Low-Code Development Platform Market Size, Forecast & Strategic Outlook 2025–2031

Other |

2026-07-06 14:34:05

As organizations re-architect customer engagement and transactional flows for a post-pandemic world, A2P SMS and cloud communications platforms (cPaaS) are no longer niche plumbing — they are a strategic layer in digital experience stacks. PW Consulting’s latest market study, with a 2025 base year and a seven-year forecast window through 2032, synthesizes macro growth, vendor strategy, regulation and operational risk into an executive-ready roadmap for decisions in 2026. This commentary previews the study’s strategic value while preserving the proprietary, segment-level figures that drive boardroom moves — an intentional “trailer” to prompt deeper engagement with the full report.

A2P SMS & cPaaS Market

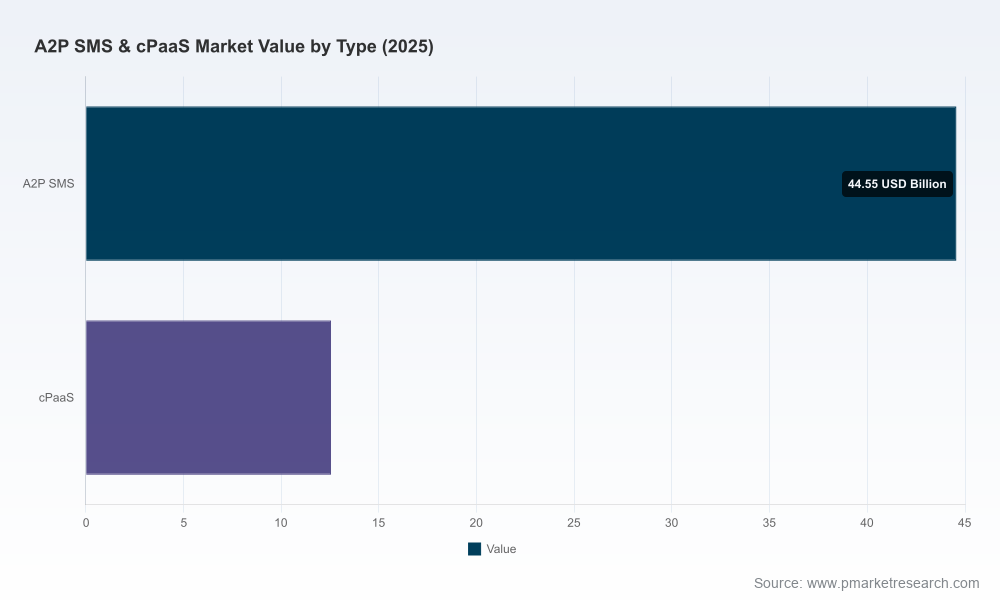

The sector has shown consistent expansion through the early 2020s and continues to accelerate as enterprises embed messaging into authentication, notifications, marketing and omnichannel journeys. Our aggregated market model — informed by historical trends from 2020–2025 and scenario-driven forecasts through 2032 — indicates a mid-single-digit compound annual growth rate (CAGR) across the forecast period. By 2026 the market steps into a new phase where scale economics, product differentiation and regulatory clarity translate into materially different outcomes for incumbents and challengers.

A2P SMS & cPaaS Market

Two strategic takeaways flow from the topline trajectory: first, growth is durable and broad-based across use cases tied to identity, commerce and customer engagement; second, the path to profitability and competitive defensibility depends on operational leverage (direct routing, carrier relationships, platform-driven value-adds) and cost control (data center and energy exposure). The latter is rapidly rising on executive agendas as energy and infrastructure costs become a determinant of pricing power and margin stability.

A2P SMS & cPaaS Market

Vendor selection and partnership design: Buyers must evaluate providers not only on API capabilities, latency and global reach, but also on route ownership, regulatory compliance posture and energy-cost exposure. Our study decodes these dimensions and provides an operational scorecard optimized for procurement and architecture teams.

