SMD Tantalum Capacitor Market 2026 to Reach US$ 3.39 Billion by 2032 at 6.4

Other |

2026-06-23 10:40:38

As the eculizumab (Soliris) marketplace enters a new phase of competitive intensity, strategic decisions made in 2026 will disproportionately determine commercial outcomes through the remainder of the decade. Our market baseline (base year 2025) values the global Soliris market at approximately USD 5,100 Million (revenues expressed in Million USD), following a steady recovery from the pandemic-era trough in 2020. Using our harmonized forecasting framework, we project a compound annual growth rate (CAGR) of 5.5% across the 2026–2032 forecast window, with the market approaching roughly USD 7,200 Million by 2032 under the base-case assumptions.

Soliris (Eculizumab) Market

These headline metrics mask a complex interplay of product lifecycle events, biosimilar entry, regulatory evolutions and payer behavior that will shape differentiated outcomes across geographies, indications and channels. This article outlines the strategic value of our full research for 2026 corporate planning, highlights the competitive dynamics you must account for now, and explains which analyses in the full report are mission‑critical to operationalize immediate plans.

Soliris (Eculizumab) Market

Timing-sensitive exclusivity and indication dynamics: Several regulatory and exclusivity milestones converge in 2026, creating asymmetric windows of opportunity and risk for originator and biosimilar players alike.

Soliris (Eculizumab) Market

Biosimilar commercialization already underway: The first approved biosimilar has moved into U.S. commercialization, altering contracting leverage, hospital formulary dynamics and procurement timelines.

Lifecycle interventions matter: Recent pediatric approvals and post‑marketing safety dossiers have extended label breadth for the originator, changing patient population assumptions and reimbursement negotiations.

Concentration compresses strategic options: A small group of manufacturers and commercial partners dominate supply and route-to-market, meaning that partnership negotiations and supply agreements have outsized impact on access and pricing outcomes.

Robust market sizing and forecasting (historical 2020–2025, base year 2025, forecast 2026–2032) with transparent assumptions and sensitivity testing around price, uptake and policy shocks.

Scenario models modeling biosimilar penetration speeds, indication expansion outcomes and payer response curves to quantify revenue and margin trajectories under alternative futures.

Commercial impact matrices—payer negotiation playbooks, hospital/clinic contracting tactics, and value‑evidence roadmaps tailored for originator and biosimilar entrants.

Regulatory and reimbursement tracker, highlighting label changes, REMS program amendments and orphan/exclusivity timelines that materially influence access.

Supply‑chain risk maps and manufacturing capacity analysis, including contingency approaches to secure biologics supply and to negotiate manufacturing SLAs with third‑party producers.

Competitive profiles and strategic playbooks for the leading participants — their strengths, market positioning and commercial levers — coupled with trigger‑based advisories for M&A, licensing or defensive investments.

An annex containing the underlying time series (2020–2032), methodological notes, and the full set of model inputs used to generate the public topline forecasts.

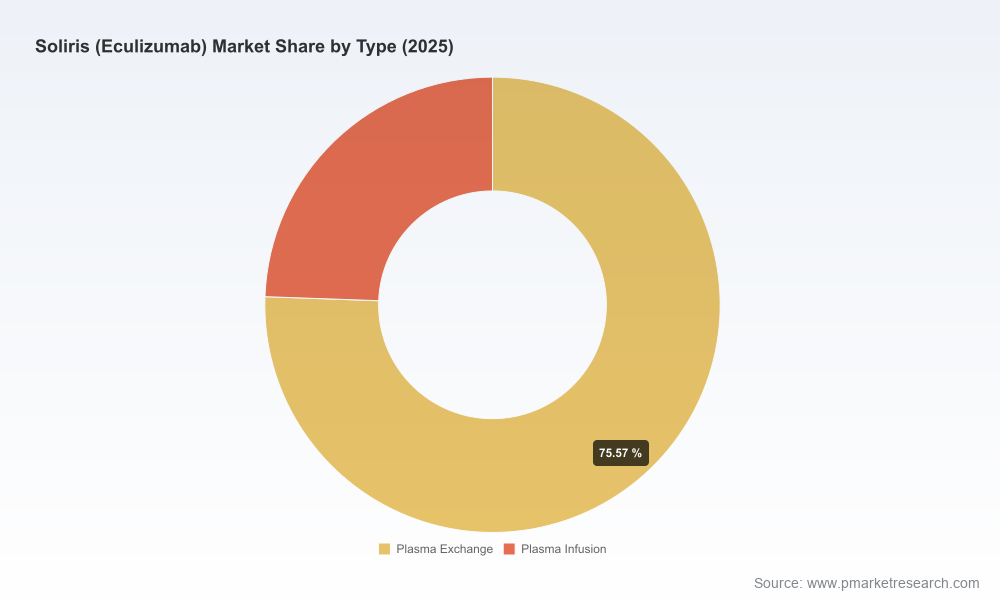

Note: this preview intentionally omits granular region-by-region, indication-by‑indication and channel breakdowns. Those essential segment-level tables and country forecasts are available exclusively in the full report and accompanying data pack.

