Mahadev Book – Modern Betting Platform Delivering Secure Gameplay And Smooth User Experience

Games |

2026-05-14 11:54:55

As companies prepare their 2026 capital allocation and operational strategies, the induction furnace (IF) market presents a clear, measurable opportunity — and a set of execution risks — that require disciplined, data-driven responses. PW Consulting’s latest market induction provides a forward-looking compass: the global IF market, valued at approximately USD 1,750 Million in our base year (2025), exhibits steady expansion at a compound annual growth rate (CAGR) of 5.32% across the 2026–2032 forecast window, reaching roughly USD 2,485 Million by 2032. These headline numbers are the starting point for decisions that will shape technology roadmaps, procurement pipelines, and M&A agendas in the metal-processing ecosystem.

Induction Furnace (IF) Market

Timing of investments: With measured growth rather than explosive expansion, the IF market rewards selective, capability-led investments rather than broad capacity expansion. CapEx and modernization initiatives in 2026 should prioritize energy efficiency, digital controls, and modularity to capture cost savings while preserving flexibility.

Induction Furnace (IF) Market

Regulatory alignment: Near-term regulatory measures — notably the EU’s Energy Efficiency Directive requiring cumulative end-use energy savings in 2026–2027 — alter procurement specifications and total cost of ownership (TCO) calculations. Companies that align equipment selection with regulatory trajectories will reduce compliance risk and access incentives.

Induction Furnace (IF) Market

Supplier concentration matters: Market concentration indicators show a market where leading vendors control a majority share, creating both supplier risk and partnership opportunities. Procurement strategies must balance negotiating leverage against the need for proven technology providers.

Energy efficiency as a competitive axis. Induction systems typically deliver 25–30% energy savings versus conventional melting technologies. That efficiency delta is now a primary procurement filter — not an optional advantage. Buyers in 2026 should expect efficiency metrics (kWh per tonne), peak-demand management features, and integration with onsite renewables to be mandatory evaluation criteria.

Decarbonization and electrification. Policy signals and buyer demand are converging on electrification pathways. Public- and private-sector commitments to CO2-neutral foundry operations mean induction furnaces are increasingly positioned as compliance enablers, especially in jurisdictions with tightening industrial emissions controls.

Input-cost volatility. Fluctuating copper and refractory-material prices compress manufacturer margins and can propagate price instability to end buyers. Strategic procurement in 2026 should include supplier cost pass-through clauses, hedging options, and material-substitution assessments.

Labor and automation. High initial capital requirements combined with skilled-labor shortages are pushing buyers toward automated, low-touch designs. Investment in automation and remote diagnostics reduces operating risk and shortens the payback horizon for higher-capability systems.

Robust market architecture: an independently validated market sizing from 2020–2025 with a detailed scenario-based forecast to 2032 that crystallizes demand drivers and sensitivity to macro variables.

Decision-ready TCO models: configurable calculators that capture CapEx, energy consumption, maintenance, consumables, and regulatory compliance costs to compare legacy vs. induction-based pathways.

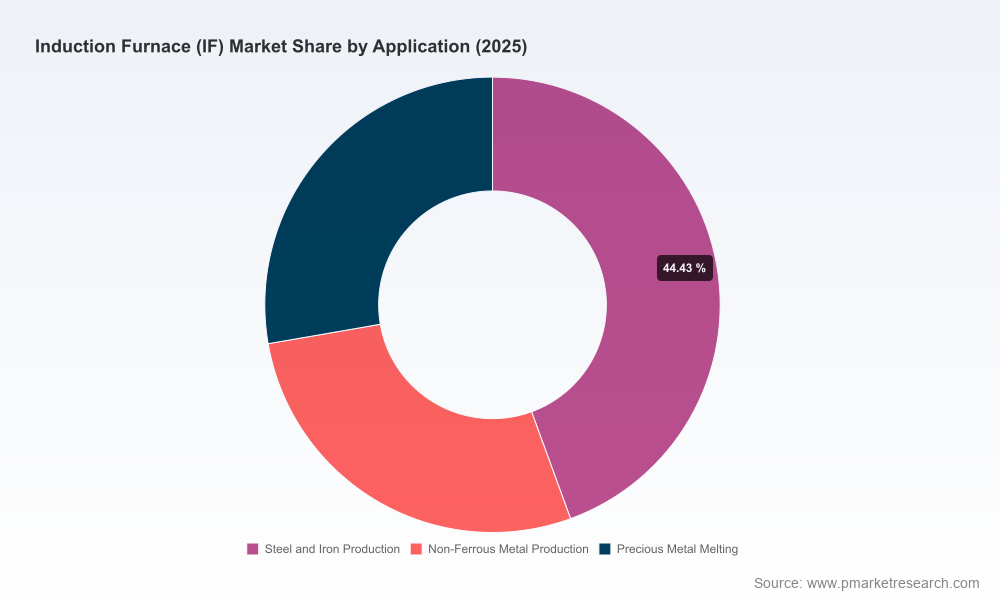

Procurement playbooks: supplier selection criteria, contract templates, service-level benchmarks, and ROI thresholds tailored to different use cases (steel, non-ferrous, precious metals, and industrial heating).

Technology maps: comparative analysis of coreless vs. channel designs, frequency and power electronics trends, automation layers, and retrofit opportunities for existing foundries.

