Powering the Long Haul – Growth Dynamics in the Hydrogen Fuel Cell Commercial Trucks Market

Other |

2026-05-15 12:20:14

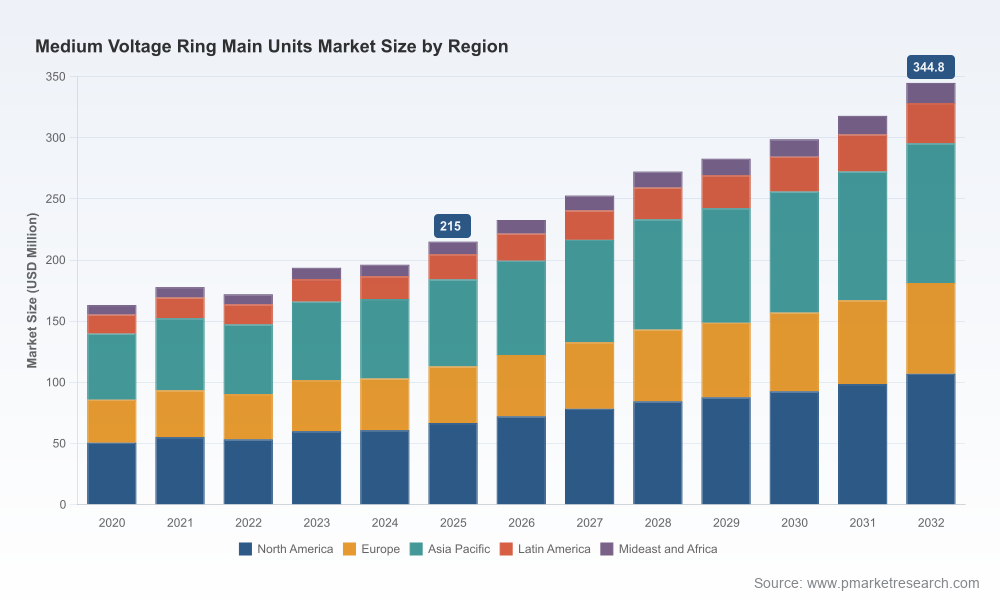

This preview frames PW Consulting’s full Medium Voltage (MV) Ring Main Units (RMU) Market study (base year 2025, historical 2020–2025, forecast 2026–2032). The RMU market has experienced a steady recovery and structural transformation in recent years: market value rose noticeably from the 2020 trough into 2025, and our forecast anticipates a compounded annual growth rate (CAGR) of c. 6.98% through 2032, reaching roughly USD 345 million by the end of the projection horizon. For energy companies, OEMs, investors and utilities planning for 2026, this research translates macro momentum and regulatory pressure into practical, executable choices — from product selection and procurement timing to capex allocation and digitalization roadmaps.

Medium Voltage Ring Main Units Market

Market timing: The market is no longer homogeneous. Renewables integration, urban densification, and network digitization create differentiated pockets of demand that reward targeted product strategies and timely manufacturing scale-ups.

Medium Voltage Ring Main Units Market

Regulatory inflection: Strengthened environmental rules and GWP constraints have turned SF6 dependence into an operational and reputational risk. By 2026, procurement and R&D decisions made today determine compliance exposure and lifecycle costs across utility fleets.

Medium Voltage Ring Main Units Market

Investment prioritization: 6.98% CAGR masks asymmetric upside for firms that combine SF6-free technologies with IoT-enabled RMUs. Identifying these asymmetries — and the exact points of margin capture — is central to capital allocation over the next 12–36 months.

Supplier selection & resilience: Low-to-moderate market concentration indicates a fragmented supplier base. This opens opportunities for strategic partnerships, private-labeling and localized manufacturing but raises supply-chain diligence requirements.

From 2020 to 2025 the RMU market expanded from a post-2020 baseline to a materially larger market by 2025. Looking ahead, our forecast models incorporate demand-side drivers (utility replacement cycles, renewable interconnection, urban expansion, and industrial automation) and supply-side constraints (SF6 availability, component lead times, and raw-material inflation). The resulting projection — mid-single-digit CAGR into 2032 — is underpinned by structural migration to SF6 alternatives, incremental electrification, and accelerated digitalization of distribution networks.

Three structural forces shape the next wave of RMU procurement and product design:

Regulatory tightening on high-GWP gases, notably the strengthened EU F-gas measures, which in certain jurisdictions now mandate SF6-free designs for specified MV switchgear deployments;

Technological substitution — mature alternatives such as clean air, solid-dielectric and next-generation fluoroketone/hydrocarbon gases — that enable SF6-free RMU architectures with competitive lifecycle costs;

Digital integration — IEC 61850-compliant monitoring and self-powered relays are standardizing remote supervision and automated fault isolation, turning RMUs into both distribution assets and data endpoints.

