Load Cells Market 2026 Strategic Primer — PW Consulting

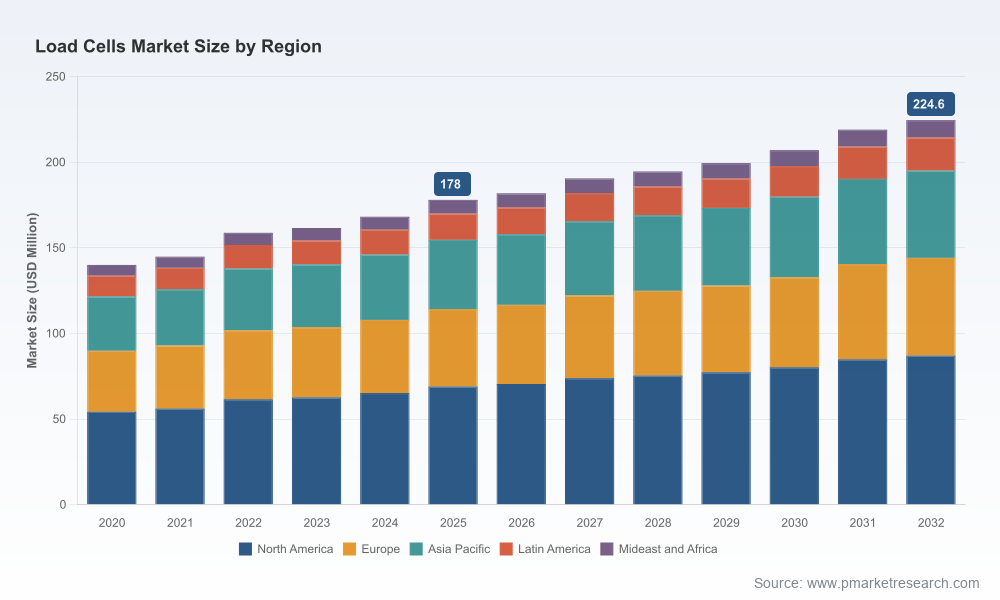

As organizations plan capital allocation and product roadmaps for 2026, the load cells market presents a measured but strategic growth opportunity. PW Consulting’s latest Load Cells Market study — anchored on a 2025 base year, drawing on historical 2020–2025 performance and providing a 2026–2032 forecast — synthesizes commercial, technical, and regulatory vectors that will determine winners and laggards across OEMs, integrators, and service providers. The market is projected to expand at a compound annual growth rate (CAGR) of 3.4% over the forecast window, moving from a 2025 industry size of approximately USD 178 Million to roughly USD 225 Million by 2032. This steady expansion, combined with a moderately fragmented supplier landscape (top‑3 firms represent about a quarter of the market; top‑5 roughly three‑tenths), creates distinct strategic inflection points for incumbents and entrants alike.

Load Cells Market

Market Snapshot: What the headline numbers hide

The headline CAGR masks differentiated dynamics across product types, capacity tiers, channels, and end-use verticals. While historical growth between 2020 and 2025 reflects resilience during supply-chain disruption and rising automation adoption, the 2026–2032 outlook is being driven by three structural themes: digitization of sensor outputs, the migration of weighing and force measurement into IoT and predictive-maintenance ecosystems, and regulatory/standards changes that raise technical barriers for some high‑precision applications.

Load Cells Market

- Size & trajectory: A compact market with predictable top‑line growth provides predictable revenue streams for manufacturing and calibration services, but limited scale for commodity players.

- Concentration: The industry’s low-to-moderate concentration ratio signals room for specialized vendors and regional champions to capture niche segments through product differentiation and service depth.

- Market premium: High‑precision and application‑specific load cells command margin premiums; digital and integrated solutions create an adjacent revenue pool (digitizers, telemetry, software integration, subscription services).

Why this research matters for 2026 corporate decisions

For 2026 planning cycles, the report serves three strategic functions:

Load Cells Market

- Investment triage — Prioritize R&D and capital spend by mapping profit pools across precision tiers, digital-enabled offerings, and aftermarket services.

- Commercial positioning — Decide whether to pursue OEM partnerships, direct system sales, or channel-centric distribution; each route has different margin and growth profiles.

- M&A and partnership screening — Identify capability gaps (e.g., digitizers, wireless telemetry, calibration networks) that can be filled faster via acquisition or alliance than organic development.

Key market dynamics shaping vendor strategy

- Digital integration and predictive maintenance: Wireless outputs and IoT integration are shifting value from the transducer to data services. Vendors who can bundle hardware with secure, standardized digital interfaces and analytics differentiate on total-cost-of-ownership.

- Standards and compliance: Revised international standards — including updates that impose biomechanical limits for human-robot collaboration — are driving design and validation changes in sensors used for collaborative robotics and safety-critical force measurement.

