Why Investors Are Watching the Pet Milk Replacers Market Closely

Other |

2026-05-15 06:39:03

As companies prepare strategic moves entering 2026, understanding the evolving commercial landscape for drugs addressing osteoarthritis (OA) pain is no longer optional — it is mission-critical. PW Consulting’s latest market study synthesizes macro trajectories, regulatory inflection points, competitive plays, and near-term translational risks to equip executives with the evidence required for confident portfolio, M&A, and go-to-market decisions.

Drugs for Osteoarthritis Pain Market

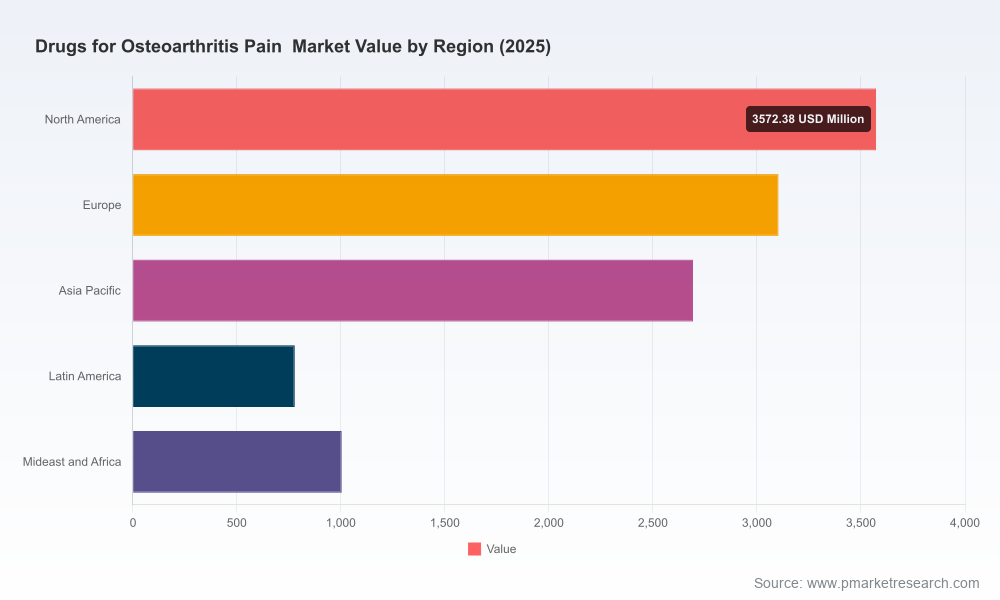

The OA pain drug market has demonstrated steady expansion in the first half of the decade and remains on a durable upward trajectory. Our base-year analysis shows the market expanding from mid-single-digit billion-dollar levels in 2020 to an estimated USD 11,150 Million in 2025. Under our baseline scenario, we project continued growth through the forecast window to reach roughly USD 16,590 Million by 2032, reflecting a compound annual growth rate (CAGR) of approximately 5.85% over the forecast period.

Drugs for Osteoarthritis Pain Market

These headline figures mask meaningful heterogeneity beneath the surface: product class lifecycle dynamics, route-of-administration trade-offs, payor reimbursement shifts and emerging non-opioid therapeutics all re-shape the value chain. PW’s analysis intentionally layers a top-down market model with product-level demand drivers so that executives can test strategic choices against realistic, actionable scenarios rather than raw extrapolations.

Drugs for Osteoarthritis Pain Market

The market is best described as moderately fragmented: the top three global players account for roughly a third of market revenues, while the top five bring concentration to just over forty percent. This structure creates both opportunities and constraints. Large multinational pharmaceutical firms retain strong distribution and payer relationships, enabling rapid scale for incremental launches. At the same time, fragmentation leaves room for specialty entrants — biotechs and regional players — to capture niche value through differentiated mechanisms, targeted delivery, or superior payer economics.

Incumbent manufacturers such as Pfizer, Johnson & Johnson, Bayer, Sanofi and GSK continue to anchor the market with established oral NSAID portfolios and extensive clinician engagement programs.

Therapeutics-oriented players — including AbbVie, Merck and Eli Lilly — compete through differentiated small molecules and centrally acting agents (for example, duloxetine or selective COX-2 inhibitors), focusing on patient segmentation where systemic therapies offer clear benefit-risk advantages.

Consumer-health focused firms such as Haleon operate from a positioning that emphasizes broad accessibility and OTC economics, creating a complementary channel dynamic to prescription therapies.

For strategic planners, the implication is clear: large-scale distribution and payer contracting advantages preserve incumbent moat for broad-use molecules, while innovation and route-of-administration differentiation (e.g., intra-articular formulations, liposomal carriers, gene therapy approaches) represent the most credible paths for disruptive entrants to capture premium pricing and payer coverage.

Regulatory and pipeline activity over the past 18 months has materially altered timing expectations for several novel candidate types. Notable developments include fast-track designations and IND acceptances for non-opioid, localized therapies and gene-based approaches targeting knee OA pain. These events compress the window between clinical proof-of-concept and potential commercial entry, changing the economics of licensing and partnership opportunities for larger players seeking late-stage assets.

