PW Consulting: IV Bags Market Poised for 5.8% CAGR Through 2032

Health |

2026-07-09 08:26:24

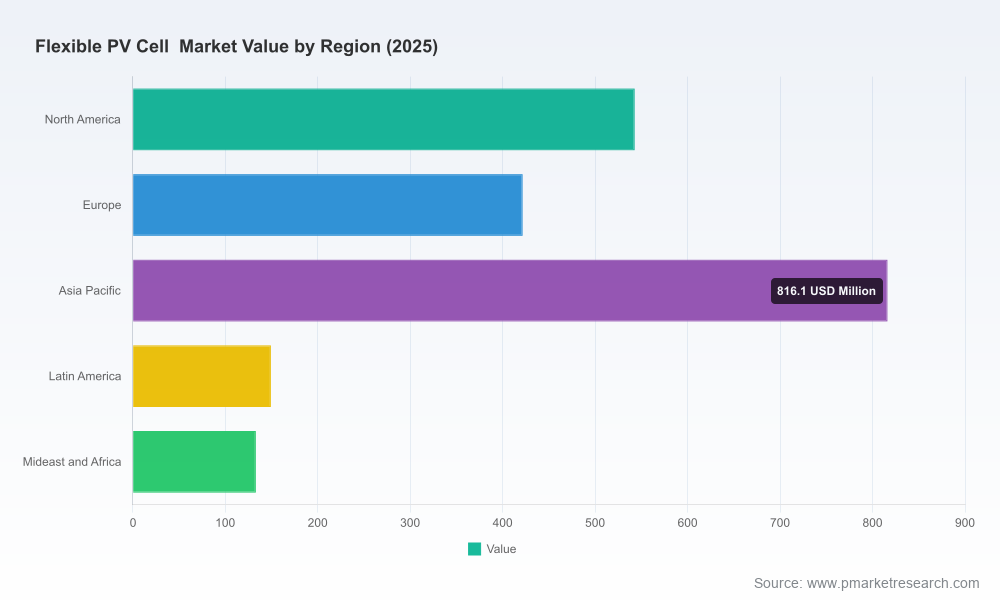

As PW Consulting’s lead industry analyst, I present a focused preview of our forthcoming Flexible PV Cell Market study — a decision‑grade briefing tailored for corporate strategists, M&A teams, and product leaders preparing for 2026. The market has evolved from a niche enabler of portable and specialized power to a commercially material layer within broader solar and electrified systems. Our analysis traces the market from a 2020 base of approximately USD 1,095 Million to an estimated USD 2,063 Million in the 2025 base year, with a forecast trajectory that reaches roughly USD 5,017 Million by 2032. The forecast period (2026–2032) is modeled at a compound annual growth rate (CAGR) of 13.5% — a rate that transforms strategic tradeoffs (material selection, integration models, channel choices) into make-or-break decisions for 2026 and beyond.

Flexible PV Cell Market

Timing of capital allocation: With the market roughly doubling over the 2025–2032 window, near‑term investments (capacity, certification, OEM partnerships) will determine whether incumbents convert growth into durable advantage or leave value on the table.

Flexible PV Cell Market

Margin and price dynamics: Policy and trade shifts in early 2026 have already altered supplier economics; understanding pass‑through, hedging, and vertical integration options is now essential.

Flexible PV Cell Market

Product roadmaps and channel strategies: The flexible PV segment’s growth is uneven across use‑cases and substrates. Our study enables prioritization without overcommitting to subsegments that remain immature.

The numerical arc matters. Historically, the market expanded steadily from the low‑USD billions in 2020 to a market size exceeding USD 2 billion in the 2025 base year. Our 2026 projection captures the first full year of post‑policy equilibrium, with incremental capacity additions and product launches pushing the market northward in the near term. By 2032, the industry is on track to be a mid‑single‑digit billion‑dollar opportunity in absolute terms (USD Million unit reporting), reflecting sustained adoption across consumer electronics, transportation, building integration, and niche heavy‑duty applications such as aerospace and defense.

Importantly, the 13.5% CAGR through 2032 is not uniform: our scenarios show pockets of accelerated adoption where regulatory incentives, local manufacturing, or product certification lower integration friction — and slower growth where technical tradeoffs or long sales cycles prevail. The report provides scenario runs that quantify these different growth rhythms to support capital planning and commercial roadmap sequencing.

Two supply‑side phenomena have reshaped the 2026 tactical landscape. First, significant policy movement in early 2026 removed a major export rebate that had subsidized module shipments from a key supplier market. That change immediately rebalanced global module economics and triggered industry forecasts of mid‑teens percentage price movement through late 2026 versus late‑2025 benchmarks. Second, raw‑material and substrate constraints — from specialty polymers to encapsulants and adhesives — have tightened lead times and raised qualification hurdles for OEMs integrating flexible cells into finished goods.

For procurement and strategy teams, the implication is straightforward: near‑term sticker price volatility coexists with structural demand growth. Hedging strategies, diversified sourcing, near‑shoring of critical production stages, and certification roadmaps should be evaluated in tandem rather than in isolation.

