Why Teeth Cleaning in Dubai Is Essential for Everyone

Health |

2026-06-16 11:18:52

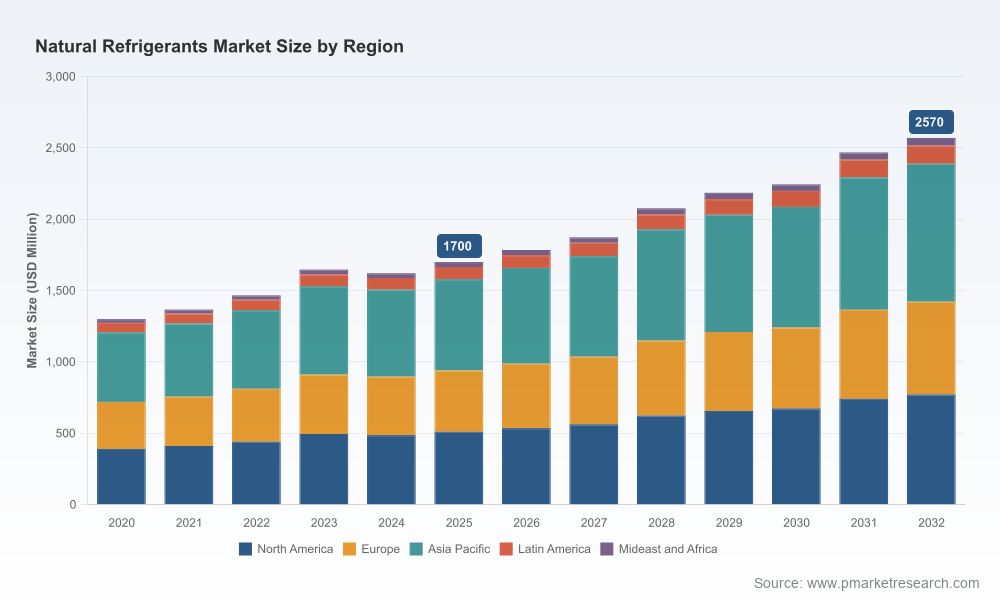

As regulatory pressure, energy transition mandates and cost pressures converge, natural refrigerants are moving from niche to mainstream. PW Consulting’s latest Natural Refrigerants Market study (base year 2025; historical window 2020–2025; forecast period 2026–2032) provides the evidence-based framework that corporate leaders need to make defensible strategic choices for 2026 and beyond. The global market has expanded meaningfully over the past half-decade — rising from a roughly USD 1.3 billion market in 2020 to about USD 1.7 billion in 2025 — and, under our base-case, is forecast to grow at a 6.1% CAGR to reach roughly USD 2.57 billion by 2032. Those headline numbers set the backdrop; the management implications for procurement, product strategy, channel development and M&A are the real story.

Natural Refrigerants Market

Regulation is reshaping demand windows and technical requirements. Recent policy moves — including the EPA’s HFC phasedown rules effective Jan 2025 and new EU F-Gas restrictions that affect certain R‑290 installations — have already compressed timelines for product redevelopment and compliance pathways. At the same time, temporary policy carve-outs and extended no‑action assurances in specific segments create tactical deployment windows that agile firms can monetize.

Natural Refrigerants Market

Technology and product portfolios are evolving rapidly. Suppliers are responding with expanded CO2 and hydrocarbon lineups, integrated component kits, and natural-refrigerant compressors. These product shifts change supply‑chain dependencies, service models and aftermarket revenue opportunity pools.

Natural Refrigerants Market

Commodity and feedstock volatility is now a core strategic risk. The ammonia market hit multi-year highs through 2025 and into 2026 amid feedstock and shipping disruptions — a factor that can decisively change project economics if not actively hedged.

Market growth is steady but not runaway. A ~6.1% CAGR implies meaningful expansion and scale economics for winners, but also sustained competition and the need for disciplined investment prioritization.

Market sizing and scenario models: validated top‑down and bottom‑up estimates (base year 2025) plus three forward scenarios to 2032 that stress-test regulatory, commodity and adoption variables.

Investment-grade go/no‑go frameworks: payback calculators, TCO templates and component cost build-ups designed for integration into capital planning and product roadmaps.

Supplier scorecards and partner maps: comparative assessments of technology capability, manufacturing scale, geographic reach and aftermarket channels for the primary market participants.

Commercial playbooks: channel segmentation, retrofit vs new-install economics, service and training strategies, and pricing guidance for different customer archetypes.

Regulatory and policy impact tracker: timelines, compliance risk matrices and recommended policy engagement priorities per region.

Supply‑chain and raw material risk heatmaps: concentration points, alternative sourcing options and procurement hedging strategies to manage feedstock-driven cost shocks.

