Hydrofluoroether (HFE) Market: Strategic Imperatives for 2026 — A PW Consulting Preview

As companies across electronics, semiconductor, precision cleaning, and thermal management sectors plan their 2026 investments, the Hydrofluoroether (HFE) market presents both a clear growth runway and a dense set of strategic trade-offs. PW Consulting’s forthcoming full-market study — based on a 2025 base year, a 2020–2025 historical series and a 2026–2032 forecast horizon — synthesizes market-sizing, supply-chain dynamics, regulatory inflection points and competitive positioning into an actionable playbook for decision makers. This preview outlines why HFEs deserve prioritized attention in 2026 capital, procurement and product roadmaps, and what executive teams should focus on before accessing the complete dataset on our portal.

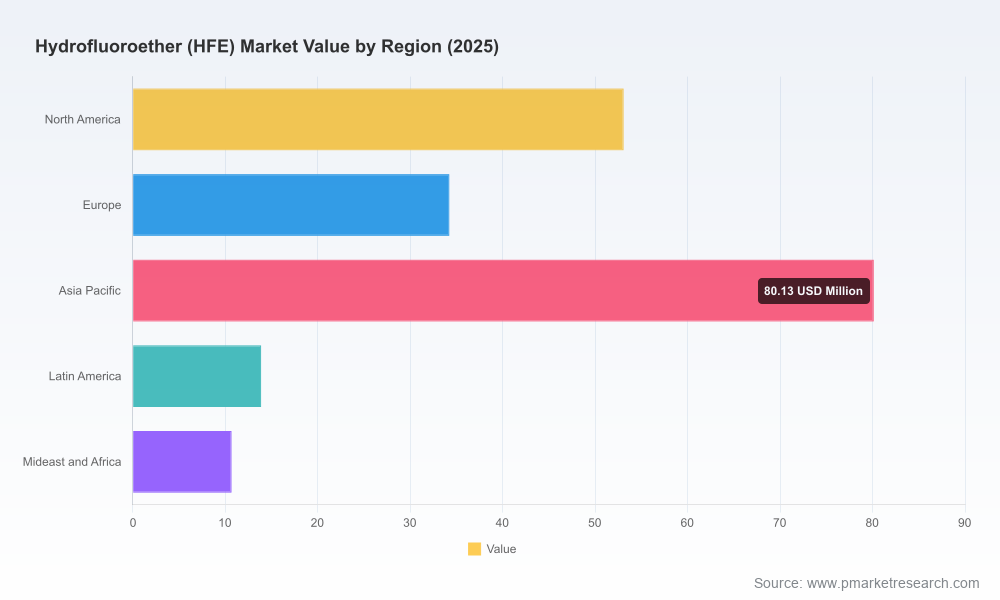

Hydrofluoroether (HFE) Market

Macro picture: steady expansion with structural tailwinds

Our top-line market model shows the HFE market expanding from an overall market size of USD 192.0 Million in 2025, growing at a compound annual growth rate (CAGR) of 6.98% through the forecast window, and reaching an estimated USD 308.8 Million by 2032. That trajectory reflects more than cyclical demand: it is driven by durable structural shifts — regulatory substitution away from high-GWP and ozone-depleting fluids, accelerated semiconductor fab builds, and rising adoption of HFEs in precision cleaning and heat-transfer niches where low global warming potential and electrical non-conductivity command premium specification status.

Hydrofluoroether (HFE) Market

For 2026 strategic planning, the key takeaway is that HFEs are not a marginal specialty anymore; they are a distinct, investable product class with a reliable growth profile. This translates into near-term commercial opportunities (supply contracts, product qualification wins) and medium-term strategic bets (manufacturing capacity, licensing/partnership models, or selective M&A) that can materially alter competitive trajectories.

Hydrofluoroether (HFE) Market

Why 2026 is a decision-making inflection point

- Regulatory crystallization: Global regulatory drivers that matured in 2024–2025 — including strengthened HFC controls under international and regional frameworks — have accelerated customer qualification cycles for low-GWP HFEs. By 2026 many OEMs and fabs will expect validated HFE supply chains as a procurement prerequisite.

- Supply reconfiguration: The market experienced a notable supply reallocation following major incumbents’ strategic exits and policy-driven constraints. That reconfiguration is still bedding down, creating windows for new entrants and capacity expansions to capture displaced volumes, but it also increases the premium on supply continuity and risk-mitigated sourcing strategies.

- Cost pressure and raw material volatility: Upstream feedstock markets have tightened, driven in part by competing industrial demand. Cost inflation at the raw-material level materially affects variable cost curves for manufacturers and will shape near-term pricing and contractual strategies.

- Customer specification cycles: Semiconductor and high-precision electronics vendors are in multi-year qualification timelines. Winning 2026 procurement cycles means having validated product specifications, test data, and service-level commitments well in advance — a capability gap for some new suppliers.

Report coverage: what the full PW Consulting study delivers

To support executable 2026 strategies, our full report bundles analytical depth with operational utility across the following modules:

- Market-sizing and forecast model (historical 2020–2025, base year 2025, forecast 2026–2032) with downloadable scenario-ready datasets in USD Million and unit-equivalents.

