Polysilicon Market: Strategies for Sustainable Growth in a Changing Market, Forecast by 2033

Other |

2026-03-11 10:21:21

As PW Consulting’s lead industry analyst, I present a compact, high-signal preview of our flagship Nanocellulose Market research — crafted to guide executive decisions through 2026 and beyond. This preview demonstrates the analytical rigor and practical orientation of the full study while intentionally withholding detailed segment tables and regional splits. Our aim is to build confidence in the study’s methodology and strategic value, and to invite stakeholders to access the full report for the underlying granular datasets and actionable models.

Nanocellulose Market

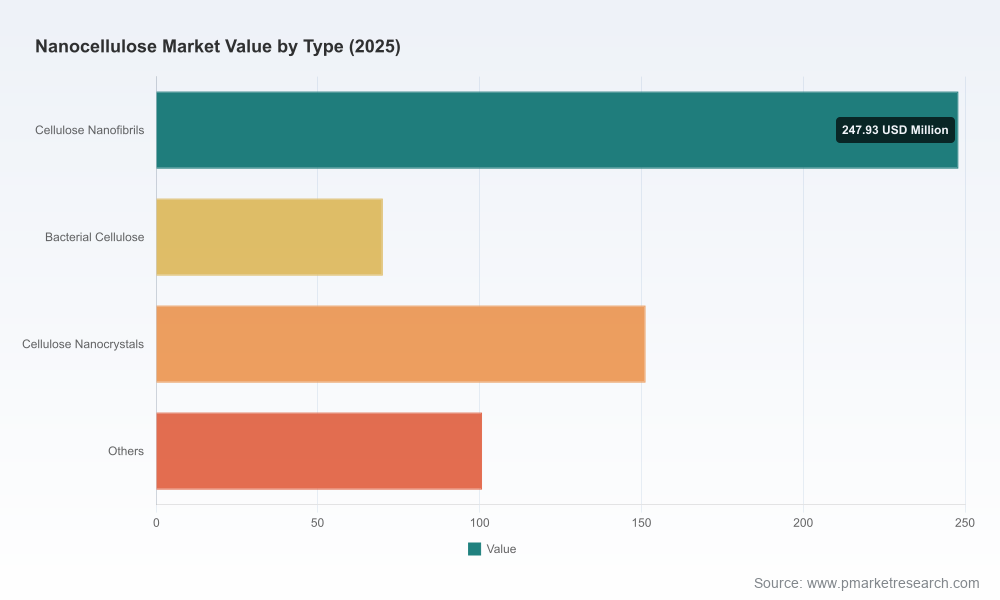

Rapid market scale-up. The nanocellulose market has accelerated from an early-stage base in 2020 to a meaningful commercial footprint by 2025, and is on a trajectory that—at a compound annual growth rate of 20.5%—takes the industry into billion-dollar scale within the 2026–2032 forecast window. For resource allocation decisions in 2026, this pace of expansion changes the calculus for manufacturing capacity, partner selection, and R&D prioritization.

Nanocellulose Market

Cross-sector optionality. Nanocellulose is not a single-use commodity: its technical properties enable plays across packaging, composites, biomedical, coatings, and specialty electronics. That breadth creates multiple routes to scale and distinct commercialization pathways—each with different margin, regulatory, and capex implications.

Nanocellulose Market

Fragmented competitive structure. Market concentration remains low-to-moderate; the three largest suppliers account for a modest share of global revenues, and the top five collectively capture less than a third. This fragmentation favors first movers with scale economics, as well as nimble innovators occupying specialized niches.

Using a 2025 base year, our model integrates historical performance (2020–2025) and technology-specific adoption curves to produce an investment-relevant forecast for 2026–2032. The market’s compound annual growth rate of 20.5% underpins scenarios where incumbent pulp-and-paper capabilities convert into competitive advantage, where engineered fermentation routes reach commercial cost parity for specialty biomaterials, and where regulatory tailwinds accelerate demand for bio-based packaging solutions.

For clarity: this preview intentionally omits the full regional, type and application breakdowns that underpin these headline numbers. The complete dataset — including disaggregated forecasts and unit economics — is available in the full report.

Strategic forecast models calibrated to technology routes (mechanical fibrillation, enzymatic, microbial fermentation), including sensitivity to feedstock cost and energy/water consumption.

Go-to-market playbooks for B2B segments: packaging converters, composites OEMs, medical-device manufacturers, and specialty coatings formulators. Each playbook includes value capture levers, sample commercial terms, and buyer proof points.

Capex/Opex build-outs for brownfield conversions vs. greenfield biorefineries, with staged investment profiles to align with 2026 procurement cycles.

Supplier and partnership matrices: technology licensors, equipment vendors, contract manufacturers, and feedstock aggregators — ranked by strategic fit and execution risk.

Regulatory and standards roadmap (EU, US, ISO/TAPPI): compliance checklists and certification timelines to expedite market entry for food-contact, medical, and packaging applications.

Scenario-based M&A roadmap and integration playbook for consolidation strategies—covering bolt-on acquisitions, capacity pooling, and licensing options.