Actionable M&A screening and JV templates: targets and integration checklists for companies seeking to accelerate capability-building via inorganic moves.

The competitive picture is neither monopolistic nor atomized: concentration metrics indicate meaningful leaders alongside a long tail of regionally strong suppliers. That mix creates both consolidation opportunities and battlefields for product differentiation.

Linde Group (Ireland) and Airgas (United States) represent large-scale gas and distribution capability — strong in CO2 supply and system-level partnerships. Their scale gives them negotiating leverage and rapid go-to-market for industrial installations.

China-based manufacturers such as Sinochem, Puyang Zhongwei, Juhua and Dongyue combine integrated production with aggressive export strategies. They are important sources of volume and cost competition for commodity refrigerants and mid-tier systems.

Specialist European and Japanese players — Tazzetti, A‑Gas, Secop, Hoshizaki — are executing a different playbook: product engineering depth, component integration and service-driven differentiation. Hoshizaki’s late‑2025 lineup expansion and Secop’s compressor focus are examples of capability-led competition.

Systems and components suppliers such as Sanhua and PRO Refrigeration are moving upstream with integrated packages and purpose-built chillers for CO2 or R‑290, reflecting a shift toward turnkey offerings that shorten customer adoption cycles.

Recyclers and specialty distributors (A‑Gas) and niche OEMs (PRO Refrigeration, Hoshizaki) are positioned to capture aftermarket and retrofit revenue — often higher margin and recurring in nature.

Recent product activity — from PRO Refrigeration’s mid‑2025 CO2 chiller launch to Hoshizaki’s expanded natural‑refrigerant model lineup and Sanhua’s integrated component announcements — underscores two tactical realities: incumbents are accelerating product rollouts, and component standardization is lowering integration barriers for new entrants.

Immediate (0–12 months): Secure feedstock and components. Negotiate multi‑year contracts or strategic supply agreements for ammonia/CO2 components and evaluate financial hedges to protect against price shocks. Build dual‑sourcing where economically feasible.

Near term (6–18 months): Triage product portfolio. Use PW’s TCO and payback templates to identify which SKUs should migrate to natural‑refrigerant platforms now, which require redesign, and which should be sunsetted.

12–24 months: Invest in component integration and service. Prioritize compressor and controller investments, expand certified service networks, and develop retrofit solution bundles to capture early adopters in commercial and industrial segments.

Strategic (18–36 months): Pursue targeted M&A and partnerships. Focus on component specialists, recyclers/distributors and regional manufacturing footprints that reduce time‑to‑market and protect margin.

Ongoing: Build a regulatory playbook. Staff scenario planners to track policy shifts (e.g., evolving F‑Gas rules or EPA guidance) and maintain an advocacy channel to influence standards and safety codes in key markets.

Commodity price volatility — especially ammonia: maintain working capital cushions, hedge strategically and explore collateral feedstock substitutions where suitable system architectures allow.

Regulatory discontinuities: adopt a modular product architecture that allows rapid de‑spec’ing of restricted refrigerants; use retrofit packages to capture customers who need compliance without full system replacement.

Safety and certification friction for hydrocarbon solutions: invest in training and certifications for installers, and collaborate with standards bodies to accelerate adoption pathways.

Competitive pressure from low‑cost exporters: differentiate through integrated services, reliability guarantees and warranty ecosystems rather than competing on commodity price alone.

Use the report as an executable input for three board-level use cases: (1) capital allocation — which product lines to fund and which to harvest; (2) M&A screening — the business cases that justify consolidation; and (3) market entry — the timing and channel mix for new geographies or customer segments. Our scenario models (base case at a 6.1% CAGR) let you stress-test capital plans for conservative, base and accelerated adoption curves through 2032.

This introduction highlights the strategic story and the actionable thinking embedded in the full PW Consulting report. To preserve the commercial utility and integrity of the underlying analysis — and to ensure decision-makers access the complete, source‑level granularity — detailed segment-by-segment tables, region/application/value-chain splits and downloadable financial models are available only in the full report and accompanying data pack. If your decision calendar for 2026 includes CAPEX, sourcing or M&A, the full dataset will materially shorten your execution cycle.

If 2026 is the year your organization must move from planning to implementation, treat this study as a tactical playbook as much as a market forecast. Start with supply‑chain lock‑ins, use payback calculators to prioritize product migrations, and set a two‑year roadmap for service and integration capabilities. PW Consulting’s Natural Refrigerants Market study equips you with the scenarios, vendor insights and operational templates to convert regulatory and technology disruption into sustainable competitive advantage.

For full access to the segment-level datasets, supplier scorecards, modelled scenarios and downloadable tools referenced here, request the complete report and data pack through PW Consulting’s publications portal.

For detailed analysis of this topic, please visit the official page:Natural Refrigerants Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com