Thermoplastic Polyurethanes (TPU) Market — Strategic Outlook for 2026 Decisions

As PW Consulting’s lead industry analyst, I present a concise, decision-focused orientation to our full TPU market study (base year 2025). This briefing synthesizes the dynamics that will matter for capital allocation, commercial strategy, and risk management through the immediate planning horizon. It is designed to demonstrate the analytical depth of the study while preserving the segment-level intelligence available in the full report.

Thermoplastic Polyurethanes (TPU) Market

Market Trajectory: The Big Picture

The TPU market has demonstrated resilient expansion through the 2020–2025 historical window and enters the 2026–2032 forecast horizon on a steady growth trajectory. Our model uses 2025 as the base year (3560 Million USD) and shows compound annual growth of 7.21% across the forecast period. By 2026 the market rises above 3.8 billion USD and, under the central case, reaches approximately 5.79 billion USD by 2032. These aggregate figures are fundamental for sizing opportunities, stress-testing capex scenarios, and benchmarking revenue targets for downstream OEMs and compounders.

Thermoplastic Polyurethanes (TPU) Market

Why this matters for 2026 corporate planning

- Capex prioritization. A 7.21% CAGR across 2026–2032 means meaningful scale-up opportunities for players who secure feedstock and distribution advantages early. Investment decisions in 2026 must balance near-term volatility with multi-year demand drivers—particularly in engineered applications where higher-margin TPU grades are used.

- Portfolio steering and differentiation. Product differentiation (bio-based grades, biomass-balanced variants, specialty compounds for medical and high-performance footwear) will be the primary lever to sustain margins as commoditizing pressure increases in some low-end grades.

- M&A and consolidation calculus. Market concentration metrics show a moderately consolidated landscape, with the top three and five players capturing a majority of industry revenue. For corporates contemplating inorganic growth, this implies targeted bolt-ons or capability acquisitions (specialty films, service-intensive formulations, regional compounding) will often offer more accretive returns than broad-based greenfield expansion.

- Risk-adjusted commercial planning. Raw material swings, regulatory compliance costs, and trade policy are critical variables that should be incorporated into 2026 price and procurement strategies.

Key dynamics shaping 2026 strategic choices

- Feedstock volatility and margin compression risk. Asian 1,4-butanediol (1,4-BDO) spot levels — an important input for polyester TPU — experienced wide swings in 2024–2025. Our analysis shows that exposure to feedstock swings materially alters mid-cycle EBITDA by several percentage points for commodity-grade TPU producers. Hedging strategies, procurement partnerships with upstream polyol suppliers, and formula redesign for polyether or PCL blends are pragmatic responses.

- Regulatory compliance as an operational cost and barrier. Two policy shifts have immediate operational implications: OSHA’s proposed 5 ppb ceiling for MDI (October 2024) and the REACH amendment (August 2023) mandating certified training for handlers of formulations above defined thresholds. These both increase capex and operating expense — from closed-handling systems to per-worker certification costs. We estimate typical site-level compliance projects range from modest process upgrades to multi-million euro capital programs depending on scale and legacy infrastructure.

- Trade policy and regional sourcing re-optimization. Recent tariffs and trade measures — including U.S. duties on certain polyether polyol imports in 2025 — have altered landed cost dynamics and made nearshoring or diversification strategies economically compelling for North American players.

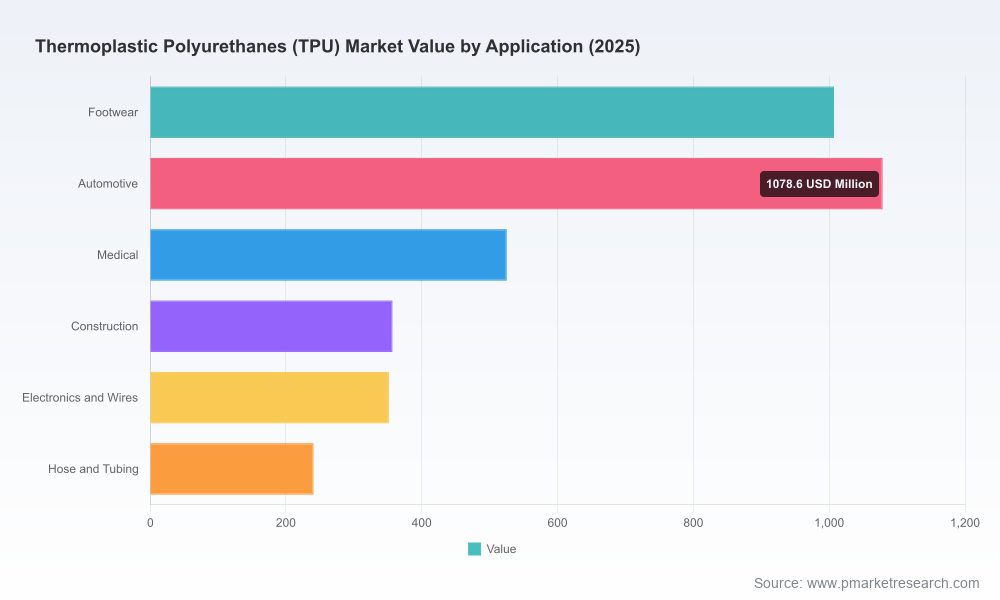

- Industrial investment and application pull. Adoption in automotive, advanced footwear, medical devices and electronics continues to drive demand for higher-value TPU grades. Application-specific performance requirements (abrasion, hydrolysis resistance, softness ranges) favor suppliers with R&D capabilities and application development centers near OEM clusters.

