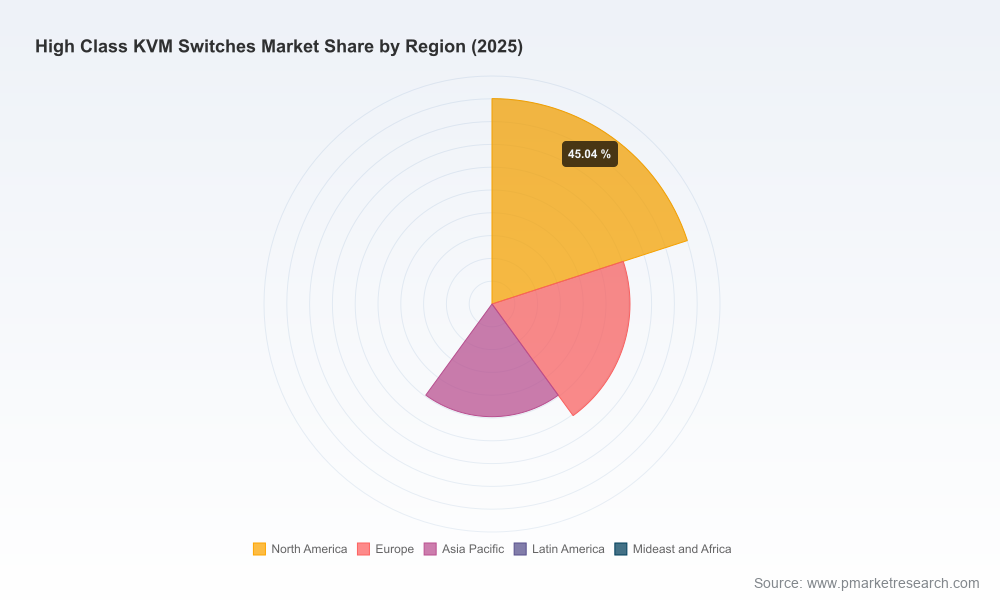

High Class KVM Switches Market — Strategic Preview for 2026 Decision-Makers

As enterprise architectures decentralize and remote operations become the default for mission-critical control rooms, broadcast centers, and hyperscale data centers, the High Class KVM (keyboard-video-mouse) switches market has entered a new phase of strategic importance. This preview synthesizes PW Consulting’s latest market research (base year: 2025; historical window: 2020–2025; forecast: 2026–2032) to highlight the decision levers that will matter most in 2026. It is written for CIOs, infrastructure procurement leads, security architects, and corporate strategy teams seeking an evidence-based lens without prematurely divulging the granular segmentation that drives procurement- and M&A-level choices.

High Class KVM Switches Market

Market snapshot: scale, growth and concentration

The market for high-end KVM switches has expanded materially over the past half-decade, rising from a global industry value in 2020 to a substantially larger base by 2025. Our base-year sizing is stated in USD (Million), with the research projecting continued expansion across the 2026–2032 forecast window. The sector is expected to grow at a compound annual growth rate (CAGR) of roughly 7.8% through the forecast period, reflecting structural demand for secure remote access, higher-resolution video handling, and low-latency extension technologies. Competitive concentration in the segment is moderate: the top three vendors account for under one-quarter of the market, and the top five account for slightly more — a dynamic that sustains opportunities for specialized vendors and new entrants with differentiated IP or regulatory-compliant capabilities.

High Class KVM Switches Market

Why this matters for 2026 strategic planning

- Security-first procurement: Regulatory migration toward modern cryptographic standards and validated modules is non-negotiable. Organizations planning procurement or refresh cycles in 2026 must assume that older FIPS 140-2-only solutions will increasingly be deprecated from certification lists, and that validated FIPS 140-3 cryptographic modules will be a requirement in government and regulated-industry deployments.

- Operational continuity under decentralization: With hybrid work and distributed control-room architectures becoming standard, enterprises must prioritize KVM solutions that support remote operation without compromising latency or video fidelity. Decisions taken in 2026 will determine whether an organization can cost-effectively scale remote access while preserving operator ergonomics and situational awareness.

- Total cost of ownership (TCO) and energy impact: KVM platforms are now being evaluated not just on acquisition price but on lifecycle power consumption, cooling footprint, and management centralization. Given the material electricity consumption of modern data centers — and projections of significant growth driven by AI workloads — energy-efficient and centrally manageable KVM solutions produce outsized operational savings over typical refresh cycles.

- Supplier risk and consolidation planning: Fragmented market share combined with rising technical certification thresholds means enterprises should harden supplier due diligence in 2026. Vendor roadmaps for cryptography standards, JPEG XS or alternative codecs, and long-term firmware support are now procurement blockers.

Technology and product themes shaping vendor strategy

- From analog to IP and beyond: The product narrative is clear: high-resolution KVM-over-IP and low-latency extender technologies dominate roadmaps. Expect continued innovation around 4K/8K support, multi-monitor configurations, and ultra-low-latency codecs tailored for live broadcast and control-room environments.

- Codec and transport evolution: Lightweight, visually lossless codecs (e.g., JPEG XS family adaptations) are moving from demonstration to deployment in environments where perceived pixel fidelity and real-time responsiveness are essential.

- Security as a platform feature: Vendors that combine FIPS 140-3 validated cryptographic modules, NIAP-aligned secure KVM options, and hardened tamper-resistant architectures will capture premium segments in regulated industries and national security procurement.

