2026 Strategic Preview: Navigating the Global Construction Market — A PW Consulting Introduction

As senior advisors at PW Consulting, we present an evidence-driven, decision-focused preview of our Construction Market study built around a 2025 base year and a 2026–2032 forecast window. This introduction distills the strategic implications executives must prioritize in 2026, while deliberately reserving the granular breakouts that power capital allocation, pricing strategies, and M&A choices for the full report.

Construction Market

Market at a glance: what the macro numbers tell you

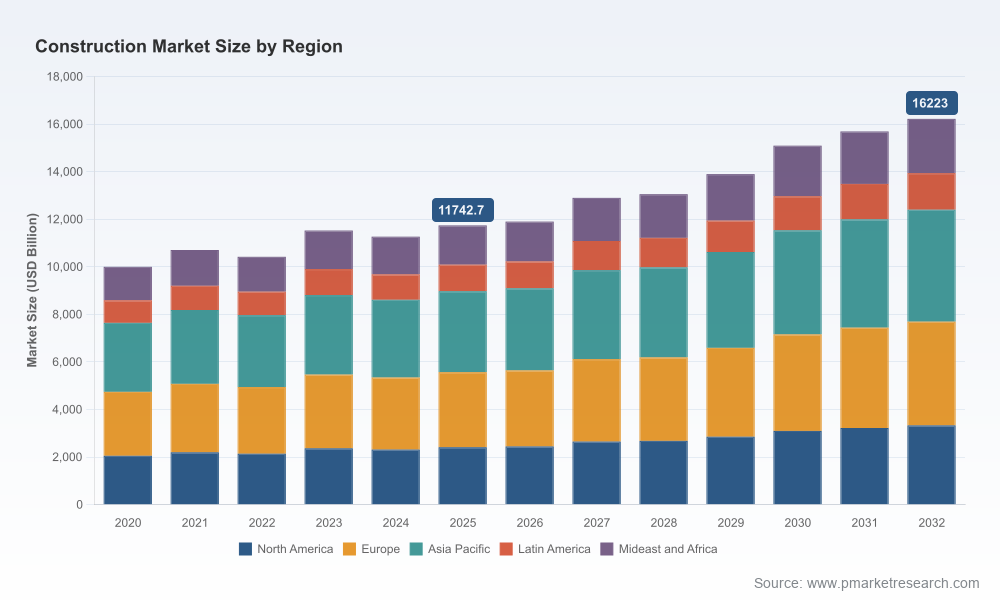

Our base-year sizing pegs the global construction market at roughly USD 11.7 trillion in 2025 (base year). After a period of uneven recovery across 2020–2025, the market resumes steady momentum: we project a compound annual growth rate of 4.7% through the 2026–2032 forecast horizon, with the market trending toward the mid-to-high teens of trillions by 2032. These topline dynamics frame three immediate implications for corporate decision-makers in 2026:

Construction Market

- Stable, above-inflation growth creates an attractive backdrop for disciplined capacity expansion and aftermarket investments.

- Mid-cycle acceleration phases will favor firms that can rapidly scale services and digital offerings, rather than capital-intensive new product ramps with long lead times.

- Macroeconomic volatility — notably commodity and tariff-driven cost shocks — will determine margin outperformance more than topline share gains for many players.

Competitive structure and concentration — room for differentiation

Industry concentration remains moderate: the top three firms account for roughly 28.5% of global market share and the top five for about 32.0%. That structure creates a dual strategic environment. Global OEMs retain scale advantages in R&D, financing, and distribution, while regional specialists and equipment-as-a-service providers can capture entrepreneurial share through localized service excellence and tailored financing offers.

Construction Market

Our analysis examines the strategic postures of the market’s leading OEMs and system providers — including Caterpillar, John Deere, Komatsu, Volvo Construction Equipment, Hitachi Construction Machinery, Liebherr, SANY, XCMG, CNH Industrial, and Terex — across four dimensions: product portfolio, digital/automation capabilities, go-to-market network, and aftermarket service economics.

- Caterpillar: continues to leverage scale in heavy equipment, finance, and global parts networks; winning on total cost of ownership propositions in large civil programs.

- John Deere: advancing operator-focused technology in midsize and compact rigs, positioning to win in urban and contractor segments where ease-of-use and productivity per operator are decisive.

- Komatsu: pushing automation and intelligent machine control; its recent articulations at major trade shows underline a push into precision earthmoving and fleet orchestration software.

- Volvo CE: increasingly focused on machine safety, fuel efficiency, and portfolio refreshes to capture premium segments and strengthen U.S. presence after recent product showcases.

- Japanese and European players (Hitachi, Liebherr): emphasizing hydraulic reliability and integrated material handling systems that favor infrastructure and long-duration projects.

- Chinese OEMs (SANY, XCMG): scaling rapidly through competitive pricing, product breadth, and growing global distribution; they are an expanding force in emerging markets and price-sensitive segments.

