How to Add Money to Venmo Without a Bank Account

Networking |

2026-06-25 12:18:05

As PW Consulting’s lead industry analyst, I present a focused market introduction designed to orient executive teams, corporate development groups, and product strategy leads as they make high-stakes decisions in 2026. This briefing synthesizes our latest Printed Battery Market study (base year 2025, historical coverage 2020–2025, forecast 2026–2032) to highlight where value will be created, which risks matter most, and how to prioritize investments without disclosing the granular segmentation that makes the full study proprietary.

Printed Battery Market

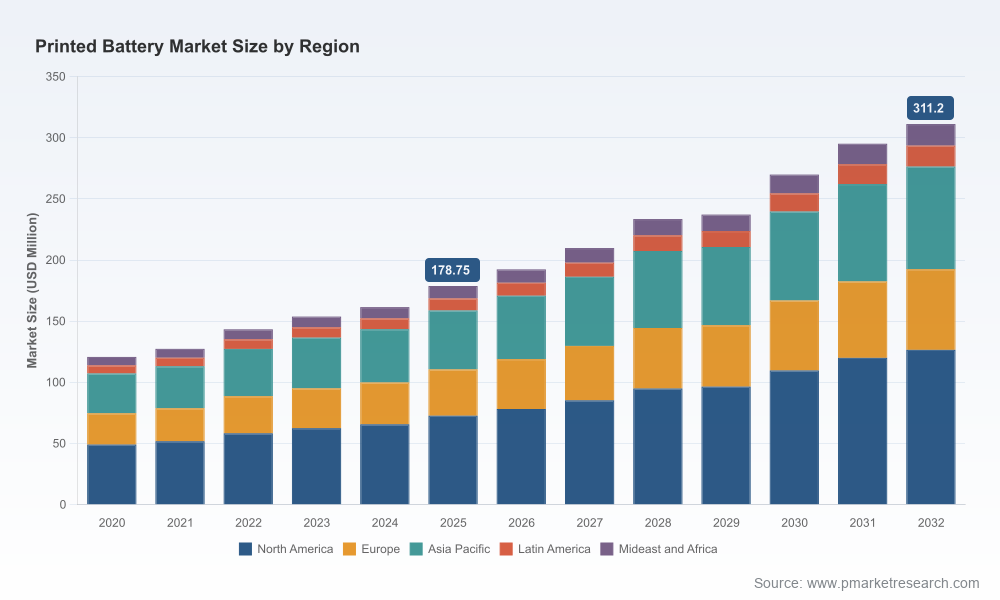

The printed battery sector has transitioned from niche laboratory development to early commercial traction. Our historical model shows the market expanding from a modest base in 2020 to a material market size by 2025, and under our central forecast the market is set to grow at a compound annual growth rate of 8.25% across 2026–2032. By 2026 the market is already meaningfully larger than the 2020 vintage, and our scenario work points to sustained expansion through 2032 driven by integration into disposable smart labels, medical patches, and low-power IoT endpoints.

Printed Battery Market

From pilot to procurement: Several strategic pilots and early commercial wins in 2025–2026 are converting development roadmaps into purchase decisions. Companies that finalize qualification cycles in 2026 will secure first-mover advantages across select use cases.

Printed Battery Market

Regulatory inflection: Tightening battery regulation in key markets is raising compliance costs and influencing supplier selection. Firms that lock in compliant supply chains and recycling pathways in 2026 will face lower retrofit costs later.

Capital allocation window: Manufacturing scale-up for printed batteries requires specialized capital equipment and yield engineering. Boards deciding 2026 capex plans will determine who achieves competitive unit economics by the end of the decade.

Our consolidated model reports a clear upward trajectory: the market expanded steadily through 2020–2025 and is forecast to continue growing strongly to 2032 under the central scenario. The forecast path reflects adoption in consumer electronics, wearables, medical devices and a growing set of disposable electronics use cases. Market concentration is moderate: the top three players capture a majority share, with the top five increasing that lead—an important structural factor for procurement and partnership strategies.

Technology diffusion vs. unit economics: Printed batteries offer unique form-factor advantages (ultrathin, flexible, printable on substrates) that enable product designs impossible with conventional cylindrical/pack batteries. However, specialized equipment (vacuum deposition, roll-to-roll platforms) and current raw material costs constrain near-term unit economics. The commercial winners will be those that optimize process yields and unlock lower-cost material formulations.

Regulatory and EoL (end-of-life) pressure: Recent regulatory tightening around battery manufacturing and end-of-life management necessitates early investment in compliance-ready designs, traceability, and recycling value-chains. These constraints will affect supplier selection and sourcing strategies in 2026–2027.

Integration-driven demand: The biggest immediate use cases are integration-led — smart labels, medical patches, continuous monitoring wearables, and embedded IoT sensors. Buyers are prioritizing suppliers that can co-develop form-factor-specific solutions and meet qualification timelines.

Consolidation & partnerships: With moderate concentration at the top, expect strategic tie-ups, selective M&A, and corporate venture activity as global electronics and materials players seek in-house capabilities or secured supply. 2025–2026 financing and pilot activity already evidence this trend.