- Management and orchestration: Centralized control planes — supporting role-based access, session logging, firmware governance, and software-defined switching — are emerging as decisive procurement filters for organizations consolidating operations across multiple sites and edge deployments.

Competitive landscape — positioning and recent strategic moves

Our competitive analysis focuses on a set of established and specialist vendors driving product innovation and certification-led differentiation. Below is a thematic synthesis of their strategic positioning (detailed vendor scorecards and benchmarking are available in the full report):

High Class KVM Switches Market

- Vertiv Group Corp. (Columbus, OH) — A systems player extending into secure KVM-over-IP with platforms that target enterprise and edge data centers. Vertiv’s recent launch of a second-generation KVM-over-IP platform with FIPS 140-3 cryptography signals a play to capture regulated enterprise spend where validated security is a procurement prerequisite.

- Raritan (Legrand, Somerset, NJ) — Focused on ultra-high-performance KVM-over-IP for large enterprise matrices, emphasizing scalability, 4K support, and resilient, fanless designs for sensitive environments. Their heritage in data-center management positions them well in integrated infrastructure bids.

- IHSE GmbH (Germany) — A leader in KVM extenders and low-latency systems for broadcast and control rooms; recent product generations emphasize next-gen codecs and 4K/8K capabilities. Their early adoption of JPEG XS-class workflows is likely to resonate with broadcast and visualization use cases where latency and fidelity are non-negotiable.

- Adder Technology (UK) — Strong in mission-critical, low-latency IP KVM and extenders for control-room and broadcast markets. Adder’s positioning is built on consistent performance in high-availability environments and partnerships with systems integrators.

- ATEN International (Taipei) — A diversified manufacturer that blends desktop and enterprise KVM offerings; product design recognition and multi-monitor innovations make ATEN a choice for professional users with ergonomic demands and cross-domain deployments.

- Shenzhen CKL Technology — Represents a class of specialist, high-density multi-monitor KVM vendors focusing on large personal-desktop consolidation scenarios; their engineering focus addresses multi-workstation workflows common in financial trading floors and professional studios.

Recent product launches, design awards, and certifications among these vendors underscore two critical market tendencies: (1) security and certification are becoming decisive differentiators, and (2) low-latency, high-resolution video handling is shifting purchase decisions from commodity switches to purpose-built, higher-margin platforms.

Practical contents of the full PW Consulting report (what you will find behind the paywall)

- Proven market sizing methodology with historical reconciliations and an integrated forecasting engine (currency: USD, revenue unit: Million) — validated against vendor revenue disclosures and channel checks.

- Actionable procurement frameworks: RFP templates, vendor evaluation scorecards, certification checklists (FIPS 140-3, NIAP PP PSD), and end‑to‑end TCO models that incorporate energy and management overheads.

- Vendor benchmarking matrix covering product architecture, security posture, codec support, latency performance, management features, and roadmap risk assessments.

- Strategic playbooks for IT and OT convergence: migration sequencing, hybrid edge-office deployments, and best-practice integration with orchestration layers.

- Scenario-based investment cases and stress-tested demand models for 2026 supply-chain volatility and regulatory acceleration.

- M&A and partnership screening heuristics for corporate development teams looking to consolidate capabilities or access regional channels.

- Case studies and implementation blueprints from enterprise and broadcast customers highlighting real-world trade-offs and measured performance outcomes.

How to use this intelligence in 2026

- Short-list by capability, not brand: Use security validation, codec/lossless compression performance, and centralized management as the first filters. Brand reputation matters, but technical fit and certification timelines are the tie-breakers.

- Procurement timing: If your refresh cycle falls in 2026, prioritize vendors with demonstrable FIPS 140-3 pathways and long-term firmware support commitments. Legacy-only vendors present contract and compliance risk.

- Energy-aware procurement: Quantify the incremental power and cooling implications of KVM consolidation strategies. For large server farms and command centers, small efficiency differentials compound quickly across hundreds of deployed units.

- Contracting and lifecycle clauses: Insist on security-update SLAs, cryptographic module migration guarantees, and transparent EOL roadmaps. These clauses mitigate the cost of forced mid-cycle upgrades when standards evolve.

Regulatory and operational risk factors to track

- Migration timelines for cryptographic validations (FIPS 140-3 adoption) and any procurement rules that reference NIAP secure KVM profiles.

- Data-center energy constraints and the potential for jurisdictional regulations tied to energy usage or sustainability targets.

- Supply-chain concentration for critical semiconductor or optical components used in low-latency extenders and codecs.

- Vendor certification and quality management adherence (e.g., ISO 9001), which materially affect deployment risk in regulated industries.

Final note — why read the full PW Consulting study

This preview lays out the strategic contours that will shape KVM decisions in 2026: a growing market backdrop, a rising bar for security and performance, and an opportunity window for organizations that align procurement, operations, and compliance before certification cliffs truncate vendor eligibility. The full PW Consulting report contains the granular breakouts, supplier scorecards, actionable templates, and pricing benchmarks required to operationalize these insights — intentionally withheld here to preserve the report’s role as the definitive decision-support asset.

For procurement teams preparing RFPs, security architects mapping certification paths, or corporate development groups screening targets, the report converts ambiguity into executable choices. Access the complete study for the full segmentation, vendor matrix, scenario models, and implementation playbooks that will inform boarding and budget decisions in 2026.

For detailed analysis of this topic, please visit the official page:High Class KVM Switches Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com