PW Consulting: Digital Scent Tech Market Poised for 9.8% CAGR to USD 305.8M by 2032

Technology |

2026-07-12 04:12:25

As PW Consulting’s Senior Strategic Advisor and Head of Industry Analysis, I present an executive introduction to our Microgrid Market research — a practitioner-focused intelligence product designed to inform capital allocation, procurement strategy, and operational readiness through 2026 and beyond. The market has reached a pivotal inflection: with a 2025 base of USD 27,000 Million (revenue unit: Million, currency: USD) and a robust compounded annual growth rate of 17.5% across our 2026–2032 forecast window, microgrids are moving from niche resilience projects to mainstream distributed-energy infrastructure. This note previews the study’s strategic value for 2026 decision cycles, highlights the dynamics shaping supplier and investor choice, and outlines the practical tools included in the full report. In keeping with the “trailer” principle, we demonstrate analytical depth while intentionally withholding proprietary sub-segment tables and granular regional allocations — those are available in the full deliverable.

Microgrid Market

Transition from pilot to program scale: The industry’s trajectory — from roughly half the scale in 2020 to a USD 27,000 Million market in 2025 — signals that microgrids are moving beyond isolated pilots into multi-project deployment portfolios. Forecasts show continued acceleration, with the market climbing meaningfully by 2026 and trending toward substantially larger scale by 2032. Executives must therefore pivot from one-off procurement to platform and lifecycle strategies.

Microgrid Market

Regulatory and funding inflection points: 2024–2026 regulatory activity embeds distributed energy resources into grid code modernization, accelerating interconnection and demand-side controls. Public incentives and state-level programs — including targeted microgrid initiatives and utility incentive funds — materially lower first-cost barriers for sponsored deployments, while national buy-local rules for energy storage components create procurement and supply-chain constraints decision-makers must plan for.

Microgrid Market

Technology economics are bifurcating choices: Installed BESS costs for commercial lithium-ion systems continue to exhibit wide ranges by site complexity and region. Meanwhile, alternative chemistries and long-duration storage entrants are maturing, forcing a reassessment of life-cycle cost assumptions and maintenance planning for multiyear contracts.

Concentration and competitive dynamics: The vendor landscape is moderately consolidated at the top but remains open for niche specialists and vertically integrated suppliers. Market concentration metrics indicate that leading suppliers capture a meaningful share without forming a closed oligopoly — a structure that favors both large systems integrators and agile innovators.

Our Microgrid Market study is designed as a working playbook for 2026 decision-makers. The full report contains:

Transparent market sizing and forecast methodology (base year 2025; forecast 2026–2032) with scenario and sensitivity engines to stress-test price, incentive and adoption assumptions.

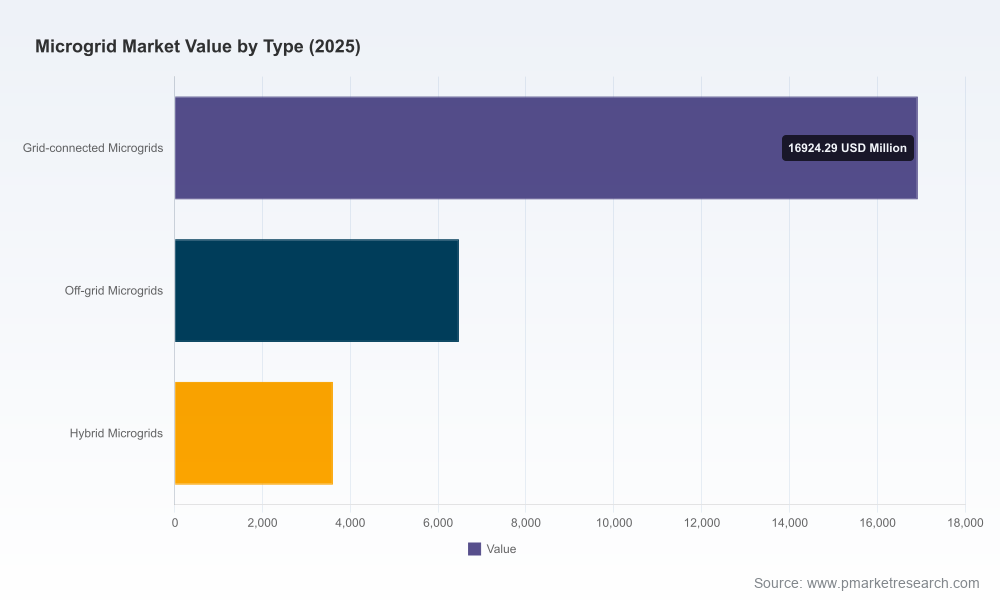

Practical procurement templates: RFx checklists, specification suites for grid-connected, off-grid and hybrid architectures, and supplier evaluation scorecards.

Vendor landscaping and strategic positioning: qualitative profiles and comparative assessment of integrators, OEMs, storage specialists, and software/control platforms.

