Polyurethane Composites Market: Key Trends and Future Growth Forecast 2025 –2032

Film |

2026-07-03 06:36:22

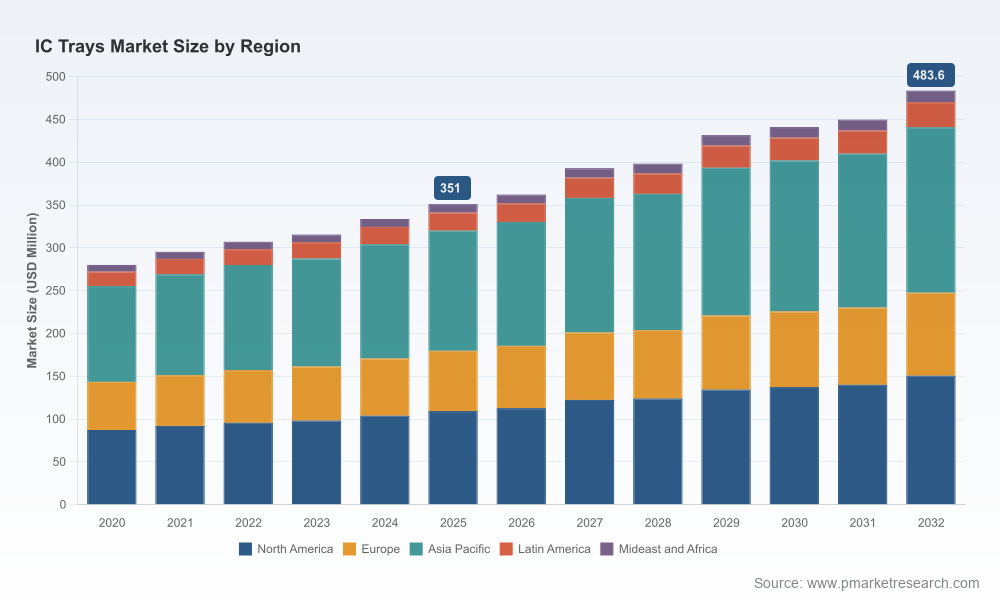

As semiconductor production seeks to reconcile faster innovation cycles with tighter supply chains, the humble IC tray has become a strategic commodity rather than a simple consumable. PW Consulting’s latest IC Trays Market study (base year 2025; forecast period 2026–2032) frames this segment as a steady-growth market with pronounced operational, regulatory, and customer-driven inflection points. By 2025 the market reached approximately USD 351 million and, given the forecast CAGR of 4.9% over 2026–2032, is expected to approach roughly USD 484 million by 2032. These headline numbers matter — they both validate ongoing investments and highlight emerging pockets of value that buyers, producers, and investors must address in 2026.

IC Trays Market

Operational continuity: IC trays are integral to automated handling, test, and shipment workflows. Small disruptions in tray availability ripple across packaging throughput and yield recovery plans.

IC Trays Market

Sustainability and compliance: New production and disposal regulations are elevating material selection and end-of-life strategies from cost items to compliance drivers, affecting total ownership costs for OEMs.

IC Trays Market

Design-for-automation pressures: As assembly and testing automation become universal, tray tolerances, ESD performance, and compatibility with vision/robotic systems are now product differentiators.

The IC trays market expanded steadily through the first half of this decade, moving from a base of about USD 280 million in 2020 to roughly USD 351 million in 2025. This growth reflects a combination of modest unit-demand increases, incremental premiumization (materials and ESD-safe designs), and rising aftermarket/service demand for custom and replacement trays. Looking ahead, the 4.9% CAGR embedded in our forecast reflects a market that is predictable, but sensitive — capable of higher localized growth where semiconductor packaging volumes or re-shoring investments occur, and vulnerable to downturns where tariffs or logistics constraints bite.

Packaging complexity: Shifts toward heterogeneous integration, multi-die packages, and very thin substrates increase demand for specialty trays and custom carriers. Product managers should treat tray spec changes as lead-indicator signals of packaging roadmaps.

Automation compatibility: Buyers are increasingly prioritizing trays that are robot-ready — consistent pocket geometry, dimensional stability, and materials that tolerate high-speed pick-and-place operations. These criteria change supplier selection dynamics.

Material and cost pressures: Volatility in polymer feedstock prices and tighter environmental regulation are driving demand for alternative resins and recycled-content trays, requiring suppliers to innovate without sacrificing ESD and dimensional performance.

Inventory and lead-time optimization: With a market that is fragmented from a supplier standpoint (see below), smart procurement programs balance buffer stock with strategic dual-sourcing to hedge against regional disruptions.

Three interlocking forces shape 2026 decisions: stricter international regulatory frameworks, renewed tariff activity, and continued geopolitical supply chain volatility. Together, these affect raw material sourcing, production footprints, and the economics of importing finished trays. Additionally, evolving regulations on production and disposal are pushing manufacturers to redesign processes and incorporate lifecycle management into pricing models. For operators and buyers, this translates to increased due diligence on supplier compliance, clearer recycling pathways, and scenario-based sourcing strategies in procurement playbooks.