Competitive landscape — strategic implications

The TPU competitive set blends global chemical majors, regional champions, and specialty compounders. Ten firms analyzed in our study exemplify the range of strategic positions:

Thermoplastic Polyurethanes (TPU) Market

- BASF SE (Elastollan®) — Global reach with emphasis on engineered grades and bio-based variants; plays to scale and breadth of application portfolio.

- Covestro AG (Desmopan®, Platilon®) — Rapid capacity expansion and application development investments in China signal an aggressive market-share capture strategy in Asia; expect continued vertical integration plays and application-led commercialization.

- Huntsman Corporation (Avalon®) — Focused on footwear soles and engineered solutions; competitive where formulation flexibility and customer support matter.

- The Lubrizol Corporation (ESTANE®) — Specialty grades and biomass-balanced offerings target automotive and paint/PPF adjacencies; leverages formulation expertise to enter new use-cases.

- Wanhua Chemical Group — A China-based player with scale in footwear, cable and film segments; cost-competitive and increasingly active in export markets.

- Avient Corporation (NEUSoft™) — Compounder focus on healthcare and catheters underscores the value of regulatory know-how and medical-grade supply chains.

- American Polyfilm, Epaflex, COIM, Mitsui Chemicals — Regional and specialty players that excel in film, granules, coatings or localized engineering grades, forming acquisition targets or partners for larger players seeking capability fills.

Recent corporate moves illustrate the strategic playbook in action. Covestro commissioned a significant phase‑I capacity expansion in Zhuhai (Jan 2026) and opened an application development center in Guangzhou (May 2026) — a coordinated capacity + front-end application approach that reduces time-to-market for OEM-specific grades. Elsewhere, investments in site-level MDI controls and training have become non-negotiable; one large European producer invested in the mid-single-digit millions of euros to meet new exposure limits, an example of direct compliance-driven capital allocation.

What the full PW Consulting report delivers (practical, executable assets)

- Granular market modelling workbook (historical 2020–2025 and forecast 2026–2032) — assumptions transparent and stress-testable.

- Scenario analyses (base / downside / upside) with break-even demand and price paths for each scenario.

- Raw material sensitivity module — automated P&L impact from 1,4-BDO, polyol, and MDI inputs, including hedging playbooks.

- Regulatory impact matrix — quantified compliance cost estimates by region and recommended mitigation timelines.

- Competitive heatmaps and capability matrices — supplier positioning by technology, application expertise, and go-to-market coverage.

- Deal screening checklist and valuation sensitivities for M&A (including operational due diligence templates for capex and environmental liabilities).

- Commercial playbooks — pricing architecture recommendations, long-term offtake negotiation templates, and distributor vs. direct channel decision trees.

These deliverables are built to be immediately operational: investors can run due diligence with the provided templates; procurement teams can implement hedging and diversification plans; R&D and commercial leads can prioritize next-generation grade development according to quantified ROI thresholds.

Practical recommendations for 2026 action plans

- Protect margins through upstream engagement. Lock multi-year supply agreements or strategic JV arrangements with polyol and 1,4-BDO suppliers. Evaluate formulation substitution where technical fit permits.

- Prioritize compliance while preserving flexibility. Accelerate investments in closed-handling MDI systems where exposure is material; phase training programs to meet REACH and OSHA changes with minimal production disruption.

- Adopt a hybrid capacity strategy. Combine targeted brownfield expansions in high-demand corridors with contractual capacity via tolling or strategic partnerships to reduce lead-time and capital intensity.

- Invest in application-led sales. Co-locate application development resources near key OEM clusters (as exemplified by recent Covestro moves) to compress design wins and shorten conversion cycles.

- Be disciplined on M&A. Look for specialty assets with defensible IP, unique regulatory approvals, or entrenched customer relationships rather than scale-for-scale consolidation.

- Embed price-indexed contracts and pass-through mechanisms. Given raw-material volatility and tariff shifts, contracts that transparently link TPU selling prices to input indices reduce margin surprise and preserve customer relationships.

Closing perspective — what to expect and where to dig deeper

The aggregated market growth and concentration dynamics provide a clear signal: TPU demand will scale materially through the late 2020s, but value accrues to players who manage feedstock risk, regulatory cost, and application intimacy. Our study demonstrates that the next wave of differentiation will come from integrated moves — capacity where demand is growing, application support where design cycles matter, and compliance investments that make production sustainable and insurable.

To preserve the most actionable competitive intelligence for our clients, we have intentionally excluded the full regional, type and application-level split tables from this briefing. The complete report contains those segment-level models, supplier share matrices, and a downloadable financial model that enables bespoke scenario runs.

For executives drafting 2026 budgets and three-year strategic plans, the PW Consulting TPU study is structured to convert macro forecasts into executable moves — from procurement hedges to targeted capex and M&A screens. Access the full report to obtain the segmental datasets, supplier scorecards, and the Excel toolkit required to operationalize the recommendations summarized here.

For detailed analysis of this topic, please visit the official page:Thermoplastic Polyurethanes (TPU) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com