Commercial strategy and pricing: The industry’s moderate concentration profile means scale matters — our competitive index identifies where pricing compression is likely and where premium positioning is achievable through advanced messaging formats and value-added services.

M&A and inorganic playbooks: For strategists considering tuck-ins or roll-ups, the report offers diligence frameworks and target heuristics that align with the industry’s growth vectors and the cost drivers that will shape margin arbitrage opportunities.

Risk and resilience planning: From carrier regulatory shifts to electricity price volatility and data-center footprint risk, the study provides scenario analyses that quantify balance-sheet and service-delivery exposure under stress cases relevant for 2026 planning cycles.

Actionable market sizing and forecasts (historical 2020–2025 and 2026–2032 outlook) with scenario sensitivity and assumptions mapping.

Go-to-market frameworks for vendors and enterprise buyers: product-to-value maps, channel and direct sales playbooks, and partner economics templates.

Operational scorecards evaluating routing models, carrier relationships, latency and deliverability metrics, and energy exposure from underlying infrastructure.

Regulatory and compliance compendium that decodes jurisdictional nuances, with pragmatic checklists for lawful interception, consent management and cross-border data flows.

Vendor benchmarking (functional, strategic and financial dimensions) and an M&A readiness index for target screening.

Implementation guides and migration roadmaps — from legacy SMS homing to modern cPaaS architectures and Rich Communication Services (RCS) pilots.

Executive playbook with prioritized initiatives, quick-win KPIs and a 12–36 month investment map aligned to expected market inflection points.

The competitive field blends global platform leaders, telco-aligned challengers and regional specialists. The market exhibits moderate concentration: the top three vendors control a meaningful share, and the top five extend nearly half of the market — a structure that rewards scale, carrier connectivity and differentiated product suites.

Twilio (San Francisco) — A dominant API-first play with broad developer mindshare, extensive global coverage and a push into omnichannel orchestration. Strengths: strong developer ecosystem, flexible APIs, platform extensibility. Challenges: margin pressures from reseller routes and the need to continuously show differentiated enterprise features beyond basic SMS.

Infobip (London) — A well-capitalized global operator with deep direct-to-carrier relationships and a comprehensive suite that spans messaging, email and chat. Strengths: routing density, enterprise sales motion, compliance expertise. Challenges: integrating acquisitions into a unified product experience at scale.

Sinch (Stockholm) — Focused on CPaaS and messaging scale, Sinch competes on carrier-grade routing and breadth of messaging products. Strengths: carrier ties and international reach. Challenges: translating traffic scale into differentiated monetization.

Vonage (Holmdel) — Positioned as a communications platform for business, with strengths in UCaaS integration and programmable messaging. Strengths: convergence of voice and messaging for contact centers. Challenges: balancing legacy UC economics with pure-play messaging dynamics.

RingCentral (Belmont) — Enterprise communications leader extending into messaging via platform integrations. Strengths: enterprise footprint and bundled offerings. Challenges: competitive differentiation in high-volume A2P segments.

Bandwidth (Raleigh) — Carrier-operator hybrid with control of network assets; attractive for buyers seeking route stability and compliance. Strengths: vertical integration and pricing control. Challenges: expansion beyond core markets.

Kaleyra (Milan) — Strong in enterprise messaging with emphasis on regional compliance and sector-focused solutions. Strengths: industry vertical plays, EU focus. Challenges: scaling global operations cost-effectively.

Plivo (Austin) — Developer-focused CPaaS with pricing competitiveness and API simplicity. Strengths: cost-effective routing and developer adoption. Challenges: enterprise packaging and carrier relationships for large-scale A2P traffic.

Bird (Amsterdam) — Specialist in programmable messaging with innovation in value-added features. Strengths: agility and partner integrations. Challenges: visibility and scale versus tier-one incumbents.

Tata Communications (Mumbai) — Telco-rooted provider with global network assets and enterprise trust in regulated markets. Strengths: network reach and carrier relationships. Challenges: product velocity compared to pure-play CPaaS vendors.