The IC trays market displays moderate fragmentation with a low-to-mid level of concentration among leading suppliers; the top-three and top-five concentration metrics indicate room for regional leaders and niche specialists. Competitive dynamics are driven as much by manufacturing competence as by value-added services — inventory stocking, custom mold development, in-house resin capabilities, and rapid prototyping.

RH Murphy Company, Inc. (Amherst, New Hampshire, USA) — A long-established supplier specializing in JEDEC matrix trays and ESD-safe variants. Their product breadth and emphasis on custom trays for testing and shipment make them a go-to for North American OEMs seeking compliance and rapid turnaround.

Mishima Kosan Co., Ltd. (Kitakyushu, Japan) — Offers vertically integrated capabilities including in-house resin pellet production, mold design, and injection molding with high monthly throughput. Their model reduces lead time risk and creates resilience in resin-constrained environments.

Shinon Corporation (Tokyo, Japan) — A catalog-driven supplier with hundreds of JEDEC tray variants and expertise in substrate cleaning trays. Their breadth suits companies that require reliable off-the-shelf compatibility for legacy packages.

TopLine Corporation (Milledgeville, Georgia, USA) — Focused on stocking and distribution, TopLine acts as a de facto inventory partner for customers needing fast fulfillment of standard JEDEC/EIAJ trays and related components.

Kostat Inc. (Gyeonggi-do, South Korea) — Combines manufacturing with custom design capabilities for carry tapes and cover tapes, appealing to packaging houses integrating carrier tape and tray strategies.

Hwa Shu Enterprise Co., Ltd. (Kaohsiung City, Taiwan) — OEM/ODM-oriented, emphasizing custom mold development and localized production for regional semiconductor manufacturing clusters.

Hiner-pack / Shenzhen Hiner Technology Co., Ltd. (Shenzhen, China) — A manufacturer active in trade shows and market outreach, with JEDEC offerings and custom carrier products for automated handling; participation at major industry events underlines their push into international sourcing channels.

Trade shows and product showcases continue to be important channels for supplier visibility and technology demonstration — for example, a leading Shenzhen-based manufacturer highlighted packaging materials and tray designs at a major Chinese semiconductor exhibition in 2025.

Manufacturers with in-house resin and molding capabilities gained tactical advantages during feedstock volatility, supporting the case for vertical or near-vertical integration in supplier selection criteria.

Customers are moving toward supplier scorecards that weigh sustainability, traceability, and ESD performance alongside price and lead time.

This study is structured to translate market intelligence into executable decisions for 2026. Key components include:

Market sizing and validated growth trajectories (historical and forecast through 2032), with sensitivity scenarios reflecting tariff shocks and reshoring waves.

A supplier heat-map highlighting manufacturing footprints, vertical integration capabilities, and typical lead times — enabling quick shortlist formation for sourcing teams.

Procurement playbook templates: dual-sourcing strategies, contract clauses for material-change mitigation, and inventory sizing models aligned to packaging line KPIs.

Product development checklist for design engineers to ensure trays meet automation, ESD, and recyclability specs without cost overruns.

Regulatory impact matrix and compliance pathways to anticipate cost pressures associated with production and disposal rules in major markets.

Risk scenarios and financial impact summaries: what a 60-day supply disruption could mean for throughput, and mitigation cost-benefit analyses for buffer inventory vs. dual-sourcing.

Adopt a layered sourcing strategy: combine a local stocking partner for critical SKUs with regional manufacturers for agile custom orders. This balances lead-time risk and cost exposure to tariffs or logistics slowdowns.

Prioritize suppliers with material traceability and recycling programs when evaluating total cost of ownership — regulatory changes will translate into direct cost impacts in the near term.

Integrate tray design requirements into packaging and automation roadmaps early. Small dimensional changes in trays can require re-tuning robotic pick-and-place programs and vision systems.

Use procurement contracts to capture innovation: allow for pilot runs and co-development arrangements for specialty trays, while securing pricing collars to reduce feedstock-driven margin volatility.

Monitor supplier concentration metrics and plan for capacity redundancy where single-source risk is material. The market shows meaningful fragmentation; pockets of capacity constraints can emerge quickly.

For teams making sourcing, product, or capital allocation decisions in 2026, the full PW Consulting IC Trays Market report provides the granular analytics and operational templates necessary to convert market signals into defensible, value-accretive actions. Detailed breakdowns by type, application, and region — together with supplier scorecards, model contracts, and scenario simulations — are deliberately presented in the full report to support procurement and engineering workflows. To access the primary tables and proprietary segmentation that underlie the strategic guidance summarized here, please consult the complete study.

For detailed analysis of this topic, please visit the official page:IC Trays Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com