SEO Services in Gulberg – Professional Search Engine Optimization Solutions for Business Growth

Other |

2026-07-06 09:58:57

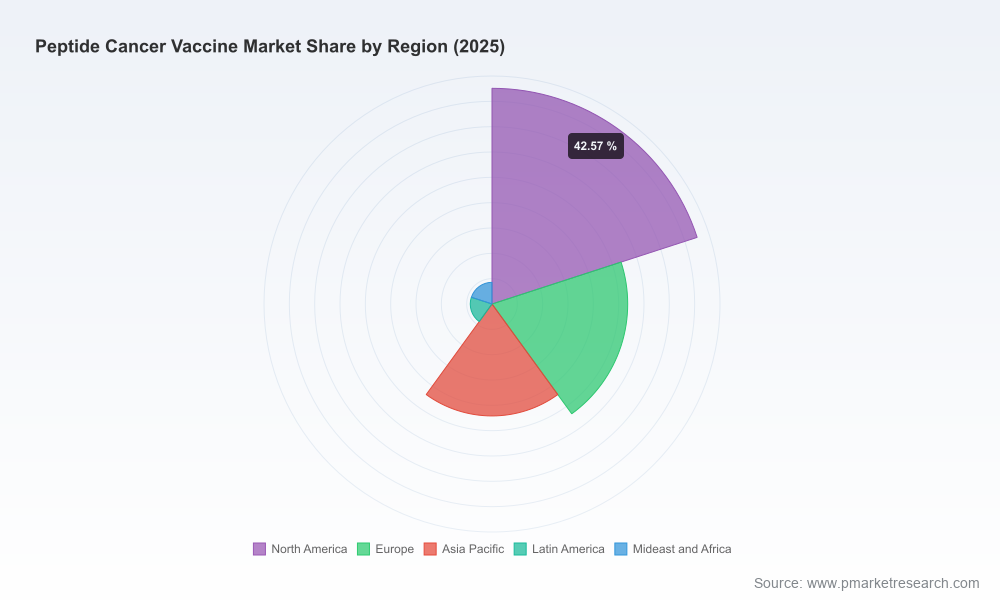

As peptide-based therapeutic vaccines shift from niche science to near-term commercial reality, 2026 will be a hinge year for corporates charting their oncology roadmaps. Our PW Consulting Peptide Cancer Vaccine Market study (base year 2025; historical review 2020–2025; forecast 2026–2032) synthesizes clinical momentum, regulatory dynamics, manufacturing economics and payer risk to convert scientific promise into investable strategy. The market we model reaches roughly USD 169.1 Million in 2025 and expands to an expected USD 263.9 Million by 2032, representing a compounded annual growth rate (CAGR) of 18.5% across the forecast window. This trajectory—together with low incumbent concentration—creates a rare greenfield in oncology where early strategic posture determines long-term leadership.

Peptide Cancer Vaccine Market

Clinical readouts entering registrational windows. Several peptide vaccine programs have produced Phase 2/3 designs or strong Phase 1/2 data through 2025, creating actionable signals for 2026 licensing and partnering decisions.

Peptide Cancer Vaccine Market

Reimbursement and regulatory clarity is emerging. The absence of licensed peptide cancer vaccines in the United States creates a reimbursement gap that payers will be defining in the next 12–24 months—opening a window for early innovators to shape value frameworks.

Peptide Cancer Vaccine Market

Manufacturing and scale economics pivot from feasibility to cost-containment. Peptides offer advantages in stability and relatively low manufacturing toxicity, but scale-up and provider network readiness will determine commercial margin dynamics.

Demand-side drivers: growing emphasis on minimal residual disease and adjuvant settings is pushing interest in therapies that can extend relapse-free survival without heavy systemic toxicity. Peptide vaccines—by design—are positioned to be used in combination and maintenance regimens where safety and incremental benefit matter.

Supply-side advantages and constraints: peptides are cost-effective to manufacture and provide superior stability compared with many biologics, but manufacturing capacity, peptide sequence complexity and batch-to-batch immunogenic consistency remain gating factors for scale.

Regulatory and evidence thresholds: industry data show rising regulatory responsiveness—FDA Phase I approval conversion has improved notably—yet only a minority of candidates historically progress beyond Phase II due to immunogenicity and durability challenges. Sponsors must therefore prioritize translational biomarkers and adaptive designs.

Market structure: the competitive landscape is fragmented. A low three- and five-firm concentration reveals an open competitive field where first-mover clinical validation or a strong partnership can rapidly change positioning.

The market is being written by innovators pursuing distinct peptide strategies—lymph node-targeted amphiphiles, multi-peptide “off-the-shelf” constructs, personalized neoantigen sets and dendritic cell–pulsed approaches. Recent clinical developments through 2025 provide the highest-confidence signals for 2026 strategy:

Elicio Therapeutics (Boston) has reported durable survival and robust mKRAS-specific T cell responses across updated Phase 1/2 programs, establishing a clinical precedent for targeted amphiphile approaches in minimal residual disease and stimulating partnership interest for combination regimens.

