Vinyl Ester Resins Market — Strategic Preview for 2026 Decision-Making

As companies position for growth in the composite materials space, PW Consulting’s latest market study on Vinyl Ester Resins delivers the strategic intelligence required to convert market signals into executable decisions in 2026. This preview highlights the study’s macro trajectory, the material dynamics shaping supplier economics, and the competitive maneuvers that will matter most to management teams, while intentionally withholding detailed sub-segment tables to encourage full-report engagement.

Vinyl Ester Resins Market

Market trajectory at a glance

Our analysis — built on a 2020–2025 historical baseline and a 2026–2032 forecast horizon — shows a resilient and steadily expanding vinyl ester resins market. Measured in USD Million, the industry expanded from under USD 1 billion in 2020 to roughly USD 1.23 billion in the base year 2025, reflecting recovery and selective demand growth across corrosion-resistant, marine, and wind-energy composites. Going into the 2026 forecast year, the market is projected to continue growing, underpinned by an aggregate CAGR of approximately 5.27% across the forecast window. By 2032, our scenario-led forecasts point to a materially larger market, underscoring both structural demand drivers and opportunities for premiumization.

Vinyl Ester Resins Market

Why this study matters for 2026 strategic planning

- Capital allocation: The forecast horizon and scenario analysis help CFOs and strategy teams prioritize CAPEX for capacity expansion, retrofit investments to support higher-reactivity chemistries, or targeted M&A to densify portfolios in corrosion- and marine-focused segments.

- Product and portfolio strategy: With product innovation shifting toward higher-performance epoxy-novolac and bio-derived resin lines, R&D and product management must balance near-term margin preservation against longer-term differentiation opportunities.

- Commercial and pricing playbooks: The report decodes recent pricing volatility drivers and offers contract-structure guidance — including hedging and indexation approaches — that purchasing and commercial teams can adopt in 2026 to protect margins without sacrificing market share.

- Supply-chain resilience: Raw material concentration, freight volatility, and regional logistics asymmetries mean procurement leaders need scenario-based supplier scorecards; the study provides these as operational tools.

What the full report delivers — practical, transaction-ready content

This is not a high-level brochure. Our full study is designed for immediate operational use by business units, corporate development teams, and investor committees. Deliverables include:

Vinyl Ester Resins Market

- Validated market-sizing (historical and forecast) with scenario overlays and sensitivity to raw-material price scenarios.

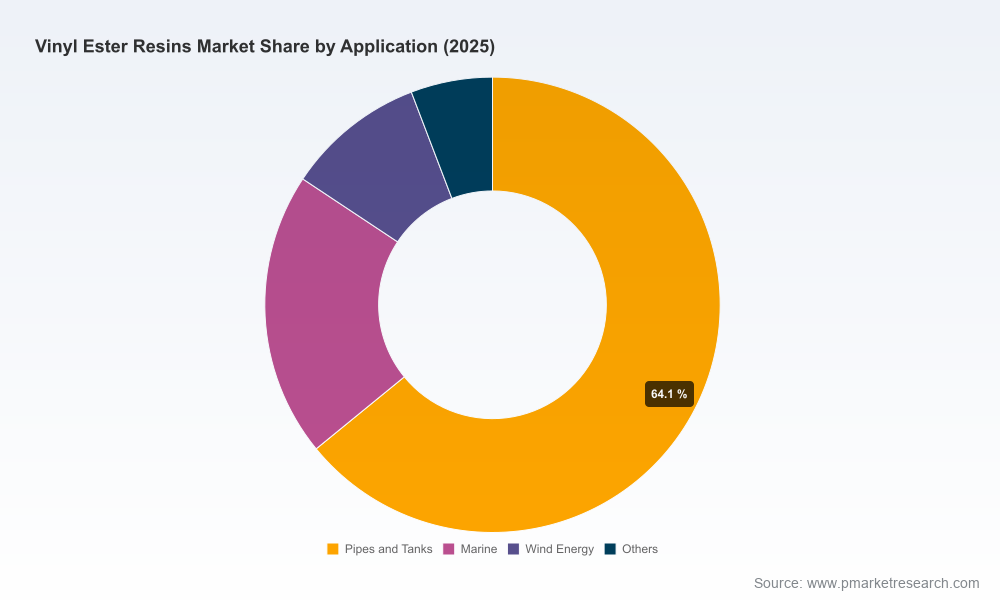

- Demand-driver matrices that map end-market exposures (e.g., marine, pipes & tanks, wind energy, industrial) to specific resin attributes and margin implications.

- Cost-and-margin modelling templates with inputs for monomer, styrene, and epoxide cost drivers; users can toggle assumptions to project impact on list and net prices.

- Go-to-market playbooks for OEM partnerships, value-added service bundling (e.g., preforms, infused laminates), and distribution strategies tailored by channel economics.

- A short-list of inorganic targets and deal comparables, with accretion/dilution and integration-readiness assessments for rapid diligence.

- Commercial clauses and procurement negotiation blueprints suited to 12–36 month contracting cycles in a moderately concentrated market.