- Demand-driver diagnostic that maps end-market adoption curves (semiconductor, precision cleaning, heat-transfer, and emerging uses) against regulatory and capital-expenditure cycles.

- Supply-chain mapping from upstream feedstocks through fluorochemical synthesis to finished HFE blends, including a cost-build model and sensitivity analysis to raw-material price shocks.

- Regulatory and standards matrix outlining qualification pathways under relevant regimes and key compliance milestones that accelerate or constrain adoption.

- Competitive landscaping with supplier scorecards, capability heat-maps, and comparative risk assessments, plus a strategic options framework for incumbents and challengers.

- Commercial playbooks — procurement, JV and partner models, sample RFP language, and go-to-market tactics for rapid qualification wins in semiconductor and optics segments.

- M&A and investment playbook highlighting accretive acquisition targets, integration risks, and forward-looking return scenarios under multiple demand cases.

- Executive implementation timelines and 30/60/90-day actions for procurement, technical, regulatory and investor relations teams.

Competitive landscape: incumbents, challengers, and strategic responses

The HFE competitive set today includes integrated fluorochemical incumbents, specialty chemical houses, and regional high-volume producers. Several firms have strengthened or adjusted their positions recently:

- 3M (St. Paul, MN) — historically a leading supplier of engineered HFE fluids, completed a full exit from PFAS manufacturing at the end of 2025. That strategic move reshaped near-term supplier availability and opened short-term requalification opportunities for alternative suppliers while raising questions for customers reliant on long-term continuity.

- Solvay (Brussels) — positioned as a specialty producer with strong high-purity capabilities and established relationships in semiconductors and battery manufacturing; the company remains a strategic option for OEMs prioritizing tight process controls and global technical support.

- Daikin Industries (Osaka) — leverages integrated fluorochemical manufacturing to provide both HFE-based solvents and thermal fluids; their vertical integration provides resilience to feedstock volatility but requires scrutiny on contractual flexibility for buyers.

- AGC Chemicals (Tokyo) — notable for product lines targeted at semiconductor and precision electronics customers, AGC’s route-to-market emphasizes application engineering and joint qualification programs.

- Kaneko Chemical (Yokosuka) — active in promoting drop-in HFE replacements and engaging with electronics trade shows in 2025; their commercial momentum underscores how specialists can capture dislocated demand by aligning product specs with incumbent platforms.

- Major Chinese producers (e.g., Shandong Huaxia Shenzhou, Juhua Group) — expanding capacity and export focus, these players are increasingly relevant for volume-driven industrial cleaning applications and for firms seeking competitive pricing, subject to regulatory acceptance in target markets.

Collectively, the universe of suppliers now offers a broader set of choices — but choice is only valuable if matched to long-lead qualification timelines, technical compatibility and regulatory acceptance. Our full supplier scorecards identify where each firm is advantaged or vulnerable across these vectors.

Strategic implications and recommended actions for 2026

- Procurement: Move from spot-buying to contracted, multi-source strategies that prioritize technical qualification and inventory buffers. Short-term cost savings without qualification throughput will expose manufacturers to fab downtime risk.

- Manufacturing and capacity planning: For chemical producers, 2026 is a year to decide between bolt-on capacity expansions versus strategic partnerships that accelerate time-to-market. Investment models should be stress-tested against raw-material volatility scenarios.

- R&D and product strategy: Prioritize formulations that balance low-GWP credentials with electrical and thermal performance. Differentiated application engineering and data packages shorten customer qualification cycles and increase price elasticity.

- Regulatory and sustainability: Build a compliance-forward roadmap and data transparency protocol that anticipates tighter regional rules and customer ESG requirements. Pre-emptive certification and emission profiling reduce commercial friction.

- M&A and partnerships: Target niche capability owners (application testing facilities, localized production assets, or regulatory-compliance consultancies) to accelerate market entry and de-risk customer qualification.

Where this preview leaves you — and why the full study matters

This preview surfaces the strategic contours executives must confront in 2026: a reliably growing HFE market, supplier rebalancing after notable exits, regulatory drivers that institutionalize demand, and raw-material dynamics that compress margins for the unprepared. While these high-level signals are sufficient to elevate HFEs on your strategic agenda, implementing winning moves requires access to granular, sourceable intelligence — regional demand curves, application-level qualification timelines, supplier operational scorecards, and the downloadable financial model that underpins our scenario runs.

PW Consulting’s complete Hydrofluoroether Market report provides those depth elements and the operational templates (RFPs, supplier risk checklists, CAPEX decision matrices) your teams can deploy immediately. For procurement, engineering, and corporate development leaders aiming to convert 2026 intentions into durable commercial advantage, the full dataset and playbooks are designed to shave months off qualification cycles and reduce execution risk.

Next steps

Access to the full PW Consulting study will grant your team: the detailed forecast model in USD Million, supplier scorecards, regulatory qualification pathways, and an actionable 12–24 month implementation plan. Visit our report page or contact our advisory desk to request an executive briefing and receive tailored guidance on how to operationalize these insights within your organization’s 2026 planning cycle.

For detailed analysis of this topic, please visit the official page:Hydrofluoroether (HFE) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com