Route Mobile (Mumbai) — Regional specialists with strong presence in high-growth markets. Strengths: localized compliance and cost-competitive routes. Challenges: margin squeeze and diversification outside core geographies.

Mitto (Zug) — Focused on deliverability and route transparency, attractive to enterprises with stringent compliance needs. Strengths: transparency and quality routing. Challenges: scaling global enterprise sales.

CM.com (Breda) — European CPaaS player pushing RCS and conversational commerce integrations. Strengths: RCS initiatives and EU-centric solutions. Challenges: global scale.

Commio (Raleigh) — Nimble provider advancing Rich Business Messaging with recent product launches; recognized with industry awards for innovation. Recent: March 2026 launch of InstantApp™ for RCS, signaling investment in richer conversational channels. Strengths: product innovation and agility. Challenges: wider carrier reach for large-scale deployments.

Teliqon (Tallinn) — Emerging regional player with specialised compliance and developer-friendly tools. Strengths: focused regional offers. Challenges: market visibility.

Twixor (Singapore) — Conversational CX specialist combining messaging with workflow automation. Strengths: workflow integration for APAC enterprises. Challenges: competing with global CPaaS ecosystems.

TXTImpact (New York) — Focused on U.S. enterprise messaging with service models for marketing and engagement. Strengths: targeted U.S. market expertise. Challenges: global expansion.

OpenMarket (Seattle) — Enterprise-grade messaging specialist with strong retail and financial services use cases. Strengths: enterprise solutions and compliance. Challenges: competing on price with larger CPaaS platforms.

Two external dynamics deserve elevated attention in 2026 planning:

Energy and data-center exposure: Wholesale electricity and capacity-price volatility have leapt onto the cost curve for platform providers. Rising regional electricity costs and increases in capacity pricing materially alter unit economics for providers with owned infrastructure or long-term colocation commitments. The industry must model energy sensitivity into pricing and evaluate architectural alternatives — edge routing, multi-cloud strategies and carrier-hosted interconnections — to mitigate margin erosion.

Regulatory clarity and operational impact: The legal classification of messaging services influences obligations, regulatory reporting and permissible commercial models. The precedent that SMS and MMS are treated as information services, and that A2P falls outside certain interconnected service definitions, creates a governance baseline but does not eliminate jurisdictional complexity. Companies must maintain proactive compliance programs, especially for cross-border flows, consent management and emergent CPaaS features such as RCS-based commerce.

Audit route economics and diversify supply chains: Quantify direct vs. reseller routing, test alternate carriers, and build contingency capacity to defend deliverability and margins.

Invest selectively in richer channels: Pilot RCS and conversational commerce where customer lifetime value justifies higher platform cost; prioritize verticals with measurable conversion gains.

Embed energy-risk into procurement: Require vendors to disclose energy exposure and efficiency plans; when feasible, negotiate price collars or migrate workloads to lower-cost regions or carrier-hosted points of presence.

Operationalize compliance: Centralize consent lifecycle, message content governance and data residency controls to reduce enforcement risk and speed cross-border expansions.

Use the vendor scorecard: Apply a weighted evaluation (routing ownership, deliverability SLAs, compliance posture, API breadth, TCO) for any procurement or M&A decision — our report provides a ready-to-use template.

This preview outlines the strategic contours that will shape A2P SMS and cPaaS decisions in 2026: durable market growth, margin pressure points from infrastructure costs, a competitive field where scale and route quality matter, and regulatory forces that require disciplined compliance execution. PW Consulting’s full study converts these insights into specific, operational intel — granular segmentations, vendor scorecards, financial models and scenario tables — intentionally withheld here to preserve the value of the dataset and to encourage direct engagement with the full deliverable.

For procurement leaders, product executives, and M&A teams preparing 2026 budgets and roadmaps, the full report provides the calibrated intelligence needed to prioritize investments, select partners, and design resilient operations. Access the comprehensive study to obtain the detailed tables, annexes and templates that translate strategy into execution-ready plans.

For detailed analysis of this topic, please visit the official page:A2P SMS & cPaaS Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com