Market dynamics that will shape 2026 outcomes

Several near-term dynamics have outsized strategic consequences for 2026 plans:

- Raw material volatility: The sector experienced pronounced input-cost shocks in 2024 when styrene and epoxide monomers spiked, prompting list price increases across formulations. While Q4 2025 saw easing in vinyl ester prices tied to softer acrylic acid costs and tempering coatings demand, the underlying supply tightness for certain intermediates remains a source of downside margin risk.

- Unit price levels and contracting norms: Market pricing reached elevated levels during the 2024–2025 cycle in some regions, necessitating more sophisticated contracting mechanisms (indexation, take-or-pay, and escalation clauses) to align supplier and buyer incentives through 2026.

- Sustainability and product innovation: Leading manufacturers are commercializing bio-derived and high-reactivity epoxy-novolac grades. For example, new product introductions that combine higher renewable/biogenic carbon content with improved reactivity alter the TAM for “value” versus “performance” resins and affect OEM sourcing specifications.

- Moderate concentration: The market exhibits mid-tier concentration dynamics — with the top three and five firms accounting for meaningful, but not dominant, shares. This creates space for regional specialists and technical innovators to secure premium niches while leaving open consolidation paths for scale players.

Competitive landscape — who to watch

Our competitive assessment combines public disclosures, product portfolios, and go-to-market footprints to identify frontrunners and fast-followers:

- Polynt S.p.A. (Italy): A global supplier with depth in marine and corrosion-resistant composites. Polynt’s approach emphasizes standard lamination and infusion-ready chemistries for high-performance applications.

- Resonac Holdings Corporation (Japan): Markets epoxy vinyl ester grades that blend epoxy durability with unsaturated polyester processing characteristics — a favorable proposition where thermoset performance needs to meet existing manufacturing methods.

- RealLand Composite Material Technology Co., Ltd. (China): Focused on industrial corrosion protection, RealLand brings a regional cost-competitive position and a growing export footprint.

- FGCI (United States): A supplier oriented to fiberglass and polyester markets with strong ties to hand lay-up and boat-building customers; well-positioned in localized channels that value service and rapid delivery.

- Interplastic Corporation (United States): Offers branded CoREZYN® lines targeted at chemical, marine, and structural applications, with emphasis on product consistency and technical support.

- Scott Bader Company Ltd. (United Kingdom): Leverages longstanding reputation in specialty resins, emphasizing industrial and marine corrosion resistance in premium applications.

- Union Composites Changzhou and Changzhou Rule Composite (China): Regional players focused on export and domestic markets, with competitive propositions on standard and specialty vinyl ester chemistries.

Recent industry moves underscore strategic themes: product-grade innovations and sustainability positioning are accelerating. For example, SIR Industriale’s launches in 2025 — a high-reactivity epoxy-novolac grade and a BIOSIRCLE® line with elevated renewable carbon content — illustrate how suppliers are advancing both performance and ESG narratives simultaneously. Such developments shift OEM sourcing criteria and create opportunities for early adopters to differentiate.

Implications for corporate strategy and commercial execution in 2026

- M&A and partnerships: Expect deal activity focused on technical capabilities (novolac and epoxy integration), regional distribution access, and firms with established OEM approvals. Buyers should prioritize targets with clean regulatory records and scalable production processes.

- R&D and product roadmaps: Invest to shorten development cycles for biogenic-content and high-reactivity chemistries that reduce cure time, improve corrosion resistance, or enable lower styrene emissions — all of which command premium pricing in informed buyer segments.

- Procurement playbook: Build multi-scenario sourcing strategies that combine strategic hedges for monomers, diversified supplier panels, and flexible contract clauses to protect margin in the face of input spikes.

- Commercial differentiation: Move beyond commodity pricing by embedding technical services (lamination support, formulation lockers, certification assistance) to secure longer-term OEM relationships.

- Operational readiness: For manufacturers, ensure manufacturing assets are capable of handling higher-reactivity and lower-styrene formulations, and invest in emissions and waste controls to satisfy rising regulatory and customer requirements.

Data integrity, concentration and what’s intentionally withheld here

The market sizing and growth rates cited above are based on revenue denominated in USD Million using 2025 as the base year and a forecast window through 2032. The study also quantifies market concentration metrics to inform competitive strategy: the top three and top five firm aggregates indicate a moderately concentrated marketplace, creating both competitive pressure and M&A runway for scale-driven players.

To preserve the report’s commercial value as a decision-making asset, this preview omits granular sub-segmentation tables (regional breakdowns, application-level percentage shares, and specific per-type volumes). These details are provided in the full report, where interactive tables and downloadable modelling templates allow executives to tailor scenarios to corporate specifics.

Next steps for 2026 planners

Leaders preparing 2026 budgets should treat the vinyl ester resin market as one offering stable mid-single-digit growth but elevated dispersion across end-markets and product tiers. Use our study to:

- Stress-test capital and procurement plans under upside and downside raw-material scenarios;

- Identify inorganic targets or partnership candidates with complementary technical capabilities; and

- Refine product roadmaps to capture premium pricing for sustainable and high-performance grades.

For teams ready to convert insight into action, the full PW Consulting report contains the operational models, commercial templates, and competitive dossiers necessary to accelerate decision cycles in 2026. Access to the full dataset and supporting deliverables will enable targeted, measurable moves — whether the priority is margin resilience, growth capture, or consolidation playbooks.

For detailed analysis of this topic, please visit the official page:Vinyl Ester Resins Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com