5 Best Sites to Buy verified Revolut Accounts

Gardening |

2026-06-06 14:35:58

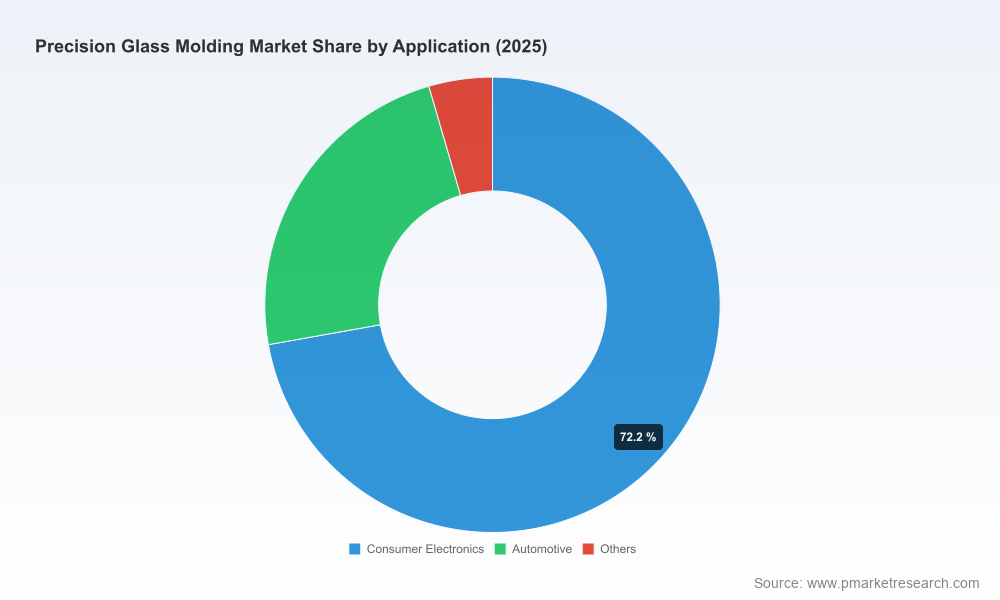

The precision glass molding (PGM) market has evolved from a specialist niche into a strategically important industrial corridor intersecting consumer electronics, automotive sensing, and infrared optics. Our updated market model — with a 2025 base year and a historical window of 2020–2025 — shows the total industry expanding from roughly USD 12.9 billion in 2020 to USD 18.7 billion in 2025, and our forecast through 2032 projects continued momentum to about USD 30.4 billion. That trajectory implies a compound annual growth rate (CAGR) of 7.2% over the 2026–2032 forecast horizon. For executives considering capital allocation, M&A, vertical integration, or new product launches in 2026, these topline dynamics set the frame for choices that should be prioritized now.

Precision Glass Molding Market

Timing capital deployment: With mid-single-digit to low double-digit expansion ahead, firms face a classic build-versus-buy calculus. Our analysis translates the headline CAGR into capacity stress-testing, unit-cost sensitivity, and payback scenarios so leaders can stage investments to capture rising volume without overcommitting to fixed tooling costs.

Precision Glass Molding Market

Materials and supply-chain risk: Raw material costs and geopolitical controls are actively reshaping supply choices — notably in IR optics where germanium restrictions have accelerated interest in chalcogenide glasses. The report synthesizes sourcing contingencies, alternate material qualification paths, and cost impacts to guide 2026 procurement strategies.

Precision Glass Molding Market

Competitive positioning: The market exhibits a concentrated top tier (CR3 and CR5 metrics indicate substantial share concentration). That concentration creates both barrier dynamics and partnership opportunities; our profiles and competitor playbook map out realistic routes to scale through contract manufacturing, licensing of tooling processes, or selective M&A.

Technology inflection points: Breakthroughs such as wafer-scale vitreous carbon molds and advances in moldable IR glasses create new vectors for cost reduction and scale. The report evaluates maturity curves and commercialization windows so R&D and product teams can prioritize investments that will move the cost-performance needle by 2027–2029.

Proprietary market model (base year 2025; historical 2020–2025; forecast 2026–2032) with topline and scenario outputs denominated in USD Million, enabling rapid sensitivity testing against price, volume and material-cost shocks.

Segmentation architecture by region, product type, and application — structured to support go-to-market prioritization. Note: we intentionally keep granular segment tables behind the report paywall to preserve proprietary value, but the executive summary identifies where commercial levers are strongest.

Five strategic use-case playbooks (capacity expansion, contract manufacturing partnerships, vertical integration, materials substitution, and M&A screening) that translate market dynamics into step-by-step actions, KPIs, and escalation triggers.