Competitive intelligence: validated profiles, capability matrices, and go-to-market strategies for the leading vendors shaping the market (detailed supplier scorecards are reserved for the full report).

Regulatory and scenario analysis: policy impact assessments, energy-price sensitivity runs, and recommended compliance pathways under near-term European and global regulatory scenarios.

M&A and partnership playbook: target archetypes, valuation multipliers, and integration checklists for acquirers seeking inorganic scale, channel access, or technology tuck-ins.

The competitive topology of the IF market is defined by a set of established global players and nimble regional manufacturers. Incumbents leverage long product pedigrees, deep service networks, and broad application portfolios, while regional firms compete on price, local customization, and responsiveness. For 2026 strategies, three themes emerge:

Platform specialization vs. breadth. Global leaders offer integrated platforms (melting, holding, pouring, controls, and service) that appeal to large steel and foundry customers seeking single-source responsibility. Niche vendors win in applications that require bespoke configurations or cost-sensitive replacements.

Electrification proofs and projects. Recent implementations — including projects where induction systems replaced cupola furnaces and successful deployment of high-tonnage units in steelmaking operations — validate the economics of electrification at scale. These cases demonstrate that substitution is no longer theoretical but operationally proven in 2024–2025 rollouts.

Service and digital aftercare. As adoption rises, lifecycle service and remote diagnostics become differentiators. Vendors who can guarantee uptime, spare-part availability, and predictive maintenance will command premium positioning.

Inductotherm Group: A market leader noted for comprehensive coreless and channel offerings and a global service footprint. Strategic buyers should view Inductotherm as a benchmark for quality and aftermarket capability.

EFD Induction: Specialist technology provider with deep expertise in industrial induction heating. Their emphasis on automotive and renewables applications positions them well for customers prioritizing high-frequency and precision heating solutions.

OTTO JUNKER GmbH: Strong European engineering pedigree with recent projects demonstrating effective cupola-to-induction substitution and electrification of billet heating — evidence of both technical capability and project delivery strength.

ABP Induction, Ajax Tocco, Radyne, SMS Elotherm: Vendors with distinct strengths in custom solutions, process hardening, and rolling/forging applications. Their investments in power electronics and controls merit attention from buyers requiring vertical integration.

Electrotherm E&T and Agni Induction Meltech: Regional leaders with cost-competitive offerings and proven high-tonnage deployments. These suppliers are attractive for cost-sensitive large-scale steel projects and local content requirements.

Electrification projects and commercial operations in 2024–2025 have proven feasibility for large-tonnage induction furnaces in steelmaking — a turning point for suppliers and buyers who were previously cautious about scale.

Project implementations replacing traditional cupolas with induction systems reinforce the low-carbon narrative and create reference cases that accelerate vendor selection cycles in regulated markets.

Advancements in billet-heater electrification and successful commissioning of multiple high-capacity units underscore the sector’s momentum toward full-process electrification in select industrial corridors.

Prioritize energy-first procurement. Use TCO models that weight energy and regulatory costs over a 7–10 year horizon to identify investments with the shortest economic and emissions payback.

Segment your supplier strategy. Blend incumbents for mission-critical capacity with regional suppliers for cost-competitive projects and fast service. Negotiate fixed-service arrangements that protect against spare-part inflation.

Accelerate digital and automation pilots. Target two-to-three facilities in 2026 for retrofit/digitalization pilots (remote monitoring, predictive maintenance) to reduce labor dependency and improve uptime.

Manage material-price risk. Implement procurement clauses and alternative-material validation to mitigate copper and refractory-price volatility impacts on new builds and spares inventories.

Prepare for regulatory tailwinds. In regions with aggressive energy efficiency or emissions mandates, accelerate replacement cycles for legacy melting units to capture incentives and avoid compliance-driven shutdowns.

Use consolidation opportunities selectively. For buyers seeking to scale quickly, target tuck-in acquisitions with proven local channels and service networks rather than headline-making bolt-on deals.

Our induction furnace market study combines audited market-sizing, scenario-based forecasting, vendor benchmarking, and operational playbooks designed for executives making 2026 allocation choices. The full report contains the granular splits by type, application, capacity, and region, detailed vendor scorecards, and downloadable TCO models that allow you to stress-test investment alternatives under your corporate constraints. Those core segmentation tables and supplier-level financials are intentionally withheld here to preserve the integrity of the analysis and to ensure readers access the full dataset on our report portal.

For procurement teams: request the TCO workbook to model CapEx/OpEx scenarios for proposed 2026 projects.

For corporate strategy and M&A teams: obtain the vendor scorecards and target archetype maps to prioritize acquisition or partnership targets.

For plant operations: secure the retrofit and automation playbooks to scope low-disruption pilots in 2026.

PW Consulting’s Induction Furnace Market study is designed to be both a strategic north star and an operational manual for 2026. The market’s stable growth trajectory, coupled with regulatory and energy imperatives, makes this a tactical moment: firms that move with clarity — aligning procurement, operations, and M&A to the energy-efficiency and electrification trends — will secure durable advantages. For the full dataset, segmented analytics, and supplier scorecards, please consult the complete report on our website.

For detailed analysis of this topic, please visit the official page:Induction Furnace (IF) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com