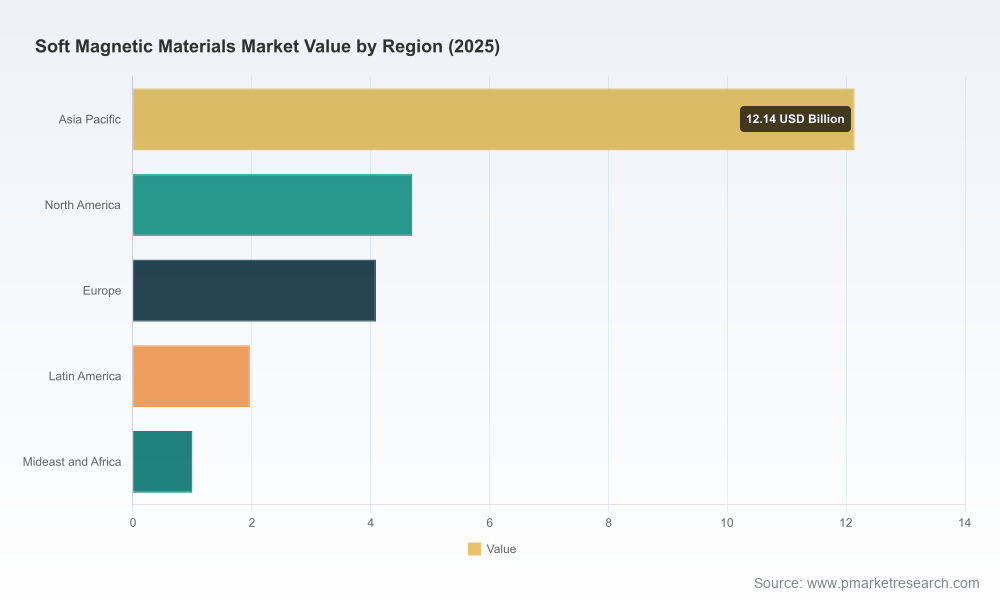

Soft Magnetic Materials Market: Strategic Primer for 2026 Decision-Making

As companies enter 2026, the soft magnetic materials market is no longer a niche engineering concern — it is a strategic battleground for suppliers, OEMs and materials innovators. PW Consulting’s new market study provides a decision-grade lens on this dynamic sector, combining rigorous historical tracing (2020–2025) with forward-looking scenario modeling across the 2026–2032 forecast horizon. Our base-year alignment and transparent growth assumptions show a market that expands from a mid‑twenty billion USD scale in 2025 to an elevated multi‑tens‑billion USD scale by 2032, tracking at a compound annual growth rate of approximately 5.8% through the forecast period. This primer summarizes the research’s practical value to corporate leaders while deliberately preserving the detailed subsegment matrices to encourage access to the full study.

Soft Magnetic Materials Market

Why this study matters for 2026 strategy

- Scale and trajectory shape resource allocation: The reported market trajectory underscores a meaningful expansion window for the next seven years. For executives making 2026 capex, R&D and M&A calls, the difference between tactical hesitation and timely investment will materially affect positioning in electric mobility, renewable energy and power electronics value chains.

- Supply chain pressure points are actionable: Recent macro shocks — trade policy shifts and raw material price moves — create identifiable risk vectors. Our study quantifies these pressures and models hedging outcomes so procurement and operations teams can convert scenario analysis into procurement contracts, localized sourcing and inventory buffers.

- Fragmentation implies differentiated playbooks: Market concentration metrics indicate that dominant scale advantages are present but not overwhelming; opportunities exist for focused technology leaders and regional champions. That profile favors targeted vertical or horizontal strategies rather than a one‑size‑fits‑all global roll‑out.

What PW Consulting’s report delivers (practical contents)

- Proprietary market sizing and forecast engine: A replicable model calibrated to the 2020–2025 historical series and stress‑tested across multiple demand and cost scenarios for 2026–2032. The engine produces topline trajectories and margin sensitivity results that executives can use to test strategic options.

- Scenario playbooks: Up to three alternative futures (baseline, accelerated electrification, and protectionist stress) with discrete triggers and contingency plans. Each scenario includes recommended timing for capital deployment and go/no‑go signals tied to macro, commodity and policy inputs.

- Cost and input‑price analysis: Detailed modeling of feedstock exposure (including silicon and iron ore movements), processing cost dynamics, and downstream pricing power. The study translates raw material volatility into operating margin impacts under realistic procurement strategies.

- Technology and product roadmaps: Comparative assessments of major soft magnetic material families, lifecycle benefits, and trade-offs for applications such as power conversion, motors and magnetics-intensive subsystems. The analysis identifies where premium materials justify price premiums and where incumbent substrates remain cost-effective.

- Supply chain mapping and resilience playbook: End‑to‑end mapping of processing nodes, bottlenecks and strategic chokepoints, plus specific recommendations on capacity flexibility, dual‑sourcing, and nearshoring thresholds tailored for 2026 implementation.

- Strategic M&A and partnership targets: A screened universe of capability gaps, in‑region acquisition targets and partner archetypes, alongside valuation sensitivities and integration risk checklists aligned to different growth scenarios.

- Executive decision dashboards: Condensed, board‑ready visualizations of KPIs and trigger points to accelerate governance decisions during a year when market moves may be rapid.