Implementation playbooks and O&M models: CAPEX/OPEX templates, lifecycle costing, warranty/guarantee terms negotiation points, and TCO comparators by use case.

Regulation & incentive tracker: an up-to-date dossier of federal, state, and utility programs that affect project viability and procurement requirements.

Deal structuring guidance: commercial models (PPA, shared-savings, lease, capex), financing mosaics, and investor due-diligence checklists.

Case studies and lessons learned: repeatable deployment archetypes with risk logs and mitigation pathways for common failure modes.

The market’s historical acceleration (rapid expansion between 2020 and 2025) validates several strategic imperatives: mobilize procurement frameworks now; create modular standards across enterprise sites; and prioritize software-driven orchestration to maximize asset utilization. Our base-year calibration incorporates observed installations and contract flows up to 2025 and projects steady market expansion into 2026 and beyond, culminating in a materially larger addressable market by 2032. With a forecast CAGR of 17.5% across our horizon, near-term decisions — supplier selection, chemistry choices, and compliance with domestic-content rules — will have outsized effects on multi-year economics.

Key dynamics informing these outcomes:

Policy sponsorship and utility incentives accelerate adoption in sponsored geographies; tailored incentive programs materially tilt economics at the project level but require alignment with procurement timelines to capture funds.

Supply-chain and regulatory constraints (including domestic preference rules for storage components) create both risk and opportunity: onshoring or qualifying suppliers early reduces allocation risk, but may increase near-term costs.

Cost dispersion across sites and battery chemistries means blanket assumptions are hazardous. Project-level installed battery costs can vary significantly depending on scope and complexity — a fact our sensitivity models capture.

The ecosystem is composed of strategic integrators, modular OEMs, storage chemistry specialists, and software/control pure-plays. Understanding each group’s strengths and constraints is essential to structuring risk-aligned partnerships:

Platform integrators (examples include multinational energy-electrical conglomerates) bring breadth: hardware, software, and service portfolios that simplify single-vendor accountability for large commercial, industrial and utility programs. Their advantage is end-to-end delivery and proven project execution, but enterprises must assess unit economics and implementation lead times.

Modular OEMs and rapid-deployment specialists emphasize prefabricated, containerized systems and fast field installations. These players are attractive for time-constrained deployments and disaster-resilience hubs where speed-to-service trumps absolute cost.

Storage and chemistry innovators (including zinc-based and fuel-cell suppliers) are shifting the value equation on duration and cycling economics. For organizations requiring long-duration or non-lithium solutions, these suppliers present differentiated risk-return profiles.

Controls and optimization software companies offer the intelligence layer that unlocks grid services, resilience value, and asset optimization. Integration readiness, API openness, and cyber-resilience capabilities are critical selection criteria.

Recent market moves reinforce these themes and provide forward-looking signals:

Scale transactions and strategic repeat orders from storage specialists underline the growth of commercial microgrids and the importance of supply continuity.

Large deals involving battery capacity illustrate aggregators’ and developer’s emphasis on grid delivery and reliability as monetizable outcomes.

Partnerships between heavy-equipment OEMs and energy developers show a growing convergence between traditional power generation and modern hybrid microgrid offerings, particularly for high-reliability customers such as data centers.

Public-sector initiatives and award-winning community projects highlight the twin tracks of resilience planning and community-scale adoption that will define procurement pipelines in many jurisdictions.

Run a rapid portfolio screen: triage assets/sites by resilience need, load profile, and interconnection complexity to prioritize pilot-to-scale rollouts.

Lock in procurement guardrails: include domestic-content compliance verification, battery chemistry requirements, and service-level KPIs in bid documents.

Establish supplier conditionality: require delivery timelines tied to incentive capture windows and include performance bonds for critical-path components.

Deploy a two-track pilot strategy: a fast, modular pilot to validate controls and an integrated commercial pilot to validate lifecycle economics and financing.

Integrate regulatory and incentive monitoring into procurement governance to ensure timely application for utility or state programs that materially affect project IRR.

We combine a transparent, reproducible forecasting engine (base year 2025; forecast period 2026–2032) with on-the-ground validation. Our deliverables include an interactive financial model, vendor scorecards, procurement templates and an implementation playbook — not just static analysis. We stress-test outcomes under alternate regulatory and technology-cost pathways so that corporate strategy, asset managers and procurement leads can run “what-if” scenarios and arrive at defensible decisions for 2026 capital cycles.

While this preview outlines the strategic contours and core imperatives, the full report contains the granular segmentation, vendor benchmarking matrices, and downloadable financial models that enterprise teams require to operationalize decisions. Those assets are intentionally gated to preserve the actionable value of our primary research.

For teams preparing 2026 budgets, procurement cycles or M&A pipelines, this study provides the framework and tools to move from intention to execution with clarity and defensible assumptions. To access the full segmentation, proprietary models and our supplier due-diligence pack, visit the PW Consulting Microgrid Market page or contact our advisory team for a briefing and custom scenario run tailored to your portfolio needs.

For detailed analysis of this topic, please visit the official page:Microgrid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com