Aircraft De-Icing Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-05 07:43:11

As companies prepare budgets, product roadmaps, and M&A pipelines for 2026, the engine filter market presents a clear growth runway — but one framed by supply volatility, regulatory acceleration, and evolving customer value expectations. PW Consulting’s new market study (base year 2025; forecast period 2026–2032) synthesizes primary research, supply-chain mapping, and scenario modelling to deliver decision-grade insights. In short: the market is neither a slow, commoditized relic nor a speculative flash-in-the-pan; it is a steady, mid-single-digit growth industry that rewards focused technical differentiation and operational resilience.

Engine Filter Market

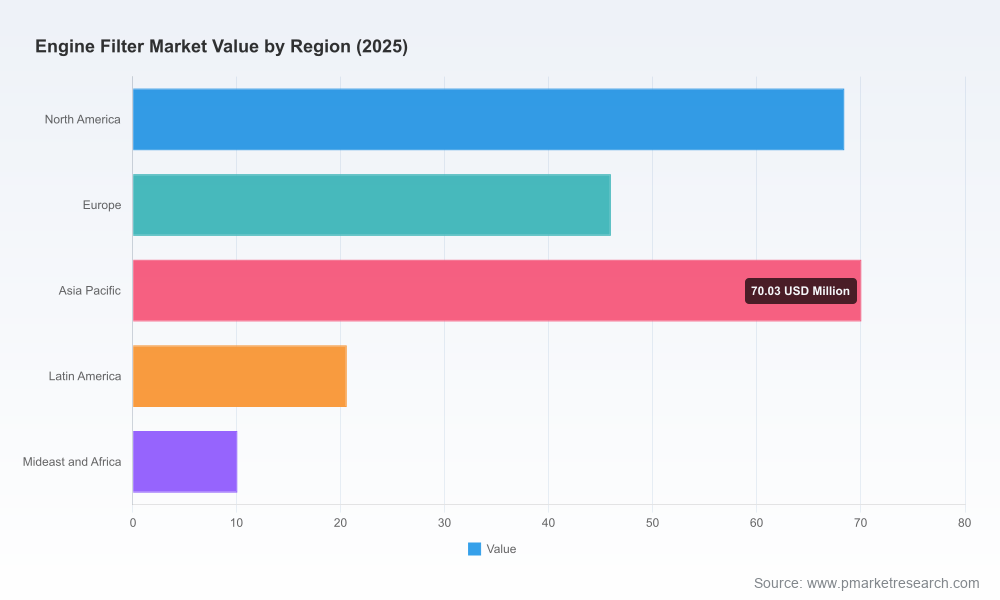

The global engine filter market reached approximately USD 215.0 million in 2025 and is projected to expand to roughly USD 344.8 million by 2032, implying a compound annual growth rate (CAGR) of about 5.5% over the forecast window.

Engine Filter Market

Market concentration is meaningful but not prohibitive: the top three players account for roughly 45.5% of market share, while the top five represent about 56.7%. This structure creates room for both scale advantages and targeted insurgent strategies.

Engine Filter Market

Our historical analysis (2020–2025) shows consistent recovery and acceleration dynamics tied to vehicle parc replacement cycles, regulatory tightening, and rising demand in diverse end markets. Forward-looking scenarios reflect sensitivity to raw material shocks, labor constraints, and emissions regulation timelines.

Three strategic inflection points make 2026 a pivotal planning year:

Regulatory and sustainability drivers are compressing product cycles. Stricter emissions and efficiency standards push engine designs that require higher-performing filtration solutions; firms that can pre-emptively align R&D with these trends capture OEM qualification windows and aftermarket premium pricing.

Supply-side fragility — particularly for specialized polymers and synthetic fibers used in filter media — introduces non-linear cost and availability risk. Companies without robust sourcing strategies face margin erosion or forced product redesigns.

Aftermarket replacement and service-based monetization pathways are becoming material contributors to lifetime value. Firms that bundle filtration with monitoring, predictive replacements, or service contracts can extract recurring revenue while improving end-customer retention.

Demand modelling with multi-scenario forecasts (base, accelerated regulation, and raw-material stress) and sensitivity analysis for pricing, material cost pass-through, and vehicle parc evolution.

Commercial playbooks: value-based pricing templates, aftermarket channel strategies (independent vs. OEM), and go-to-market blueprints for light-, medium-, and heavy-duty segments.

Supply-chain heatmaps: tiered supplier lists, single-source risk assessments, contract renegotiation levers, and cost-to-serve analytics for manufacturing footprints.

Technology roadmaps: comparative evaluation of filter media innovations (e.g., pleat-strengthening treatments, nano-structured media, sealed-design architectures) with adoption timelines and OEM qualification checklists.