Our full study is built for decision-makers who need executable intelligence, not academic theory. Core deliverables include:

An audited market model (2020–2025 historical, 2026–2032 forecast) with scenario levers for technology adoption, price erosion, and regulatory impact.

Demand-driver maps and use-case matrices that identify near-term commercial pathways versus longer-term platform bets.

Manufacturing and CAPEX playbook describing equipment footprints (roll-to-roll, vacuum deposition), unit-cost drivers, and scale milestones required to approach incumbent battery economics.

Supply chain risk map covering raw material suppliers, single-source components, and logistics sensitivities tied to regulatory compliance.

Go-to-market and procurement frameworks — vendor scorecards, qualification timelines, and negotiation playbooks for OEMs and integrators.

Regulatory and EoL compliance templates, including lifecycle assessment inputs and circular-economy pathways tailored to EU and North American frameworks.

Commercial scenarios and quick-return cases for product teams assessing pilot-to-production roadmaps in 2026.

The provider ecosystem combines nimble specialist developers and established electronics/materials houses. Several profiles are representative of strategic archetypes we analyze in the report:

Pure-play innovators: Companies such as Enfucell Oy (Vantaa, Finland) and Jenax Inc. (Republic of Korea) are focused on flexible, application-specific printed batteries for wearables, medical patches, and disposable IoT — attractive for co-development agreements and rapid prototyping.

Medical- and monitoring-focused players: Blue Spark Technologies (Westlake, Ohio) and Cymbet Corporation (New Brighton, Minnesota) have architectures and certifications aligned with continuous vital-sign monitoring and embedded medical applications, making them logical partners for regulated product lines.

Scale-oriented manufacturers and incumbents: Global groups such as Samsung SDI, Panasonic Industry, and LG Energy Solution are moving from prototyping to pilot lines, signaling potential for rapid scale-up or strategic licensing of printed formats into mainstream device portfolios.

Application-specialists and systems integrators: Companies like Planar Energy Devices, BrightVolt, FlexEl, Ultralife and Power Paper occupy niches—flexible consumer products, smart labels, and embedded industrial electronics—where integration capability and supply continuity are crucial.

New commercial entrants and breakthroughs: Recent commercial-level wins and defense contracts indicate an accelerating path to scale for certain players; strategic diligence should track these commercialization milestones closely.

We evaluate each company on technology readiness, IP defensibility, manufacturing maturity, channel access, and regulatory posture. The study’s vendor scorecards assign weights aligned with typical 2026 OEM procurement priorities but the detailed scoring and underlying metrics are available only in the full report.

Commercial breakthrough and defense demand from late-stage entrants signal that printed batteries are crossing important qualification thresholds — a sign that the procurement landscape will shift from R&D sourcing towards strategic supplier selection.

Significant corporate investments and pilot projects from large battery and electronics firms show that incumbents are hedging bets: expect faster pathway-to-scale in use cases that align with broader device roadmaps (e.g., foldable displays, medical patches).

Capital and venture flows into key innovators are compressing timelines; firms that secure preferred supply or IP licenses in 2026 can move from pilot winners to market leaders by early-2030s.

Prioritize qualification for one to two high-value use cases. Avoid breadth-first approaches in 2026; concentrated qualification yields faster time-to-revenue and better negotiation leverage with suppliers.

Build supply chain defensive options. Given material and equipment constraints, secure preferred vendor relationships and consider co-investment in near-shore pilot capacity to mitigate regulatory and logistics risk.

Insist on compliance-first specifications. Regulatory tightening increases the cost of non-compliance. Integrate EoL and traceability requirements into supplier RFPs from the outset.

Design for manufacturability early. Product teams should partner with printed-battery suppliers during early design cycles to optimize substrates, laminates, and connector standards — reducing rework and qualification delays.

Consider strategic corporate venturing or minority investments in high-potential specialists to secure early access to capacity and IP while keeping financial exposure controlled.

Our Printed Battery Market study is purpose-built for decision-makers who need to move from strategic intent to executable plans in 2026. We provide the full market model, supplier scorecards, CAPEX and OPEX build-outs for pilot lines, regulatory compliance playbooks, and M&A due diligence templates. The public summary you are reading intentionally omits core segment-level data and granular vendor metrics to preserve the actionable insights we deliver to clients.

For teams preparing procurement cycles, product launches, or capex approvals this year, the study delivers the evidence base and scenario-tested playbooks needed to de-risk choices. Access to the full dataset and the accompanying advisory workshop will enable your organization to finalize 2026 budgets and supplier commitments with confidence.

Contact PW Consulting for the full report and to schedule a tailored briefing focused on your use cases. Our advisory engagement includes a 90-minute executive workshop and a bespoke sensitivity run of the market model for your product portfolio.

If you are conducting vendor due diligence, we can provide the detailed vendor scorecards and a recommended short-list calibrated to your regulatory and qualification timelines.

This briefing frames the big strategic choices for 2026 — the year when printed batteries shift decisively from exploration to early commercialization. PW Consulting’s full study equips leaders to convert that inflection into durable advantage.

For detailed analysis of this topic, please visit the official page:Printed Battery Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com