XPLR Guide to Discovering Hidden Places in Your City

Shopping |

2026-04-28 18:45:08

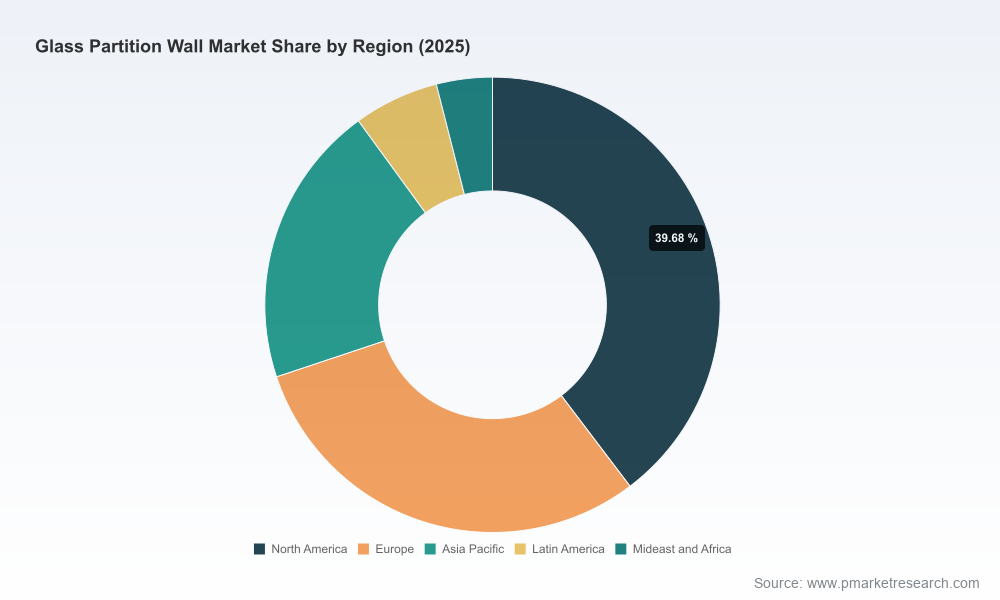

The global glass partition wall market has entered a phase of consolidated, innovation-driven growth. Our PW Consulting baseline shows the market expanding from an estimated USD 950 million in 2020 to USD 1,150 million in the base year 2025, with a projected compound annual growth rate (CAGR) of 6.5% over the 2026–2032 forecast window. By the mid-point of the forecast the market is expected to pass the USD 1.6 billion mark, with modeled upside tied to accelerated commercial fit-out cycles and modular construction adoption. Market concentration remains material: the top-three suppliers account for roughly half of industry revenues, while the top five approach a strong majority—an important signal for competitive and M&A strategies in 2026.

Glass Partition Wall Market

This introduction synthesizes the strategic value of the full Glass Partition Wall Market study for corporate planning in 2026. It highlights the macro trajectory, the regulatory and supply-side inflection points, competitive positioning themes and operational levers that will matter most to manufacturers, specifiers, real estate owners and investors.

Glass Partition Wall Market

In keeping with the “trailer” principle that governs our public briefs, we intentionally present directional, data-driven conclusions while withholding granular sub-segment revenue splits and exclusive tables found in the full report. Those detailed breakouts—essential for transaction due diligence, market entry scoping and SKU-level pricing strategy—are available in the full publication.

Glass Partition Wall Market

Consistent expansion with selective acceleration — The market’s 6.5% CAGR reflects steady demand for glass partition solutions driven by office refurbishments, institutional retrofits and rising preference for transparency and light in commercial interiors. This macro growth masks asymmetries across geographies and applications—creating both hotspots of high-margin opportunity and areas of intense price competition.

Consolidation opportunity amid concentrated supply — With the three largest players commanding a clear lead and the five largest controlling a dominant share, mid-market vendors face a choice: specialize, vertically integrate, or pursue M&A to scale engineering, distribution and installation capability. For acquirers, the market concentration presents attractive roll-up economics if integration can deliver standardized manufacturing and installation protocols.

Raw material and input volatility — Input signals matter. In 2025 soda ash prices eased due to oversupply and weaker demand across some glass-using industries, and domestic production ticked upward. These movements reduce near-term cost pressure for float-glass-based systems, but the supply chain retains exposure to energy, logistics and regional tariff shifts that can rapidly change installed costs.

Regulatory and performance specifications as market gatekeepers — Specification standards relevant to partitions (including ASTM-level glass flatness, tempering and airborne sound transmission standards, and new guidance on mounting and fire-reaction testing such as EN 18080:2025) are elevating the technical bar. Vendors that embed certified acoustic and fire performance into product families will have an advantage in winning institutional and high-spec commercial projects.