- Cnh Industrial and Terex: niche strength in lifting, aerial, and mixed construction-agricultural solutions, with differentiated channel strategies.

For executives, the competitive takeaway is clear: scale matters, but it no longer guarantees insulation from margin disruption. The winners in 2026 will be those who combine product reliability with software-enabled productivity, nimble distribution, and value-added services that can be monetized post-sale.

Key industry shocks shaping 2026 decisions

Several industry dynamics are reshaping capital allocation and procurement choices going into 2026:

- Raw-material inflation and tariffs: Steel and aluminum input costs have surged, with material price indices experiencing double-digit year-over-year jumps and steel/aluminum tariffs ratcheted up mid-2025. These dynamics accelerate cost escalation and force new supplier strategies, including long-term hedges, localized sourcing, and vertical integration evaluations.

- Labor scarcity: Persistent labor shortages are elevating project timelines and increasing the value of productivity-enhancing equipment (automation, telematics, remote operation). Firms that can demonstrably reduce labor hours per output will command premium pricing and faster market penetration.

- Trade-show and product-cycle signals: Recent product showcases (e.g., Komatsu at CONEXPO-CON/AGG and Volvo CE’s portfolio refresh) reveal industry priorities — automation, articulated transport efficiency, and compaction performance — which in turn influence procurement specifications for large civil and infrastructure programs.

What the report contains — practical, actionable assets for 2026

This study is built for immediate operational use by corporate strategy, product management, procurement, and M&A teams. Key deliverables include:

- Topline sizing and a 2026–2032 forecast model incorporating scenario branches for high/low commodity paths and tariff outcomes.

- Strategic segmentation frameworks across region, type, and application — with demand drivers, buyer economics, and supplier margins analyzed at a level suitable for board-level investment decisions.

- Supply-chain stress tests that quantify cost-to-complete under steel and aluminum price shocks and offer policy-ready mitigation playbooks (e.g., index-linked procurement contracts, regional sourcing corridors, and inventory financing structures).

- Commercial playbooks for OEMs and rental houses: pricing elasticity analyses, bundling strategies between equipment and connected services, and aftermarket monetization roadmaps.

- Competitive intelligence dossiers for the leading 10 vendors, including capability matrices, product roadmaps, and identified white-space opportunities for entrants or incumbents seeking adjacent expansion.

- M&A and alliance heatmaps: where consolidation creates value, thresholds for scale-driven synergies, and integration risk matrices tailored for 2026–2028 timeframes.

- Executive dashboards and scenario workbooks that allow rapid stress-testing of strategic options ahead of board cycles and capital-planning rounds.

Note: in keeping with our "preview" principle, this introduction highlights the report’s practical utility without disclosing the full granular segment matrices and precise subregional splits. Those details are available in the full report via our source page.

Strategic moves to prioritize in 2026

Based on our analysis, we recommend five tactical priorities for firms operating in or adjacent to the construction market:

- Reprice and renegotiate with speed. Index-linked clauses and dynamic margins will be essential to protect profitability amid input volatility.

- Prioritize aftermarket capture. Service contracts, digitized telematics, and predictive maintenance materially expand lifetime value and reduce cyclicality.

- Accelerate automation selectively. Invest where labor scarcity and safety exposure deliver the fastest ROI (e.g., site automation, fleet orchestration, remote operation for repetitive earthmoving tasks).

- Hedge supply risk through diversification. Combine global sourcing with nearshoring options for critical steel- and aluminum-intensive components.

- Make targeted M&A or partnerships for capability gaps. Focus on software, telematics, and regional service platforms rather than broad-scale bolt-ons that dilute focus.

How PW Consulting’s approach helps executives act

Our methodology blends primary interviews with contractors, OEM leaders, and rental operators, proprietary demand-synthesis models, and scenario-based stress testing. The result is not just a set of forecasts, but an operational playbook that helps executives:

- Translate commodity and tariff shocks into pricing and procurement actions within 90 days;

- Create investment cases for product electrification or automation with clear payback timelines under multiple demand scenarios;

- Identify the handful of aftermarket and digital services that move EBITDA in the next two years, and build pragmatic go-to-market steps to capture them.

Final perspective and next steps

The construction market entering 2026 is simultaneously large, growing, and exposed to concentrated operational risks. A 4.7% forecast CAGR through 2032 signals reliable demand, but commodity inflation, tariff policy, and labor shortages will determine which firms capture sustained profitability. Our report equips decision-makers with the quantitative models, competitive insight, and executable playbooks needed to prioritize investments, structure deals, and reshape go-to-market models over the coming 18 months.

For the complete dataset, regional and application-level breakouts, and the operational toolkits referenced above, please consult the full Construction Market report on the PW Consulting source page. The intelligence you need to make high-conviction decisions in 2026 is assembled and ready for immediate enterprise use.

For detailed analysis of this topic, please visit the official page:Construction Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com