Market dynamics shaping 2026 choices

Three convergent forces will dictate near‑term competitive outcomes: demand growth driven by electrification and power electronics, input‑cost volatility, and trade/regulatory policy. Our modeling embeds the latest observable events to produce actionable intelligence for 2026.

Soft Magnetic Materials Market

- Demand pull from electrification: Increasing adoption of electric motors, advanced transformers and compact inductive components continues to enlarge the addressable market. The report quantifies how different adoption curves for EVs and renewables convert into incremental material demand and where premium magnetic solutions can capture disproportionate value.

- Raw materials and processing costs: Recent industry data show metal silicon prices and iron ore movements creating real cost pressure for silicon‑steel manufacturing nodes. PW Consulting models how a multi‑percent swing in these inputs propagates through pricing, gross margins and required working capital levels for typical manufacturers and converters.

- Trade policy and regional competitiveness: Policy shifts enacted in 2025 and early 2026 have already altered import economics in key markets. These include expanded tariffs on certain steel imports in some jurisdictions and varying duty regimes across economic blocs. The study quantifies the threshold at which protection measures shift the optimal production footprint and recommends mitigation actions, such as tariff engineering, local finishing capabilities and strategic inventory positioning.

Competitive landscape — who’s shaping the market in 2026

The competitive map blends global steelmakers, specialist alloy developers and components-focused material houses. Market structure metrics show room for both scale plays and niche innovators. The report includes in‑depth company profiles, capability heat maps and strategic option trees for leading players; a few illustrative positions follow.

Soft Magnetic Materials Market

- Specialist material producers: Firms that focus on advanced soft magnetic alloys and precision cores remain critical partners for high‑efficiency motor and sensor OEMs. Their R&D pipelines and IP estates are central to winning electromobility design wins.

- Large steelmakers: Major flat‑rolled steel producers continue to influence volume supply, especially in electrical steels. Investments in processing lines, annealing capability and product optimization for motor cores materially affect market capacity and pricing dynamics.

- Component‑oriented manufacturers: Companies producing powder cores, ferrites and finished inductive components combine materials know‑how with assembly capabilities, shortening OEM qualification cycles and offering differentiation beyond raw material performance.

Recent notable developments that exemplify strategic responses include: a major European steelmaker commissioning expanded annealing and insulating lines at a key site in 2025 to support EV motor demand; a multinational components firm launching an eco‑oriented product family in late 2025 aimed at lowering lifecycle environmental impact; and a North American materials company signing a strategic partnership in early 2026 to strengthen domestic supply chains through rare‑earth domestication. Each move maps to discrete recommendations in the report regarding timing, scale and partnership structures.

Regulatory and commodity headwinds — implications for 2026 action

- Tariff shocks: Expanded tariff measures on certain steel articles implemented in recent policy cycles have immediate implications for landed cost and supplier selection. The study provides a decision framework to determine when local production or strategic warehousing become preferable to spot purchasing.

- Feedstock inflation: Observable increases in silicon and iron ore pricing have already translated into measurable margin squeezes for conversion‑intensive producers. Our sensitivity analysis shows the breakpoints for passing through costs to customers versus restructuring product mixes towards higher‑value alloys.

- Regional duty variability: Differential duties across export markets create arbitrage opportunities but also require sophisticated transfer pricing and logistics planning. The report highlights where regulatory arbitrage is feasible and where it exposes firms to trade remediation risk.

Actionable strategic plays for 2026

- Prioritize dual‑track sourcing: Implement a mix of long‑term offtakes with strategic local partners and short‑term hedged purchases to flatten input volatility without sacrificing responsiveness.

- Accelerate selective localization: Where tariff economics or qualification timelines matter, invest in regional finishing or small modular processing capacity rather than full upstream mills — an approach that preserves flexibility and reduces capex intensity.

- Invest in material differentiation: Allocate targeted R&D to alloy families that deliver demonstrable system‑level benefits (efficiency, thermal management, weight) for EV and power‑conversion applications; these justify premium pricing and lock in OEM roadmaps.

- Use M&A to close capability gaps: Seek bolt‑on acquisitions that accelerate time‑to‑market for advanced powders, nanocrystalline cores or eco‑compliant process technologies; emphasis should be on integration playbooks and customer retention metrics.

- Embed policy triggers into governance: Adopt a small set of quantitative trigger points tied to tariffs and raw material indices that automatically elevate capital or procurement decisions to the board for expedited approval.

Why PW Consulting’s study is the right input for 2026

Our report is structured to be immediately actionable for executives: it blends a rigorous, auditable market model with pragmatic playbooks and a curated landscape of target partners and acquisition candidates. By balancing macro forecasts with granular operational levers and governance triggers, the study gives leaders the confidence to commit capital where it matters in 2026 — while preserving optionality against policy and commodity shocks.

Next steps — where to find the detailed intelligence

This article highlights core directional findings and strategic implications while intentionally withholding the full segmentation matrices, granular regional and application shares, and company‑level revenue breakdowns that many teams will require for operational planning. To access the complete data tables, interactive forecast model, company scorecards and the full set of scenario worksheets — including downloadable KPIs for board reporting — visit the PW Consulting Soft Magnetic Materials Market report page.

For detailed analysis of this topic, please visit the official page:Soft Magnetic Materials Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com