Global Hot-Dip Galvanized Steel Market Growing at 2.5% CAGR Through 2032

Other |

2026-07-01 11:37:31

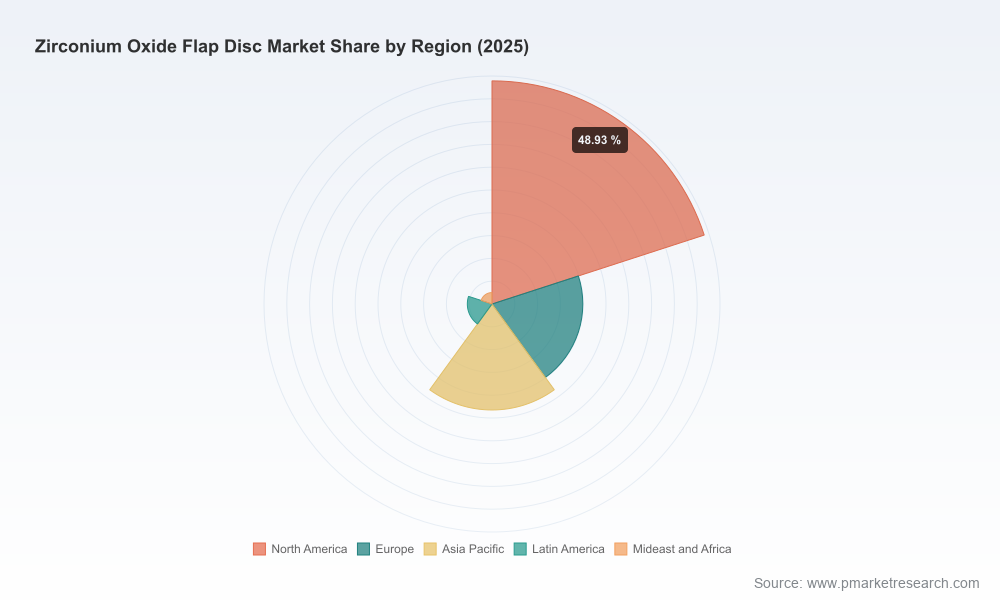

As manufacturing and metal‑working value chains re‑orient toward efficiency and surface quality, zirconium oxide flap discs have moved from a niche consumable to a strategic input for a wide range of industrial users. Our PW Consulting base‑year assessment (2025) places the global market at approximately USD 191 million, having expanded steadily from 2020. Looking ahead to our 2026–2032 forecast horizon, the market is expected to grow at a compound annual growth rate (CAGR) of roughly 3.5%, reaching an estimated market scale in the mid‑hundreds of millions by 2032. Market concentration remains relatively low: the top three suppliers account for roughly a quarter of industry sales, and the top five capture about 30% — an important feature for procurement and competitive strategies.

Zirconium Oxide Flap Disc Market

Between 2020 and 2025 the market exhibited steady expansion driven by metal fabrication activity, construction cycles, and continued replacement demand from heavy industry. The expected 3.5% CAGR to 2032 reflects a combination of steady industrial demand, selective premiumization, and incremental gains from newer end‑use applications where higher removal rates and disc longevity deliver clear unit‑cost advantages.

Zirconium Oxide Flap Disc Market

Key demand drivers covered in the full study include: sustained repair & maintenance activity in heavy industries; demand for improved finish and cycle‑time reduction in manufacturing; and end‑user shifts toward longer‑life abrasives to lower downtime and labour costs. Offsetting these are pressures from substitution (alternate abrasive systems for some applications), automation that alters abrasion patterns, and cyclical end‑market exposure.

Zirconium Oxide Flap Disc Market

On the supply side, several structural themes influence supplier economics and product performance. Zirconium oxide (zirconia) feedstock dynamics remained broadly stable through early 2025 with slight upward pressure in some quarters. Regional supply tightness — notably in supplying countries with rising aerospace and nuclear demand — has driven localized price pressure and prompted some suppliers to re‑think inventory and sourcing strategies. These developments are material to 2026 procurement decisions: small percentage movements in zirconia pricing can compress gross margins unless offset through formulation, yield improvements or targeted price actions.

Regulatory compliance is another anchoring factor. Zirconia flap discs sold into developed markets are routinely designed to meet EN 13743 (European abrasive product safety) and referenced against ANSI B7.1 / OSHA 1910 safety requirements in the United States. Compliance, certification and customer audit readiness carry non‑trivial cost and speed‑to‑market implications that we quantify in the report.

The market’s moderate concentration and technical differentiation favor firms that combine product R&D with channel reach and quality assurance. Below is a high‑level synthesis of how leading firms are positioning themselves (full company scorecards and comparative matrices are included in the paid study).

Across these incumbents, competitive differentiation rests on grain chemistry (zirconia blends), bond systems, flap architecture, and after‑sales support such as safety documentation, training and tool‑matching advice. Our competitive heat map evaluates these dimensions and identifies where an entrant can realistically displace incumbent share versus where co‑opetition or channel partnerships are the efficient route.

The published study is designed as an executable toolkit for decision makers in 2026. Highlights include:

To preserve the integrity of our commercial insights and to encourage targeted engagement, detailed segmentation by region, application and type is available in the full report and in our interactive dashboards. This preview intentionally omits those granular splits.

This preview frames the strategic choices facing procurement, product and corporate development leaders in 2026. For teams that need to convert insight into action, PW Consulting offers the complete dataset, interactive models and tailored advisory: live supplier benchmarking, bespoke scenario runs using your demand profile, and a tactical 90‑day implementation plan that converts the recommendations above into measurable savings and revenue outcomes.

Access to the full report unlocks the granular regional, application and product‑type splits, supplier scorecards and the raw Excel models that are indispensable for contract negotiations, product roadmap prioritization and M&A due diligence. For a guided walkthrough and a customized executive briefing, contact our advisory desk to schedule a strategic session.

For detailed analysis of this topic, please visit the official page:Zirconium Oxide Flap Disc Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com