- Regulatory sensitivity for advanced components: Recent updates to dual-use controls in Europe have implications for suppliers of cryogenic or quantum‑adjacent components used in high‑precision sensor fabrication; compliance and export controls will influence supply‑chain choices for advanced manufacturers.

- Aftermarket and traceability: Routine calibration cycles, driven by quality systems like ISO 9001, create recurring revenue opportunities for vendors who can offer calibration-as-a-service, traceability records, and regional calibration networks.

- Geographic rebalancing and capacity expansion: Major suppliers are expanding capacity and targeting emerging markets with smart load cell solutions. Market entry strategies should account for local service expectations and regulatory regimes rather than relying on volume alone.

Competitive landscape — leaders, challengers, and strategic gaps

The sector is populated by a mix of precision specialists, systems integrators, and weighing-system incumbents. Several archetypes emerge from our competitive review:

- Precision engineering specialists: Firms focused on high‑accuracy and test‑and‑measurement applications emphasize laboratory-grade performance, traceable calibration, and specialized materials engineering. Their clients value repeatability and documentation over unit price.

- Systems and scale providers: Established weighing-system companies integrate load cells into scales and industrial weighing solutions, leveraging channel reach and installation services to lock in lifecycle revenues.

- Custom fabricators and niche innovators: Smaller firms and bespoke suppliers that serve nonstandard applications (biomedical, subsea, downhole) excel at tailored mechanical and environmental designs.

Representative market actors display complementary strengths. Some firms excel in custom and repair services for legacy assets; others lead in low‑profile stainless steel beams or wireless/digitized modules. Notable market activity in 2025–2026 includes new low-profile and onboard vehicle weighing beam load cell introductions, expanded single‑point ranges, and digitizer/transmitter launches that illustrate the shift to integrated, field-ready digital products. Additionally, a number of firms are broadening product families to capture aftermarket service and system-integration margins.

For strategists, the takeaway is clear: scale matters for distribution and contract wins, but specialization and digital capability are the primary margin drivers. The market’s fragmentation creates opportunities for roll-up strategies, bolt-on acquisitions, and channel consolidation focused on service proliferation and software-enabled differentiation.

What PW Consulting’s Load Cells Market report delivers

The study is designed as a practitioner’s toolkit for 2026: it integrates quantitative forecasting with executable go‑to‑market playbooks. Key deliverables include:

- Robust market sizing and trend decomposition (base year 2025, historical 2020–2025, forecast 2026–2032) with scenario-sensitive outputs built on a 3.4% forecast CAGR.

- Vendor scorecards and capability maps covering manufacturing footprint, product breadth, digital readiness, and service networks.

- Practical pricing and margin benchmarks for hardware and complementary offerings (digitizers, telemetry, calibration contracts), and recommended commercial levers to capture aftermarket value.

- Supply‑chain risk matrix and mitigation playbooks covering raw-material volatility, compliance with dual‑use controls, and strategies for decentralizing calibration capacity.

- Regulatory impact assessment covering recent standards changes and export-control developments, with compliance roadmaps for product teams.

- Candidate lists for M&A and partnerships prioritized by strategic fit, integration risk, and expected time-to-market for capability capture.

- Scenario planning tools — baseline growth, accelerated automation adoption, and constrained-trade/regulatory tightening — with implications for capacity planning and working-capital needs.

Actionable 2026 playbook — five priorities for leadership

- Accelerate digitization: Ship product families with integrated digitizers, secure telemetry, and documented APIs. Bundle these with maintenance/analytics subscriptions to lift lifetime value.

- Invest in calibration and service networks: Convert mandatory recalibration cycles into recurring revenue through regional labs, certified partners, and digital traceability platforms.

- Pursue focused M&A: Target niche precision suppliers, digital-amplifier manufacturers, and regional calibration shops to quickly buy capabilities and channel access rather than building from scratch.

- Rework commercial models: Shift from one‑time hardware sales to outcome- and uptime-based contracts for industrial automation and vehicle‑weighing customers, aligning incentives and creating stickier relationships.

- Embed compliance in product design: Update product roadmaps to reflect new ISO and export-control constraints early in the R&D cycle to avoid costly redesigns or market exclusions.

Closing — where to go next

For 2026 strategy cycles, the question is not whether the load cells market will grow — the forecast is clear — but how companies will capture disproportionate returns within a modestly sized, technically demanding industry. PW Consulting’s full report pairs the headline market trajectory and concentration metrics with the missing granular intelligence — regional and application splits, capacity-tier economics, and vendor-level revenue estimates — that executives need to set budgets, structure deals, and time product launches.

Use this primer to calibrate internal debates and to prioritize which segment-level datasets and vendor dossiers you need to unlock next. For the detailed datasets, segment breakouts, and vendor scorecards that operationalize the playbook above, please refer to the full Load Cells Market study available through PW Consulting.

For detailed analysis of this topic, please visit the official page:Load Cells Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com