The competitive field has consolidated around a few vertically integrated players and specialist partners. The originator franchise benefits from deep clinical legacy, recent label expansions (including pediatric populations) and established patient support programs that reduce financial friction for infusion therapies. These strengths help preserve demand and provider familiarity even as biosimilars enter the market.

At the same time, strategic partnerships between established biosimilar manufacturers and commercial networks have shortened the path to meaningful U.S. distribution. Manufacturing arrangements that localize supply for major markets, coupled with experienced commercialization partners, materially shorten commercialization risk and accelerate tender responsiveness. The practical consequence: pricing and contracting pressures will emerge faster in certain channels (e.g., hospital tenders, integrated systems), while pockets of protected demand will persist where value perception and patient support differentiate the originator.

Recent notable developments that should inform 2026 strategy include:

Post‑marketing safety and long‑term efficacy data presented at major clinical fora, which support durable use in newly secured indications and strengthen the clinical case in payer discussions.

Regulatory label updates expanding pediatric use in selected indications—these extend target populations and change lifetime value calculations for treated cohorts.

Commercial biosimilar launches in major markets driven by manufacturing-capable partners and licensed commercialization agreements—these accelerate competitive exposure in high‑value geographies.

Adjustments to REMS and patient support mechanics that alter the operational cost of access and have knock‑on effects for hospital economics and payer authorizations.

Immediate (0–6 months): Rebaseline forecasts and contracting models to reflect pediatric label changes and the operational impact of biosimilar availability in prioritized geographies. Lock in supply agreements or volume options with manufacturers to manage margin volatility.

Near term (6–18 months): Accelerate payer evidence generation (real‑world outcomes and health economic dossiers) tied to the new label populations; deploy targeted patient access programs to blunt biosimilar switches in high‑risk cohorts.

Commercial defense: Implement differentiated contracting (outcomes‑linked agreements, bundled infusion pricing) where buyers have bargaining power; leverage patient support programs to maintain adherence and minimize switching risk.

Strategic growth (12–36 months): Evaluate selective alliances with biosimilar manufacturers for co‑promotion or supply security; consider bolt‑on acquisitions or in‑licensing to broaden immunology/ complement inhibitor portfolios.

Longer horizon (24+ months): Institutionalize scenario planning and a playbook for rapid repricing events; diversify manufacturing and invest in follow‑on assets to offset product concentration risk.

The base case in our model assumes continued clinical adoption supported by label expansion and managed biosimilar uptake, delivering the headline 5.5% CAGR to 2032. However, directional outcomes bifurcate materially under alternative assumptions:

Upside: Stronger than expected uptake in expanded pediatric and neurological indications, coupled with slow biosimilar penetration in specialty infusion pathways, can accelerate market value beyond base projections.

Downside: Rapid, wide‑scale biosimilar substitution in hospital tenders and aggressive payer‑driven price concessions can compress revenues and margins, forcing accelerated lifecycle actions or additional access investments.

Operational shock: Manufacturing disruptions or regulatory policy shifts limiting off‑label access would reweight regional forecasts and require urgent reallocation of commercial resources.

Portfolio prioritization: Decide whether to double‑down on lifecycle extensions (indication expansion, pediatric evidence) or redeploy capital toward alternative complement inhibitors and next‑generation modalities.

Pricing and contracting: Build dynamic pricing playbooks keyed to tender cycles and hospital formulary dynamics rather than static list price changes; negotiate supply guarantees where margin preservation matters.

Commercial partnerships: Evaluate the commercial value of entering distribution alliances versus in‑house launches, with a focus on speed to market and channel control in high‑value territories.

M&A and licensing: Use the market scenarios to set trigger thresholds for opportunistic acquisitions of adjacent assets, or to license rights that mitigate concentration risk.

Our Soliris market research is designed as a decision‑grade tool for 2026: it synthesizes rigorous forecasting, event‑driven scenario planning and a pragmatic commercial playbook that executives can deploy immediately. The full deliverable includes the granular regional and indication breakdowns, country‑level forecasts, competitive share matrices and an executable slide pack that operational teams can use in negotiations and board discussions.

As a deliberate preview, this article showcases the analytical depth you need to make confident choices in 2026 while withholding the detailed segment tables and numerical splits that most directly drive contracting and tactical market moves. Access to those segmentation tables, model files, and proprietary scenario runs is available through the full report and data pack.

Contact PW Consulting to schedule a tailored briefing: we will walk through the underlying time series, test your internal assumptions against our scenarios, and produce a 60‑day playbook customized to your position in the Soliris value chain.

For detailed analysis of this topic, please visit the official page:Soliris (Eculizumab) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com