The RMU vendor ecosystem includes long-established global OEMs and agile regional players. Market concentration is modest: the top three players account for under one-quarter of the market, and the top five remain clustered only slightly higher — a structure that favors differentiation through technology, service and localized production rather than pure scale. Key vendor strategies we observe include:

Product platform bifurcation: Global leaders are offering parallel portfolios — SF6-free air or solid-insulated RMUs alongside high-density GIS offerings — to serve different application economics and regulatory regimes.

Digital-first propositions: Several firms have embedded IEC 61850-compatible telemetry, self-powered protection relays, and edge-analytics to deliver operational value beyond pure switching functionality.

Decarbonization and procurement plays: Established suppliers are accelerating SF6-free product rollouts and long-term framework agreements with large utilities, creating entry barriers for late movers and offering customers bundled service-plus-hardware models.

Localized capacity expansion: Manufacturing capacity investments in key markets are being executed to reduce lead times, manage tariff exposure and support utility service contracts — a crucial consideration for operators with tight replacement windows.

Representative company moves tracked in our research illustrate these dynamics: commercial contracts for SF6-free RMUs with large utilities; capacity expansion in high-growth countries; and field deployments of SF6-free and sealed-RMU solutions in challenging environments. These developments validate the thesis that technology parity and supply footprint are becoming as important as legacy brand equity.

Compliance complexity: Jurisdictional variations in implementing F-gas and parallel GWP restrictions mean that a one-size-fits-all product strategy exposes companies to retrofit costs and stranded inventory risk.

SF6 availability and alternative sourcing: Scarcity and procurement volatility for SF6 — plus the rising adoption of fluoroketone and hydrocarbon alternatives — make component sourcing maps and third-party testing essential components of supplier evaluation.

Standards and interoperability: IEC 61850 conformance for smart RMUs accelerates the value capture from distribution automation projects but raises integration costs where legacy SCADA and protection schemes remain in place.

This report is structured as an operational playbook for 2026 action. Highlights include:

Validated market sizing (by value) and a transparent forecast model (2026–2032) with scenario sensitivities for regulatory and commodity shocks.

Technology matrix and TCO models comparing SF6, clean-air, solid dielectric and fluoroketone-based RMUs across lifetime OPEX, maintenance profile and regulatory compliance costs.

Supplier benchmarking and procurement scorecards assessing product maturity, digital capabilities, manufacturing footprint, and risk exposure — designed for use in RFPs and strategic sourcing.

Go-to-market and manufacturing playbooks for OEMs: partner selection frameworks, localization thresholds, and capacity ramp templates for priority markets.

Utility decision templates: replacement vs. retrofit decision trees, staged rollout plans for fleet modernization, and use-case cost-benefit analyses for smart RMUs.

Regulatory impact scenarios explaining where SF6 restrictions will materially shift demand and how to sequence product approvals and certifications.

Case studies and supplier negotiation levers drawn from recent commercial agreements and field projects across multiple geographies.

Executives with capital deployment or procurement authority should treat the coming 12–24 months as a window for decisive action. Our recommended plays are:

Adopt a risk-segmented procurement policy: identify assets subject to imminent regulatory pressure and prioritize SF6-free replacements there, while using dual-sourcing strategies elsewhere to contain near-term costs.

Invest in interoperability and data maturity: ensure RMU purchases include IEC 61850 conformance and clear upgrade paths to reduce integration costs and unlock distribution automation value.

Secure conditional manufacturing capacity or partnerships in priority markets to shorten lead times and improve service-level economics.

Embed lifecycle TCO into capital approval: require vendors to provide full-lifecycle emissions and maintenance profiles as part of bids to capture total cost and regulatory risk.

Monitor supplier roadmaps for SF6 alternatives and field-proven reliability; prioritize partners that can demonstrate both product maturity and service networks.

This article is intended as an executive preview. To preserve the value of our granular analysis — particularly product-and-region segmentation, price curves, and vendor share tables — the full dataset, supplier scorecards, and transaction-level insights are available only in the full PW Consulting report. Those granular slices contain the precise segmentation and deployment cost models required to operationalize the strategic plays outlined above.

For utilities: request the utility edition to obtain fleet-level scenario models and retrofit decision tools that translate market dynamics into deployment schedules.

For OEMs: obtain the vendor benchmark pack to compare product portfolios against SF6-free adoption rates, digital features and manufacturing capacity gaps.

For investors and project developers: secure the investment brief that distills hot spots for M&A, strategic partnerships and scale economics in the MV RMU value chain.

In short, the MV RMU market presents a classic strategic inflection: modest aggregate growth masks differentiated commercial outcomes for players who can navigate regulatory constraints, accelerate SF6-free adoption, and pair physical hardware with digital services. PW Consulting’s full study converts these macro trends into actionable, transaction-ready intelligence for 2026. Contact us to access the complete dataset, supplier scorecards and implementation templates that operationalize the insights summarized here.

For detailed analysis of this topic, please visit the official page:Medium Voltage Ring Main Units Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com