Competitive benchmarking: profiles and strategic posture assessments for incumbent leaders, fast followers, and niche specialists — including product portfolios, channel strategies, and recent moves.

M&A and partnership playbook: target screening criteria, valuation heuristics, and integration risk frameworks designed to accelerate scale or capability buys without destroying engineering leverage.

The market is anchored by a mix of diversified industrials and filtration specialists. Strategic takeaways for suppliers and investors:

Parker Hannifin (Baldwin brand) leverages engineered pleat protection and lube oil filtration technologies that emphasize contaminant removal and durability. Their strength is scale and a well-recognized aftermarket brand that supports premium positioning in industrial and commercial vehicle channels.

Mann+Hummel has focused investments in air filtration engineered to sustain full service intervals and optimized combustion performance. Their technical credibility with OEMs positions them well for collaboration on next-generation engine architectures and electrified powertrains that still require auxiliary filtration systems.

Cummins (Fleetguard) brings a heavy-duty orientation, with advanced NanoForce and NanoNet technologies targeted at large-engine reliability. Their vertical integration with engine platforms creates cross-selling advantages into fleet service programs.

MAHLE’s sealed-design aftermarket filters — marketed around near-total removal efficiencies for fine particulates — exemplify how product differentiation can command channel preference and support longer replacement intervals.

Bosch mixes natural and synthetic media blends across oil and air filtration, combining materials science with scale manufacturing to deliver reliable, premium-positioned products for OEMs and high-end aftermarket segments.

For 2026, expect competition to intensify along two vectors: first, performance differentiation enabled by advanced media and design; second, service and data-enabled offerings that turn a consumable item into a platform for recurring revenue.

While headline market growth is steady, heterogeneity across applications and channels matters. The drivers that make the aggregate market attractive — emissions regulation, durability expectations, and rising aftermarket replacement demand — produce uneven opportunities. Additionally, several noise factors warrant explicit mitigation strategies:

Raw-material price volatility: Specialized polymers and synthetic fibers are subject to supply shocks. Procurement teams must plan for dual-sourcing, strategic inventory buffers, and index-linked contracting where feasible.

Labor and capacity constraints: Manufacturing growth is being limited in some regions by skilled labor availability and capex lead times. Strategic capacity expansion requires early commitments and localized automation investments.

Regulatory timing risk: Accelerated emission standards can compress qualification cycles. Companies that have aligned their R&D pipelines to regulatory roadmaps will win OEM design slots; laggards will be relegated to commodity replacement markets.

We recommend executives prioritize the following actions in Q1–Q4 2026 to convert market growth into durable advantage:

De-risk supply chains now: implement layered sourcing, secure long-lead components with multi-year purchase agreements, and run scenario stress tests for raw-material price spikes.

Invest selectively in media technology: allocate R&D capital to media treatments and architectures that deliver measurable improvements in efficiency, pressure drop, and service intervals. Tie R&D milestones to commercialization gates and OEM qualification timelines.

Monetize aftermarket relationships: pilot subscription or sensor-enabled replacement programs with fleet customers and large OMEs to lock-in recurring revenue and capture higher lifetime margins.

Use M&A to buy capabilities, not just scale: target companies with proprietary media, sensor integration experience, or strong regional aftermarket distribution rather than low-margin production assets alone.

Price for value: evolve pricing from cost-plus to value-based models where customers are willing to pay for reduced downtime, lower total cost of ownership, or longer service intervals supported by data.

Our study is built to be actionable: each recommendation is mapped to financial impact, required investments, time-to-value, and implementation risk. Clients receive the underlying demand models and sensitivity tables so they can run “what-if” scenarios tailored to specific OEM contracts, regional exposures, and procurement strategies. Importantly, while this article previews key insights, the full report provides the granular segmentation, channel economics, and company-level metrics necessary to make capital allocation, R&D prioritization, and M&A decisions with confidence.

Decisions taken in 2026 will determine whether companies capture disproportionate returns from a market that is expanding but increasingly selective in rewarding differentiation. Success will come to organizations that combine materials and design leadership with pragmatic supply-chain risk management and go-to-market models that monetize aftersales and services.

If you are evaluating capital allocation, M&A targets, or product roadmaps for the coming fiscal year, PW Consulting’s full Engine Filter Market study provides the detailed segment economics, supplier scorecards, and scenario models required to make those decisions defensible. Contact our research team or visit our website to access the complete dataset, segmentation breakdowns, and premium appendices reserved for subscribers and corporate clients.

For detailed analysis of this topic, please visit the official page:Engine Filter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com