factor into near-term capital allocation, sourcing and product strategy. We deliberately spotlight analytical depth to build confidence while withholding proprietary sub-segmentation detail — the full report provides the granular tables, scenario models and playbooks that operationalize these insights.

Lyocell Fiber Market

Market trajectory at a glance

The Lyocell fiber market has emerged as one of the fastest-growing specialty cellulosic segments in textiles and nonwovens. Using 2025 as the base year, our historical review (2020–2025) and forecast (2026–2032) show a robust expansion path driven by sustainability-led demand, new capacity and broadened end‑use penetration. Key macro datapoints from our study that frame the strategic agenda:

Lyocell Fiber Market

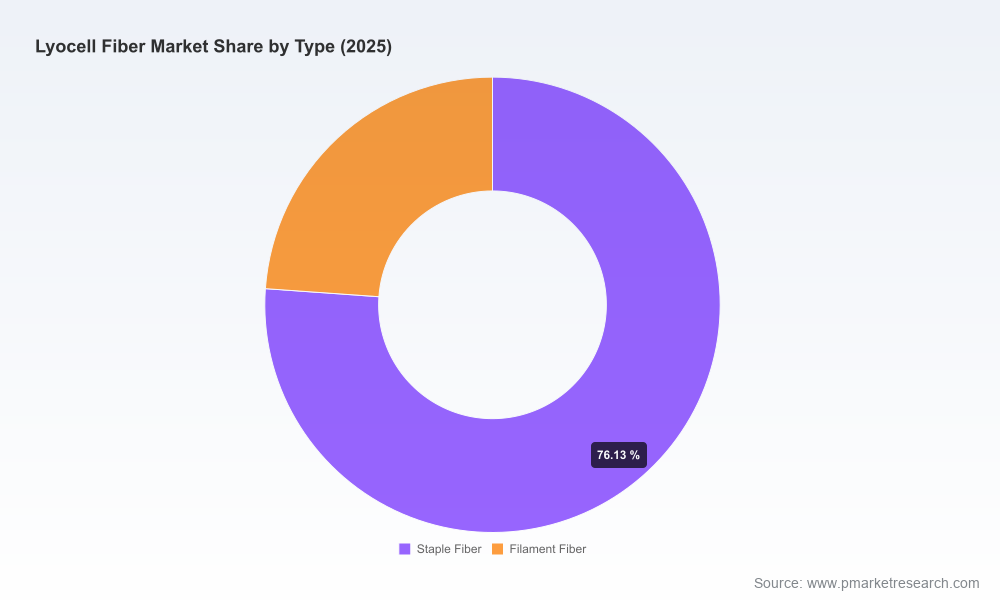

- Historical market size progressed from USD 980.0 Million in 2020 to USD 1,475.0 Million in 2025 (base year).

- Under our central scenario, the market reaches approximately USD 2,590.0 Million by 2032.

- The compound annual growth rate across the forecast window is 8.45% — a pace that materially exceeds many conventional fiber categories.

- Market concentration is notable: the top three players account for roughly 62% of market share, while the top five capture roughly 78%, indicating an oligopolistic structure that favors integrated and scale-capable producers.

These topline dynamics create a structural opportunity set for incumbents and new entrants alike — but they also embed tactical risks that must be stress-tested before committing capital or signing long-term purchase agreements.

Lyocell Fiber Market

Demand signals and where growth will be sourced

Three demand vectors are converging to accelerate Lyocell adoption:

- Sustainability premiuming by brands and conscious consumers (carbon, biodegradability, and circularity credentials).

- Performance extensions into sportswear, technical apparel and high-value nonwovens (hygiene, filtration, medical applications).

- Downstream conversion improvements and innovations that widen application breadth (blends, filament advances, and specialty finishes).

For decision-makers, the implication is clear: product strategies that combine demonstrable sustainability credentials with functional performance command a margin advantage. However, the path to capture this premium is operationally intensive — from validated supply chains to certifications and closed-loop process proofs.

Supply-side developments and strategic inflection points

The supply landscape is being reshaped meaningfully by capacity additions and technology differentiation. Several recent industry moves underscore evolving power dynamics:

- Lenzing AG has extended its nonwoven-grade footprint into Asia with VEOCEL™ production at Prachinburi, signaling a push to own growth in hygiene and filtration segments within proximity to large converters.

- Sateri’s commissioning of a new lyocell plant marks a substantial capacity escalation that changes regional sourcing economics and bargaining dynamics.

- Aditya Birla Group’s launch of a sustainable lyocell range (Livaeco Lyocell) demonstrates the strategic play of combining brand-led fiber offerings with performance orientation for sports and activewear.

- Specialty approaches, such as SMARTFIBER’s algae‑enriched SEACELL™ and Lenzing’s REFIBRA™ closed-loop initiatives, illustrate a bifurcation: scale-oriented commodity lyocell versus differentiated specialty solutions.

