4,4-Biphenol Market — Strategic Outlook for 2026 Decision-Makers

Executive trailer

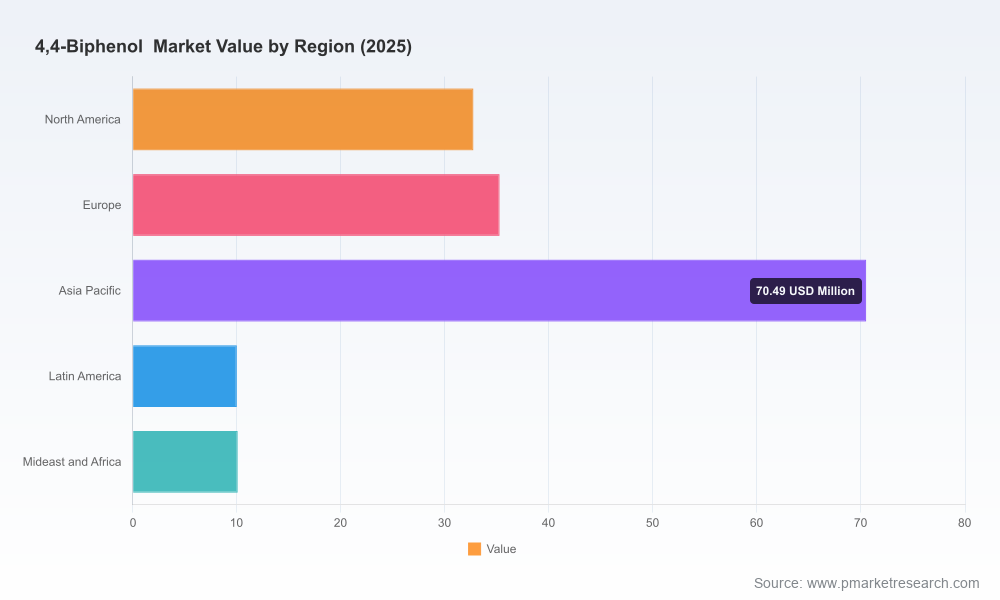

This PW Consulting market briefing previews our full 4,4-Biphenol Market study (base year 2025, historical 2020–2025, forecast 2026–2032). The global market has demonstrated steady expansion from approximately USD 120 million in 2020 to USD 158.55 million in 2025, and our modelling points to a sustained compound annual growth rate (CAGR) of 7.23% across the 2026–2032 forecast window, reaching roughly USD 258.5 million by 2032. Those headline metrics capture a resilient specialty-chemicals segment driven by demand for high-performance polymer feedstocks, evolving regulatory oversight, and constrained supplier capacity.

4,4-Biphenol Market

This piece is written as a strategic “trailer”: it communicates the analytical depth and decision-usefulness of the full report while preserving the proprietary micro-level segmentation and supplier data that compel stakeholders to access the full deliverable for implementation-ready details.

4,4-Biphenol Market

Why this research matters to 2026 corporate strategy

- Timing: 2026 is the inflection year for several strategic choices — finalising capital projects approved in 2024–25, renegotiating multi-year supply contracts, and repositioning product portfolios for accelerated electronics and medical-device demand. The report turns macro growth into actionable inflection points.

- Clarity where uncertainty is concentrated: The market’s 7.23% CAGR masks uneven dynamics across purity grades, finished-polymer end markets, and trade corridors. Executives need to know where premium pricing, quality hurdles, and export/import rules will affect margins and service levels; our report maps those intersections.

- Competitive posture: The market exhibits high concentration — the top three suppliers capture roughly 72% of supply and the top five about 79% — creating structural advantages for incumbents and important barriers for new entrants. That concentration informs choices on capacity commitments, contractual protections, and M&A prioritisation.

What the full report delivers (practical takeaways)

PW Consulting’s full study is designed for commercial, technical and corporate strategy teams who must make binding decisions in 2026. Highlights include:

4,4-Biphenol Market

- Unit-level demand forecasts and topline market sizing (historical and forward) with sensitivity scenarios tied to polymer market performance and electronic/medical device cycles.

- Granular segmentation by product purity class, end-use polymers and trade regions, with comparative growth vectors — presented as modelling blocks clients can toggle by assumption.

- Supplier-by-supplier capacity map and credibility assessment, including quality certifications, traceability practices, and typical lead times (supplier names and profiles are covered at a strategic level in this briefing; the report contains supplier scorecards).

- Price-formation and margin model that links feedstock inputs, duty/tariff regimes, and logistics cost shocks to delivered economics at customer level.

- Regulatory risk matrix and compliance playbook covering global listings, transport classifications, and food-contact/medical-device pathways.

- Deal playbooks for sourcing — short-, medium- and long-term contracting options, hedging and inventory strategies, and criteria for insourcing vs third-party manufacturing.

- M&A and partnership candidate shortlist derived from capability gaps, geographic exposure and integration synergies (with high-priority targets flagged for further diligence).

Market dynamics and regulatory context — what to watch in 2026

The 4,4-Biphenol ecosystem sits at the intersection of high-performance polymer demand and tightening regulatory attention. Several factual developments should shape any 2026 strategy:

- Regulatory monitoring: 4,4-Biphenol appears on several institutional inventories and historical exposure documents, and it is subject to TSCA listings with potential PBT (persistent, bioaccumulative and toxic) monitoring under discussion. While there were no targeted U.S. restrictions issued in 2024–2026, the presence on these regulatory radars increases the probability of more stringent data requirements and compliance costs going forward.