Flexible PV is a convergence technology: cell chemistry, substrate engineering, lamination, and process integration deliver the customer‑visible attributes (efficiency, weight, flexibility, lifetime). Our study documents how plastic substrates (polymeric films) remain commercially dominant for portable and curved‑surface applications due to cost and processing advantages, but require high‑quality barrier coatings to meet lifetime expectations under humidity and oxygen exposure. Simultaneously, ultra‑thin flexible glass is advancing rapidly for building‑integrated photovoltaics (BIPV) applications, valued for superior optical transmittance and weather resistance.

Cell technologies — from thin‑film CIGS to emerging perovskite tandems and specialized radiation‑hardened architectures — are each playing distinct roles in the value chain. The report evaluates maturity, reliability datasets, and integration costs for each technology family and maps where they are likely to achieve commercial scale within our forecast window.

The Flexible PV segment remains relatively unconcentrated: market share metrics indicate a fragmented landscape where the top three to five firms do not dominate. This fragmentation creates room for differentiated plays — product specialization, channel exclusivity, or IP‑protected manufacturing processes.

Two illustrative company profiles captured in our research show how different strategic postures play out:

PowerFilm Solar (Iowa, USA) — an incumbent focused on thin‑film amorphous silicon on flexible polyimide substrates. Their roll‑to‑roll monolithic integration and emphasis on ruggedized, lightweight modules have made them a go‑to for transportation and defense use‑cases. Their playbook underscores vertical integration of cell processing and module lamination to reduce failure modes in harsh environments.

Sungold Solar (Shenzhen, China) — a producer of flexible panels using monocrystalline cells with polymeric lamination and a pronounced OEM/ODM footprint for RV, marine, and curved installations. Recent certification achievements in early 2026 have strengthened their position in export and regulated channels, improving adoption prospects among global OEMs.

Beyond these names, our market map captures a wave of strategic activity — certifications, capacity plays, and M&A. Notably, a 2026 acquisition anchored a U.S. domestic capability in radiation‑hardened space cells, a development that shortens supply chains for space and defense primes and raises the bar for non‑U.S. suppliers targeting those segments.

Policy shifts and certification standards matter disproportionately for flexible PV because the products are frequently integrated into regulated end‑use systems (vehicles, buildings, defense). The report includes an indexed matrix of certifications, test standards, and region‑specific procurement requirements that buyers and suppliers can use to accelerate qualification timelines. We also model the commercial impact of tariff and incentive changes on landed cost and gross margins for different go‑to‑market models (direct OEM supply, licensed module supply, contract manufacturing).

Demand scenarios and an investment trigger matrix: When to build capacity, when to partner, and when to license technology based on adoption curves and policy risk.

Technology moat and risk assessment: Comparative due diligence on cell chemistries, substrate choices, and encapsulation strategies — including failure‑mode sensitivity and lifecycle cost modeling.

Commercial playbooks by application: Best practices for channel engagement, pricing templates, and certification roadmaps for consumer electronics, automotive integration, BIPV, and aerospace/defense segments.

Competitive heat map and M&A scorecard: Identification of likely acquisition targets, strategic partners, and integration risks — informed by recent industry moves and the market’s low concentration profile.

Supply chain optimization blueprints: Inventory strategies, dual‑sourcing templates, and short‑/medium‑term procurement actions to mitigate the immediate price pressure and input volatility observed in 2026.

Prioritize certification and qualification in target geographies before scaling production. Speed‑to‑certification is a competitively scarce capability that converts product interest into procurement awards.

Lock in substrate and barrier supply agreements with performance‑based pricing to protect margins against near‑term price spikes in encapsulants and specialty polymers.

Evaluate near‑shoring or regional contract manufacturing for high‑security or regulated customers; the acquisition activity we tracked demonstrates demand for localized, certifiable capacity.

Design modular product platforms where cell, substrate, and encapsulation choices can be swapped without re‑engineering the entire system, reducing time‑to‑market across diverse end uses.

Adopt a portfolio approach to technology bets: fund incremental pilot lines for emerging high‑value cell technologies while maintaining volume and cash generation in proven product families.

This article is a strategic primer designed to convey the analytical depth of PW Consulting’s Flexible PV Cell Market research while reserving detailed segmentation tables and proprietary projections for the full report. Subscribers will receive the complete dataset (historical 2020–2025 and forecast 2026–2032 in USD Million), segmented market models, scenario outputs, and company diligence packs — all structured to support board‑level decisions in 2026.

For organizations deciding where to allocate capital in 2026 — whether that means expanding capacity, pursuing certification, striking OEM deals, or evaluating M&A options — our study translates the market’s projected 13.5% CAGR and multi‑billion‑dollar endpoint into concrete, prioritized actions. To access the full intelligence set, including detailed segmentation by region, type, and application, and the comprehensive competitive profiles and financial models, please follow the report link on PW Consulting’s research portal.

For detailed analysis of this topic, please visit the official page:Flexible PV Cell Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com