OSE Immunotherapeutics (Paris) advanced its multi-peptide candidate with positive Phase 2 results in a maintenance setting and publicized Phase 3 trial design in NSCLC, signaling commercial readiness pathways for multi-peptide platforms where comparator-controlled outcomes are achievable.

TapImmune and OncoPep represent complementary approaches targeting tumor-associated antigens and multi-peptide constructs with specific indications (e.g., HER2, smoldering myeloma) that highlight the diversity of clinical entry points for peptide vaccines.

Strategic implication: robust Phase 2/3 signals materially de-risk partnering conversations and valuation benchmarks. For corporate development teams, 2026 is prime for optioning assets with clear biomarker-driven stratification or for co-developing combination regimens where peptide vaccines enhance checkpoint inhibitor durability.

Value proposition and pricing: absent precedent pricing paradigms for marketed peptide cancer vaccines, early sponsors must assemble HTA-grade dossiers focused on relapse prevention, quality-adjusted survival gains, and real-world cost-offsets from reduced downstream therapy utilization.

Payer engagement: because there are currently no U.S.-licensed peptide cancer vaccines, payers will be influential in framing eligible populations. Proactive, joint evidence-generation pilots with payers and network providers will accelerate access decisions.

Distribution and administration models: the clinical positioning (maintenance vs. combination vs. neo-adjuvant) dictates channel and administration infrastructure. Peptide stability eases cold-chain constraints, but site-of-care and provider education remain operational priorities.

Manufacturing partners and supply security: companies should lock capacity through CDMO relationships or build modular peptide suites capable of rapid sequence swaps to support personalized workflows and multi-peptide panels.

Our full study is designed as an executable guide for boards, M&A teams, product strategy leaders and investors. Key practical deliverables include:

Granular market sizing and a 2026–2032 forecast model with scenario toggles for indication prioritization and reimbursement outcomes.

Clinical pipeline tracker with milestone calendars, comparator evidence matrices and probability-adjusted success models keyed to immunogenicity endpoints.

Commercial due-diligence playbooks: payer value-dossier templates, HTA submission roadmaps, launch sequencing recommendations and pricing-sensitivity analyses.

Manufacturing and supply chain assessment: CDMO capability maps, cost-per-dose modeling and regulatory compliance checklists.

Deal landscape and partnering heatmap: acquisition, co-development and licensing scenarios with expected valuation bands under multiple clinical outcomes.

Risk register and mitigation playbook addressing regulatory attrition, immunogenicity shortfalls, reimbursement delays and competitive displacement.

For biotech sponsors: prioritize a bifurcated evidence strategy—pursue fast, randomized maintenance/neo-adjuvant trials to generate clinically meaningful endpoints while running adaptive biomarker-enriched studies to optimize patient selection.

For large pharma: pursue bolt-on acquisitions or strategic alliances to enter the peptide vaccine space with minimal time-to-market, placing a high premium on assets with Phase 2+ validation or clear combination synergies with existing portfolios.

For CDMOs and suppliers: invest in modular peptide manufacturing lines and flexible GMP capacity; offer integrated analytics and peptide sequence QC services to capture upstream value.

For investors: focus diligence on clinical proof-of-concept data that demonstrates durable immunologic endpoints and on management teams with a pathway to payer engagement that starts in parallel with late-stage trials.

Decisions in 2026—whether to partner, to build manufacturing, to pivot a pipeline or to bid on an asset—require a synthesis of clinical probability, payer dynamics and commercial execution risk. Our market model and playbooks convert these variables into actionable levers: build vs. buy timelines, evidence-gathering priorities, go-to-market sequencing and downside protection structures. Importantly, the report preserves scenario-level flexibility by mapping forecasts to multiple reimbursement and clinical success scenarios so that boards can stress-test capital allocation under plausible futures.

Peptide cancer vaccines present a strategic window where relatively modest investments in clinical validation and manufacturing readiness can create outsized commercial optionality. The market is growing at a high double-digit rate, and the competitive field remains open. For organizations that move decisively in 2026—prioritizing robust evidence generation, payer engagement and modular manufacturing—the next three years will determine whether they capture a leadership role in a new class of oncology therapies.

PW Consulting’s full Peptide Cancer Vaccine Market report contains the detailed segment-level forecasts, company profiles, valuation scenarios and go-to-market templates necessary for operationalizing these strategic conclusions. For the complete dataset, interactive models and tailored advisory support to inform 2026 decisions, please consult our full report and contact our team through the source webpage.

For detailed analysis of this topic, please visit the official page:Peptide Cancer Vaccine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com