Collectively, these moves imply three critical supply-side inflection points for 2026 decisions: feedstock access and cost pass-through, regional proximity to converters and brands, and the ability to certify and trace sustainability claims end-to-end.

Competitive landscape — who matters and why

The market’s top-tier firms are not interchangeable. Each competitor brings a different strategic playbook you must model when assessing partnerships, co-development or capacity investments:

- Lenzing AG (Austria) — a technology and quality leader with vertically integrated offerings (TENCEL™, VEOCEL™) and strong sustainability storytelling (REFIBRA™, closed-loop production). Their moves set technical standards and often create tiered pricing benchmarks.

- Aditya Birla Group (India) — a high-volume branded supplier focused on performance apparel through Birla Cellulose and Livaeco. Their scale and brand relationships make them a primary partner for mass and premium textile converters targeting performance claims.

- Sateri (China) — an aggressive capacity builder serving textiles and hygiene markets. Recent plant expansions materially alter regional supply economics and create sourcing flexibility for Asian converters.

- SMARTFIBER AG (Germany) — exemplifies premium niche positioning, bringing bioactive and wellness-oriented lyocell variants to premium apparel and lifestyle categories.

- Baoding Swan Fiber Co., Ltd. (China) — an early domestic producer with a focus on staple fibers and industrial applications, relevant for regional sourcing strategies.

Understanding not just who the suppliers are but what proposition each offers (scale, sustainability, specialty, regional footprint) is a prerequisite to structuring robust supplier agreements and aligning product roadmaps.

Risk matrix — what could derail expected growth

Growth is not guaranteed. Our report models headwinds that materially change the growth curve and provides mitigants for each:

- Feedstock volatility: pulp availability and price swings can compress margins unless hedged or offset by integration.

- Policy and certification risk: evolving regulatory expectations around biodegradability and recycling require proactive certification strategies.

- Overcapacity in pockets: localized capacity surges can depress regional pricing and create short-term oversupply.

- Technology risk: failure to commercialize performance or recycling technologies can relegate products to lower-value segments.

Our scenario modules quantify the impact of each risk on revenue and margin levers and outline concrete contingency measures — from financial hedges to flexible procurement clauses and technology co-investment frameworks.

What the full PW Consulting report delivers (practical contents)

Our comprehensive study is purpose-built for executives and product leaders who must make capital, sourcing and portfolio decisions in 2026. Deliverables include:

- Validated market sizing and bottom‑up forecasts (historical 2020–2025; forecast 2026–2032) with sensitivity bands tied to key demand and supply assumptions.

- Consolidated supplier scorecards and technology audits that rank players by capacity, sustainability credentials, cost position and innovation roadmap.

- Go‑to‑market playbooks for brands and converters: product positioning, price premium capture strategies and launch sequencing for performance and nonwoven applications.

- Investment models for new capacity and conversion projects, including payback profiles, unit economics, and break‑even pulp pricing scenarios.

- M&A and partnership watchlist with practical valuation ranges and integration risk checklists (confidential appendices contain target-level analytics).

- Operational levers: sourcing architectures, contract templates for long-term supply, and a certification/traceability implementation pathway.

- Primary market interview insights and a data appendix with time‑series pricing, utilization rates and technical performance metrics (available in the full report).

These components are engineered to convert insight into executable 12–36 month plans rather than high-level theory.

Immediate strategic actions for 2026

Based on our analysis, here are prioritized actions executives should adopt in the coming 12 months:

- Reassess supply portfolios: model dual‑sourcing with at least one vertically integrated partner and one specialty supplier to balance price stability and product differentiation.

- Negotiate long-term offtake or index-linked contracts that include clauses for capacity ramp timings and quality/traceability milestones.

- Accelerate product roadmaps that exploit lyocell’s sustainability-perf nexus (e.g., performance blends, nonwoven hygiene premium lines).

- Allocate R&D funds to validate closed-loop recycling or pulp substitution pilots — these are now table stakes for brand claims and margin protection.

- Embed scenario-based stress tests into capital approval processes to ensure new projects remain viable under pulp and price downturns.

- Monitor regional capacity additions and their commissioning timelines to optimize plant footprints and inventory strategies.

Why PW Consulting — and next steps

Our Lyocell Fiber Market study is not a static forecast; it is an operational toolkit. We combine proprietary market-sizing methods, primary supplier interviews, and scenario-driven finance models to convert market intelligence into board-ready recommendations. If your 2026 planning cycle includes sourcing renewals, capacity decisions, product launches or M&A, this report will materially shorten decision time and reduce execution risk.

For the full segmented analysis, confidential company exhibits, and the implementation playbooks referenced above, please access the full report on our website or contact your PW Consulting engagement lead. The preview you have read demonstrates the study’s rigor; the complete report contains the underlying segment-level data and executable annexes needed to act decisively in 2026.

For detailed analysis of this topic, please visit the official page:Lyocell Fiber Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com