We profile the full supplier ecosystem, from established pulp and specialty cellulose firms to emerging biotech and pilot-scale producers. Highlights:

CelluForce (Canada) — industrial-scale CNC production and rapid productization into electronics and coatings. Their recent capacity expansion and high‑temperature grades increase the bar for thermal performance in electronics and advanced coatings.

FiberLean Technologies (UK) — differentiated by an onsite production model that reduces logistics and enables integrated supply to large paperboard and packaging converters. This model directly addresses the cost and freshness constraints for water-based nanocellulose dispersions.

Borregaard (Norway) — uses lignocellulosic biorefining know-how to produce multiple nanocellulose grades from spruce biomass, positioning itself strongly for packaging and biomedical customers that value wood‑derived feedstocks.

Nippon Paper, Stora Enso, UPM (Nordic & Japan) — corporate incumbents with integrated pulp operations and market access into packaging and composites supply chains. They are capable of rapid scale-through by leveraging existing fiber supply, but must manage internal capital allocation against other pulp priorities.

Regional champions and innovators — a group that includes Kruger, Oji Holdings, RISE, and a number of venture-backed specialists (e.g., Modern Synthesis, Melodea). These players drive technical variety (CNC, CNF, BNC) and novel feedstock experiments such as agricultural residues and seaweed.

Two important dynamics arise from this roster: first, incumbents can achieve scale advantage through existing fiber and chemical infrastructure; second, a steady stream of niche entrants continues to expand the addressable market by tailoring grades for high‑margin applications. Together these trends create both competitive threat and partnership opportunity for manufacturers and brand owners.

New feedstock pathways — In 2025, commercial demonstrations converting seaweed and agricultural residues into nanocellulose signaled practical, low-cost feedstock alternatives. Companies and regions that secure feedstock aggregation advantage lower variable costs and reduce exposure to wood-fiber cycles.

Product innovation — Several suppliers announced thermally stable and bio‑barrier grades for electronics and recyclable flexible packaging, and the first injectable nanocellulose hydrogel for medical devices reached commercial launch. These product introductions compress development timelines for applications that once required lengthy validation.

Capital formation — Targeted funding rounds for scale-up and pilot plants indicate investor willingness to finance the transition from pilot to production, especially when teams can demonstrate clear downstream offtake or captive demand.

Policy alignment. Regulations addressing single-use plastics and packaging waste in key markets, together with preferential procurement schemes and food/medical certification pathways, materially improve the commercial case for bio-based nanocellulose substitutes.

Standards and safety. Adoption of ISO and TAPPI standards for cellulose nanomaterials reduces buyer uncertainty and enables faster procurement decisions by large brand owners who require consistent quality and safety data.

Infrastructure requirements. Commercial biorefining and mechanical fibrillation are capital-intensive and water/energy-sensitive. Our report models the unit economics across alternative process platforms and quantifies break-even scales relevant to 2026 investment decisions.

Scaling complexity — Moving from pilot to commercial volumes brings operational issues (reproducibility of fibrillation, dispersion stability, downstream integration) that can erode margins if not addressed early.

Feedstock concentration — While feedstock diversification is advancing, localized shortages or logistics costs can still create short-term supply stress for new large-capacity sites.

Substitute technologies — Competing bio-based polymers and performance-engineered synthetics will continue to evolve; winning in a selected application requires a combination of performance parity, cost competitiveness, and regulatory clearances.

Decide now on the scale and model: onsite, captive, or toll-manufacture. Our cost curves and staged capex profiles in the full report let you simulate these choices against customer adoption timelines.

Lock in feedstock or conversion partners through offtake and JV structures — early aggregation reduces price volatility and accelerates certification timelines.

Target high-margin, low-volume applications as an initial beachhead (specialty coatings, medical hydrogels, electronics intermediate films) while building capabilities for higher-volume plays like packaging and composites.

Embed standards and regulatory strategy into product development roadmaps to shorten time-to-market for food-contact and medical use cases.

Our full report equips corporate and investor clients with the concrete inputs needed to act in 2026: disaggregated forecasts by region, type and application; supplier scorecards and M&A candidate ranking; capex/Opex templates; risk-adjusted investment models; and a prioritized short‑list of potential partners and customers. The preview you have read demonstrates the analytical framing; the full report supplies the numeric fidelity and playbooks necessary to execute.

Note: To preserve the strategic value of the research and to comply with our "trailer" approach, we have withheld detailed segment and regional tables from this preview. The complete datasets and executable templates are available to licensed clients and purchasers on our report page.

Contact PW Consulting to request the full Nanocellulose Market report, access the forecast workbook, and arrange a strategy workshop tailored to your company’s portfolio.

For investors: we offer an accelerated due‑diligence package that maps capex timelines, regulatory milestones, and offtake risk for prioritized targets.

Nanocellulose has moved from scientific curiosity to commercial inflection. For leadership teams planning capital deployments, partnerships, or new product lines in 2026, the strategic window to secure advantage is immediate. PW Consulting’s full study gives you the quantitative foundation and practical playbooks to convert that window into durable market presence.

For detailed analysis of this topic, please visit the official page:Nanocellulose Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com