Non-opioid, localized injectables have received regulatory attention that shortens development uncertainty and increases the attractiveness of commercialization partnerships.

Gene therapy and neurotrophin-targeted programs, while higher risk, are progressing through regulatory gates that could create high-margin specialty options for severe, refractory OA subpopulations.

At the same time, regulatory agencies and payor bodies are clarifying outcome expectations: guidance documents and endorsed endpoints (for instance, validated pain subscales for knee OA) are converging clinical and reimbursement evidentiary standards.

For 2026, the practical consequence is that companies must re-evaluate R&D timelines, investment thresholds and partnership strategies: earlier engagement with regulatory authorities and payors becomes a differentiator, and readiness for rapid scale-up (or strategic divestment) will decide whether a candidate becomes a market challenger or a stranded asset.

Our qualitative and quantitative synthesis identifies five interdependent dynamics that will shape market winners and losers through 2026:

Clinical differentiation versus convenience: efficacy gains must be balanced against the logistical and cost burdens of administration (e.g., intra-articular vs. oral).

Payer acceptance and evidence alignment: adoption will require trials designed around payer-relevant endpoints and real-world outcomes aligned with recent clinical guidance.

Supply-chain and raw-material risk: some viscosupplements rely on specific biological sources, and procurement constraints can translate into pricing and availability volatility.

Access programs and affordability levers: copay assistance and patient-support models are increasingly central to commercial rollouts for higher-cost intra-articular agents.

Competitive timing and launch sequencing: fast-track regulatory paths and IND acceptances compress windows for value capture and influence M&A and licensing urgency.

Executives facing portfolio prioritization or M&A trade-offs should consider differentiated playbooks by strategic objective:

Scale and defense (incumbent pharma): prioritize lifecycle management for core oral agents, deepen payer contracts, and selectively license or co-promote injectable or specialty assets to shore up margins and front-line access.

Disruption and premium capture (biotech/innovators): focus on robust, payer-aligned endpoints, develop practical delivery models that minimize site-of-care friction, and plan partnerships that accelerate commercialization while preserving upside through milestone structures.

Channel optimization (OTC & consumer-health): leverage broad distribution and brand recognition to capture early, low-friction demand while monitoring prescription-level innovations that could encroach on self-care populations.

Strategically, M&A and licensing windows are most attractive when clinical readouts reduce technical and regulatory uncertainty but before incumbent pricing responses are fully deployed. Our valuation scenarios quantify this timing premium and should be used to inform term sheets and preferred deal structures.

Our complete Drugs for Osteoarthritis Pain Market report is structured to move an executive from insight to action. It includes:

A granular market model with base-year calibration (2025) and scenario-driven forecasts covering 2026–2032, enabling sensitivity testing against price, uptake, and access assumptions.

Clinical-to-commercial translation matrices that map trial endpoints to payer coverage likelihood and expected time-to-reimbursement.

Competitive landscaping and capability heatmaps for the leading manufacturers, highlighting commercial strengths, gaps in the portfolio, and potential partnership targets.

Regulatory and reimbursement horizon scans, including the latest agency guidance and practical implications for clinical development and label strategy.

Commercial launch playbooks and pricing scenarios, with recommended contracting strategies, sample patient-support program architectures, and channel-specific tactics.

Supply-chain risk assessment, including raw material dependencies and mitigation strategies for specialty formulations.

M&A and licensing decision frameworks with illustrative valuation ranges, deal-structuring templates, and timing recommendations calibrated to the current pipeline landscape.

Importantly, while this executive briefing illustrates structural market direction and strategic implications, PW Consulting’s full deliverable provides the underlying models, assumptions and segment-level data necessary to operationalize these recommendations — access to that granularity is essential for deal negotiation, product launch budgeting, or regulatory planning.

From our analysis, three immediate actions should be on every 2026 planning checklist:

Re-scope late-stage development plans to align trial endpoints with payer-preferred measures and recently issued regulatory guidance to minimize commercialization risk.

Assess partnership versus build economics for specialty injectables and gene-based approaches now that several programs have advanced regulatory milestones; timing of deals materially affects valuation and time-to-market.

Stress-test supply chains and launch budgets against higher-cost administration scenarios and potential access-support programs; early investment in patient-support infrastructure often determines uptake velocity for premium therapies.

The OA pain market is expanding and evolving in ways that reward proactive strategy and disciplined execution. Our study translates macro growth (USD 11,150 Million in 2025; a projected rise to about USD 16,590 Million by 2032 at a CAGR near 5.85%) into decision-ready intelligence: which assets to accelerate, which partnerships to prioritise, and where to allocate go-to-market capital to maximize risk-adjusted returns.

PW Consulting’s report is purpose-built for leadership teams, corporate development, and commercial functions who must make high-stakes decisions in 2026. If your organization needs modeled scenarios, transaction-ready valuation frameworks, or a validated launch playbook for an OA pain asset, our full report contains the operational detail you will rely on — and the data you will use at the negotiating table.

For access to the full dataset, segmentation analysis and executable recommendations, please visit the report page linked from PW Consulting’s market insights portal.

For detailed analysis of this topic, please visit the official page:Drugs for Osteoarthritis Pain Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com