Competitive landscaping including detailed profiles, capability matrices, and a supplier heatmap highlighting machine builders, captive molders, and specialist chalcogenide producers.

Cost and margin model for precision glass molded optics that decomposes per-unit cost into raw materials, molds/tooling, cycle-time, coatings, and post-processing — designed for finance teams to run scenario-based margin impact studies.

Deal intelligence and recent developments log with dates, capital raises, new product debuts, and technology releases — curated to inform partnership screening and competitive-response timelines.

The competitive landscape is characterized by a mix of vertically integrated specialists, machine manufacturers, and service-oriented players. Each archetype implies different strategic implications for potential entrants and incumbents:

Vertically integrated leaders — Firms that control tooling, preforms, centering and coating can better capture margin and deliver consistent part-to-part performance at high volumes. Their scale advantage is reinforced by recent capital commitments aimed at capacity expansion.

Specialist material players — Companies that qualify new moldable glasses (notably chalcogenide variants) are gaining a foothold in IR and thermal-imaging segments. For companies exposed to germanium supply risk, these suppliers represent a near-term strategic hedge.

Equipment OEMs — High-precision molding machines are an enabler for nearshore production and decentralized manufacturing. Investing in or partnering with machine builders can reduce lead times for tooling and enhance responsiveness to local demand spikes.

Recent industry movements underscore these dynamics. Significant financing rounds into capacity expansion, high-visibility trade show launches of micro-optics portfolios, and academic advances in scalable mold materials all point to an industry entering a commercialization phase where differentiation will be executed through manufacturing depth, materials know-how, and supply-chain control.

Manufacturing cost pressures remain the primary adoption barrier for glass over polymer optics. While glass delivers superior thermal stability and optical performance, its cost profile requires either high-volume deployments or premium applications to justify adoption.

Geopolitical and export-control shifts can create rapid substitution cycles for critical IR materials. These regulatory dynamics should be built into 2026 sourcing and qualification plans, particularly for companies serving defense or security segments.

Tooling and mold longevity are technical gatekeepers. Advances in mold materials and wafer-scale approaches could materially reduce per-unit tooling amortization, creating windows of opportunity for late movers if they can secure early access to the new tech.

Run a focused scenario plan using the report’s market model: stress-test your revenue and margin plans with the baseline 7.2% CAGR and alternative demand shocks to identify the breakpoints where investment in molding capacity becomes accretive.

Pursue strategic partnerships with vertically integrated molders or consider minority investments to secure volume capacity and shorten lead times for critical components.

Accelerate materials qualification programs for chalcogenide and other alternative glass families if you have exposure to IR/thermal applications — build dual-sourcing strategies to mitigate geopolitically driven supply shocks.

Evaluate capex alternatives: compare the economics of incremental machine purchases versus long-term contract manufacturing agreements. The right choice will depend on your volume cadence and your tolerance for fixed-cost leverage.

Establish a technology scouting mandate to monitor wafer-scale mold commercialization and other process breakthroughs — securing early trials or licensing can flip your cost curve within a two- to three-year window.

Prepare an M&A funnel focused on mid-sized specialist molders and materials players. Given industry concentration at the top, selective acquisitions can be an accelerated route to capability ownership and margin capture.

Embed regulatory monitoring in product planning: export controls and material restrictions are high-impact, low-frequency events that should be modeled explicitly into your product roadmaps.

This research is built to move beyond descriptive market sizing. It provides the analytical tooling executives need to translate the 2025 baseline and the 2026–2032 forecast into operational decisions — from procurement and capex sequencing to R&D prioritization and M&A screening. While this briefing outlines the strategic contours, the full report contains the transaction-grade details, competitive scorecards, and an interactive Excel model you will need to execute with confidence.

Download the full study to access the proprietary segmentation tables, company benchmarking matrices, and the downloadable market model that underpins the scenarios summarized here.

Engage our consulting team for a 90-minute executive workshop where we will apply the market model to your portfolio and produce a prioritized action plan with implementation milestones for 2026.

Precision glass molding is at a strategic inflection point. With a clear growth trajectory, concentrated incumbents, and material/technology cross-currents, firms that move in 2026 with disciplined scenario planning and selective capability plays stand to capture disproportionate value as the market scales. For practitioners who need the granular segmentation and executable playbooks that underpin these conclusions, the full PW Consulting report and accompanying data pack are available through our release page.

For detailed analysis of this topic, please visit the official page:Precision Glass Molding Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com