- Tariff signals: The 2026 tariff schedule lists 4,4-Biphenol at a duty-free HTS classification (0%) under the relevant code. That duty treatment reduces a near-term cross-border cost barrier and may encourage trade flows where logistics and lead times are competitive.

- Pathways to specialty end-markets: The compound is recognised in food-contact substance notifications as a monomer for certain copolymers, and it is widely specified for liquid-crystal polymers and other engineering plastics used in electronics, telecoms, and medical devices. These formal recognitions create niche opportunities — but also require rigorous documentation, supply-chain traceability, and product registration effort.

- Operational classification and transport: Safety data sheets and transport rules classify the material under standard RID/GHS categories and, in several data sources, list typical usage restrictions (e.g., R&D-only designations in some SDS entries). Manufacturers and shippers must ensure compliance with local transport regimes and customer acceptance criteria.

Strategically, these dynamics mean buyers should factor regulatory compliance costs and lead-time risk into contract pricing, and sellers should prioritise traceability and credentialing as a differentiation strategy.

Competitive landscape — profiles and strategic implications

The market is dominated by a small set of established producers with materially different strategic postures. This briefing references several active producers and their defining attributes; the full report contains extended company profiles, recent developments, and a supplier-scorecard matrix.

- Chimei Plastic (Taiwan): Known for producing high-purity 4,4'-Biphenol as a plastic-rubber additive and polymer precursor. The supplier benefits from customer relationships in precision plastics industries and emphasizes consistency for high-value downstream applications.

- Honshu Chemical Industry (Japan): Serves the LCP and PPSU segments for electronics and medical device uses. Their value proposition is reliability in regulated end-markets, and they tend to compete on regulatory support and application engineering.

- SII Group (Japan): Targets a broad set of engineering plastics, including LCP, polysulfones, polyaryletherketones and polycarbonates; they bring scale in specialty monomer production and portfolio breadth.

- Ascent Petrochem (China): Industrial-scale manufacturer emphasising ISO-aligned quality and high-purity grades; strong cost-competitiveness and scale orientation are their strategic levers.

- Anhui Liwei Chemical (China): Accredited facility with strict batch traceability and quality protocols; their positioning is aimed at customers requiring documented supply-chain integrity.

Implications:

- High concentration (CR3 ~72%, CR5 ~79%) creates both opportunity and risk: incumbents enjoy pricing discipline, but the supply base is sensitive to capacity outages and feedstock cost volatility.

- Quality and credentialing (99%+ purity classes and ISO systems) are primary entry barriers for downstream OEMs in regulated sectors. A low-cost producer without certified traceability will struggle to displace incumbents in medical or food-contact applications.

- Geographic footprints matter: producers that combine proximity to key polymer-makers with robust export pathways (and favourable tariff treatment) will capture market share during demand upcycles.

Strategic prescriptions for 2026 decision-makers

The following recommendations translate our analysis into actionable next steps for commercial, procurement and corporate strategy teams:

- Embed scenarios into contracting decisions. Use three scenarios (base = consensus growth, upside = accelerated electronics/medical adoption, downside = regulatory/granular substitution) to size contract volumes and escalation clauses through 2028–2030 horizons.

- Prioritise supplier qualification and traceability. For buyers targeting regulated end-markets, require third-party certification and batch-level traceability as non-negotiables; factor compliance proofing timelines into onboarding plans.

- Differentiate on technical support. Sellers should invest in application engineering for LCP and other high-value polymers; value-added services (formulation support, co-development agreements) create stickiness that pure commodity pricing cannot match.

- Hedge logistical and regulatory exposure. Given duty-free classification for the HTS code and evolving TSCA/other listings, combine regional sourcing with modest strategic inventory to reduce single-supplier risk while avoiding overcapitalisation.

- Pursue targeted inorganic options. For firms needing rapid market entry or complementary capabilities (e.g., quality systems, local regulatory expertise), shortlisted bolt-on acquisitions or tolling partnerships are likely more efficient than greenfield builds in 2026.

- Operational excellence in quality control. Invest in analytical capability to substantiate purity claims (especially >99% classes) and implement robust change-control procedures — this materially reduces commercial friction with regulated customers.

How PW Consulting supports decision execution

Our full 4,4-Biphenol report is built to be operational. Clients receive the underlying model, configurable scenario inputs, supplier scorecards, and a regulatory playbook. We also offer on-demand services: commercial due diligence for transactions, supplier selection workshops, regulatory gap assessments, and bespoke forecasting tied to client-specific product portfolios.

If you are preparing contracting rounds, validating a capacity expansion, assessing M&A opportunities or developing a go-to-market strategy for specialty polymer feedstocks in 2026, PW Consulting’s dataset and engagement teams convert uncertainty into accountable decision pathways.

Next step — where to get the full intelligence

This briefing intentionally omits the micro-segmentation tables, supplier-level revenue splits and unit-cost curves that clients need to execute. The full report contains those deliverables — including purity-grade revenue by end-use polymer, regional supply-demand balances and supplier capacity schedules — along with downloadable models you can plug into your planning systems. Visit PW Consulting’s report page to access the complete study, modelling assets, and advisor engagement options.

For detailed analysis of this topic, please visit the official page:4,4-Biphenol Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com