Where to Get a Saxenda Injection in Dubai: Legal Requirements

Health |

2026-04-27 08:04:28

Between 2020 and 2025 the global pyrometers market demonstrated steady expansion, moving from roughly USD 1,350 million to about USD 1,735 million (base year 2025). Our forward-looking model, calibrated to market signals and primary vendor intelligence, projects continued expansion through the 2026–2032 forecast window at a compound annual growth rate of 5.16%, with the market approaching the low‑to‑mid USD 2,400 million range by the end of the horizon. For corporate leaders making investment, procurement, or M&A decisions in 2026, this trajectory combines predictable growth with pockets of technology-driven disruption — creating both near-term optimization opportunities and mid-term strategic bets.

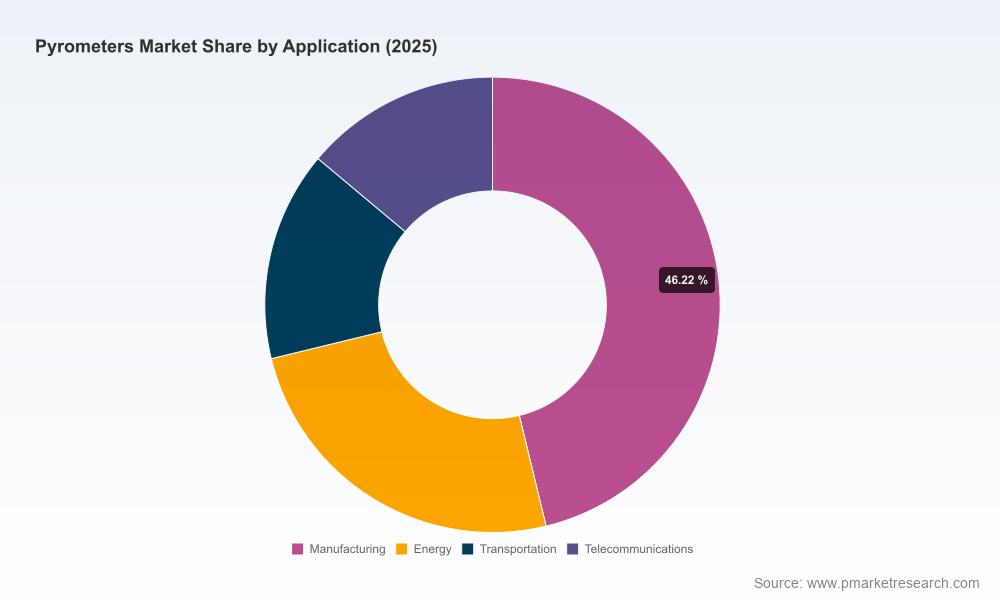

Pyrometers Market

The pyrometers market is being shaped by three concurrent forces. First, industrial digitization — integration with IIoT, MES/SCADA, and enterprise analytics — is converting point temperature measurement from a quality-control instrument into an input for closed-loop automation and digital twin models. Second, regulatory and aerospace quality standards have tightened: the adoption of updated standards such as SAE AMS 2750H and the rollout of associated training (e.g., Pyrometry II courses) are raising the bar for calibration practices, traceability, and supplier qualification. Third, component- and raw-material price volatility (notably for thermocouple alloys and optical-electronic components) is injecting cost uncertainty into manufacturing economics and vendor pricing models.

Pyrometers Market

These dynamics are amplified by the product economics of optical pyrometers, which command premium pricing relative to thermocouple assemblies — a multiple that drives careful trade-offs between accuracy, speed, integration complexity, and total cost of ownership.

Pyrometers Market

The competitive field is moderately concentrated: the top three vendors account for a meaningful share of the market, and the top five capture a majority position. This structure produces a mix of global scale players and highly specialized regional innovators. Key vendor archetypes to consider when building or benchmarking a supply base include:

Representative companies across these archetypes include long-established names with specialized portfolios — from manufacturers of non-contact pyrometers for metal processing to providers of shortwave thermal imaging and compact Ethernet-enabled devices. Recent product activity highlights this diversity: new fiber-optic pyrometer devices, expanded SWIR imaging offerings, and intensified trade‑show activity focused on metal‑temperature technologies. These moves indicate a vendor focus on technology differentiation and end‑to‑end solution selling.

To move from insight to action, the report delivers a suite of tools designed for operational and strategic teams. Key inclusions are:

These deliverables are grounded in primary interviews with device manufacturers, integrators, end-users, and calibration houses, complemented by a validated bottom-up revenue model and sensitivity analyses for key drivers.

Primary risks include regulatory shifts that raise compliance costs, raw-material price spikes, supplier consolidation activity that can tighten OEM leverage, and cybersecurity vulnerabilities as pyrometers become networked. To maintain situational awareness, track a compact dashboard of KPIs:

Executives should use the findings to prioritize initiatives that reduce measurement uncertainty, stabilize input costs, and accelerate integration of thermal sensing into digital operations. Begin with a focused instrument audit and a vendor re‑qualification process that tests suppliers on spectral capability, field calibration services, and secure networking architecture. Use the TCO templates in the report to quantify the payback of imaging and fiber‑optic investments versus incremental gains in yield, throughput, and reduced rework.

This briefing is designed as a strategic “preview” that demonstrates the analytical depth and operational utility of PW Consulting’s full Pyrometers Market research. The complete report contains region‑ and application‑level datasets, granular segment trajectories, vendor market shares, downloadable modeling files, and detailed vendor profiles — essential inputs for procurement tenders, M&A diligence, and product roadmap decisions. For teams intending to make decisive 2026 moves, accessing the full dataset will materially shorten the path from insight to execution.

Contact PW Consulting to obtain the full market dataset, supplier scorecards, TCO models, and scenario packages that underpin the recommendations above. Our advisory teams are prepared to run tailored workshops that convert the report’s outputs into a 90‑day implementation plan.

For detailed analysis of this topic, please visit the official page:Pyrometers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com