Product innovation and service differentiation — The fastest-growing value pools are occupied by suppliers who bundle modularity, rapid on-site installation, lifecycle service, and sustainability credentials. Demand for movable and folding wall systems, slimline sliding doors and demountable solutions underscores a buyer preference for flexible space strategies that reduce tenant downtime.

The competitive field combines regional champions, premium European players, nimble North American integrators and high-volume factory-direct suppliers. Key archetypes include:

Systems integrators and design-led suppliers: Companies with end-to-end capabilities—design, engineering, manufacture and installation—tend to win complex commercial and institutional work where specification control, warranty and single-source accountability are decisive. These firms compete on speed-to-site, custom engineering and tight project management.

Modular and movable specialists: Producers of operable, folding and movable glass wall systems are capturing budgets tied to flexible workplace strategies. Product launches that improve sealing, acoustic performance and slim sightlines are differentiators.

Factory-direct, cost-leaders: High-capacity manufacturers that sell through distribution or direct supply chains can undercut on price in commoditized segments (e.g., standard full-height partitions) while competing on lead times for volume projects.

Premium and sustainability-focused brands: European and specialist manufacturers that emphasize sustainability certifications, ISO-aligned production and bespoke finishes are positioned to capture high-end corporate and institutional projects where lifecycle cost and corporate ESG commitments influence procurement.

Representative company examples mapped to these archetypes include established U.S.-based systems integrators that emphasize rapid custom solutions, makers of movable and folding wall systems, premium UK and German manufacturers focusing on sustainable production and finishing, and Chinese factory-direct suppliers providing fully customized full-height systems at scale. Notable recent market activity includes a January 2026 product launch of a new slimline sliding door and demountable series by a U.S. systems supplier, and continued trade show engagement across key markets—signals of product refresh and go-to-market acceleration heading into 2026.

Prioritize spec-compliance and test-proofing: Incorporate ASTM and EN-compliant performance data into marketing and bid packs. Early investment in certified acoustic and fire test reports shortens procurement cycles for institutional buyers and reduces bid-stage risk.

Hedge supply exposure and secure capacity: With raw-material tremors still possible, secure multi-sourced agreements for key inputs, consider strategic inventory buffers for high-volume SKUs, and explore vertical integration or preferred supplier arrangements for glass and framing components.

Differentiate through modularity and after-sales services: Expand demountable, reconfigurable product lines and back them with refurbishment and asset-tracking services—these create recurring revenue and increase customer switching costs.

Focus M&A on engineering, finishing and installation capability: For buyers seeking scale, acquisitions that add national installation networks or specialized engineering IP deliver immediate margin uplift and accelerate entry into high-spec projects.

Invest in digital tendering and visualization tools: Configurators, BIM-ready product libraries and rapid estimation tools materially shorten procurement cycles and increase win rates for specification-driven projects.

Align product roadmap to sustainability and lifecycle cost narratives: Highlight recycled-content glass options, low-VOC framing and cradle-to-gate assessments to capture buyers with strong ESG procurement frameworks.

The full PW Consulting study is built as an operational toolkit for 2026 decision-making. It includes:

Market sizing and CAGR-based forecasts with scenario modelling across 2026–2032 (base year 2025; historical series 2020–2025).

Segmented demand analysis by product architecture, application and region—presented with entry thresholds and margin benchmarks (note: detailed sub-segment tables are available in the full report only).

Comprehensive supplier landscaping with capability maps, pricing heuristics, lead-time benchmarks and categorized M&A targets.

Supply-chain risk assessment spotlighting raw-material trends, logistics pinch-points and supplier concentration risk.

Regulatory and testing compendium that consolidates relevant ASTM, EN and acoustic/fire performance requirements—actionable for procurement and product development teams.

Go-to-market playbooks for OEMs, distributors and installers covering channel design, specification engagement, tender tactics and digital productization.

Case studies and proforma financials for representative project types to stress-test investment theses and pricing strategies.

Executive teams and business-unit leaders should use the report to: align capital expenditure with the forecasted revenue trajectory; prioritize product lines that meet tightened acoustic and fire requirements; and identify acquisition targets or partnerships that close capability gaps in installation and modular manufacturing. Project teams will find the tendering playbooks and specification compendium directly actionable for immediate bid wins.

With a clear macro growth runway and non-trivial market concentration, 2026 represents a pivotal window for companies to re-define competitive advantage in the glass partition wall market. The combination of evolving standards, raw material cycles and shifting buyer preferences means tactical moves this year—on product certification, factory capacity and channel design—will disproportionately shape market share outcomes over the next business cycle.

For a complete set of proprietary sub-segment tables, supplier scorecards, project-level cost models and the full methodology, access the PW Consulting Glass Partition Wall Market report. The full dataset is required to convert the directional strategies summarized here into executable plans and transactional intelligence.

For detailed analysis of this topic, please visit the official page:Glass Partition Wall Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com